Mobile service providers have not achieved much market share from content sales globally at least as measured by volume of downloads, Juniper Research estimates.

Mobile operator storefronts and portals now account for about six percent of content downloads worldwide, with Google Play and Apple’s App Store now comprising nearly 70 percent between them.

That has lead many operators to close their own storefronts, Juniper Research says. On the other hand, the value of mobile content that could be sold using direct carrier billing could rise from $2 billion in 2012 to more than $13 billion by 2017, according to Juniper Research.

Direct carrier billing might therefore be said to represent a more lucrative mobile service provider revenue opportunity than selling mobile content.

Analysys Mason forecasts that direct carrier billing will provide service providers with more than US$12 billion in revenue in 2022.

According to mobile applications vendor Ebscer, since BlackBerry introduced carrier billing in August 2010, the percent of sales coming from carrier billing has increased every month for Ebscer.

At the end of April 2011, over 25 percent of total app sales for Ebscer in BlackBerry App World were coming from operator billing.

Wednesday, March 6, 2013

Service Providers Not Making Much Money from Mobile Content, Billing for It Is More Lucrative

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Who Does Google Compete With?

Who does Google compete with, strategically? Over the years, many names have been discussed, including Yahoo, Microsoft or Apple. Google sometimes is said to be unable to compete with some others, such as Facebook. But increasingly, the name that appears is "Amazon."

So it is that Google has begun testing a same-day delivery service with retailers, a move that obviously will be seen as part of a wider head to head competition with Amazon in the e-commerce space, as part of Google Shopping Express.

For a firm historically associated with an advertising revenue base, that might sound odd. But lots of application providers and some service providers now see "mobile commerce" as the next big revenue frontier, with angles ranging from promotion to payments to couponing and payments, as well as a broader "product sales" function.

That shift might see Goolge Shopping Express evolve in the direction of becoming a full marketplace, more like Amazon.

So it is that Google has begun testing a same-day delivery service with retailers, a move that obviously will be seen as part of a wider head to head competition with Amazon in the e-commerce space, as part of Google Shopping Express.

For a firm historically associated with an advertising revenue base, that might sound odd. But lots of application providers and some service providers now see "mobile commerce" as the next big revenue frontier, with angles ranging from promotion to payments to couponing and payments, as well as a broader "product sales" function.

That shift might see Goolge Shopping Express evolve in the direction of becoming a full marketplace, more like Amazon.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Leap Doesn't Find iPhones Too Helpful, Apparently

One has to wonder whether the highest-end devices are such a good match for value segment mobile customers.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Broadband Matters When People Figure Out What to Do with It

"The U.K.’s broadband market is already in rude health," said Ed Vaizy, U.K. Parliamentary Under Secretary of State for Culture, Communications and Creative Industries. What the heck does that mean?

Basically, that the United Kingdom has done a good job of bringing low cost broadband access to its people, offering access at low prices, caused by high degrees of market competition. Challenges remain, particularly in rural areas.

"The U.K. currently benefits from low prices and a high degree of competition in the broadband market," said Vaizy. "The U.K. has the best deals available for consumers across a selection of pricing bundles in the major European economies."

But the role of "demand stimulation" also was cited as key. In other words, beyond making access possible, as much hinges on people figuring out ways to use broadband to grow the economy.

"But we cannot create a world class connected Britain just by laying more fiber in the ground or building new base stations," Vaizy said. " It is also crucial that we get as many people as possible online enjoying the benefits presented by better connectivity, and also encourage British companies to expand and develop their internet-based operations."

"Ultimately it is users that will turn infrastructure investment into growth," he said.

In other words, a fixation on "raw speed" is misplaced. What ultimately matters more is what people figure out they can do with broadband, in ways that benefit the economy.

Basically, that the United Kingdom has done a good job of bringing low cost broadband access to its people, offering access at low prices, caused by high degrees of market competition. Challenges remain, particularly in rural areas.

"The U.K. currently benefits from low prices and a high degree of competition in the broadband market," said Vaizy. "The U.K. has the best deals available for consumers across a selection of pricing bundles in the major European economies."

But the role of "demand stimulation" also was cited as key. In other words, beyond making access possible, as much hinges on people figuring out ways to use broadband to grow the economy.

"But we cannot create a world class connected Britain just by laying more fiber in the ground or building new base stations," Vaizy said. " It is also crucial that we get as many people as possible online enjoying the benefits presented by better connectivity, and also encourage British companies to expand and develop their internet-based operations."

"Ultimately it is users that will turn infrastructure investment into growth," he said.

In other words, a fixation on "raw speed" is misplaced. What ultimately matters more is what people figure out they can do with broadband, in ways that benefit the economy.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

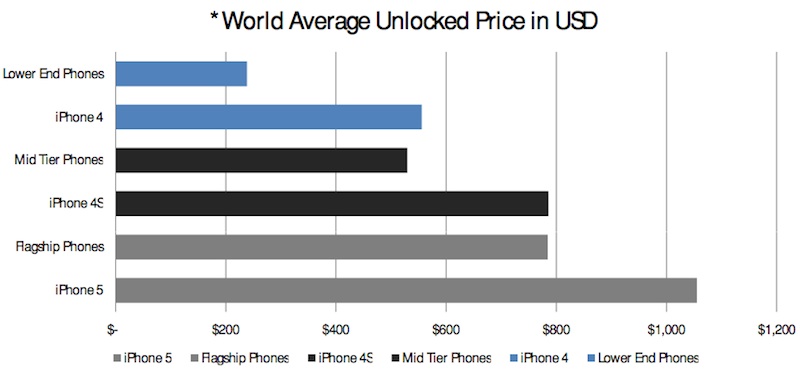

How Much Difference Will Unlocked Phones Make?

It’s hard to ascertain the real prospects for actual movement by the U.S. federal government to mandate mobile phone unlocking in the U.S. market. But it would be fair to say that is the sort of issue politicians like. It makes them sound very “pro-consumer,” at little “cost.”

That’s a dangerous combination for any industry. But it might also be fair to note that the actual benefits to consumers might be relatively modest, even if such new rules were to become part of the framework of mobile “consumer protection and choice,” as it is certain the matter would be sold.

Presumably, the value of unlocked devices will becomes a bigger actual value to consumers only when Long Term Evolution fourth generation networks are fully established in the U.S. market, for some simple reasons.

Unlike many other countries, subscribers and networks are at the moment split into GSM (AT&T and T-Mobile USA) and CDMA (Verizon Wireless and Sprint) air interface camps. An unlocked CDMA device cannot be used on the AT&T and T-Mobile USA neteworks, while a GSM unlocked device cannot be used on the Verizon or Sprint networks.

So while the idea “sounds nice,” the actual amount of consumer value is much less than most probably would think. That is not to say there is “no” value, only that the actual value might wind up being rather minor.

And some would say it doesn’t make sense to cause potential major damage to obtain a relatively small amount of benefit.

But the value of unlocking might be more subtle than many expect. If unlocked phones are sold at full retail prices, when consumers have the choice of a subsidized device, it seems likely to expect most consumers still will continue to opt for a subsidized device. That is especially true for the popular higher end devices.

Not many consumers are going to prefer shelling out full retail price for the latest Apple iPhone, even if they can, when the alternative is a lower device acquisition price, even at the cost of higher monthly recurring costs than might be possible if subsidies were not offered and available.

Beyond that, unlocking might help some consumers and provider segments, especially users on the “value” end of the market, and some firms that specialize in refurbishing and selling reconditioned devices.

That might be helpful for some businesses, and some U.S. consumers. ReCellular has been said to be one of the largest U.S.-based mobile phone refurbishers, and a mandatory “unlocked” phone regime might help such firms by boosting the value of used devices, at least marginally.

ReCellular resold or recycled 5.2 million mobile devices in 2010. ReCellular sells about 60 percent of its phones in the U.S. market and the rest mostly to dealers in Asia, Africa, Latin America and Eastern Europe.

But one might note that the market for used phones is relatively small. Global sales of used phones total a few hundred million units a year, estimates Andy Castonguay, an analyst at consulting firm Yankee Group. That compares with the 1.6 billion new phones sold world-wide last year.

That is only a proxy for the degree to which U.S. consumers might actually take their unlocked phones and switch to a different service provider.

For one thing, most consumers do not seem to keep any single device all that long. According to one U.S. study, the typical mobile device is used 18 months before being replaced. Whether that would be different in an unlocked device context is unclear.

The point is that people in the U.S. market mostly do not seem to want to keep their devices that long, whether they use one service provider or had a device that enabled easy switching. Keep in mind that the 18-month figure, like all “averages,” hides the differences between some users who will keep any device longer, and some who will replace devices even faster than 18 months.

That is not to say device unlocking would have zero advantages for end users and some businesses. It is harder to say what such rules might do for device innovation or the fortunes of mobile service providers.

Service provider revenues might be lower in an unlocked phone regime, since device sales count as “revenue,” and since unlocked device service plans would likely be lower than current plans that include the subsidy recovery.

And it is hard to see how competition between service providers would be less robust, in a full unlocked device regime, than under the current situation.

Service providers might sell fewer phones in the first place, as retail distribution shifts to third party retailers. Whether that helps or hurts service providers is tough to say, with precision.

On the other hand, service providers might benefit. The cost of phone subsidies might drop, so lower “revenue” might also be balanced by lower operating costs.

But service providers might have less ability to “control” customers or stabilize expected revenues that are “less lumpy” because the current two-year contracts reduce churn.

The point is that although the conventional wisdom is that mandatory phone unlocking will help consumers and harm service providers, it is not clear how big those changes might be. Every action has unintended consequences beyond the reactions service providers will undertake.

That’s a dangerous combination for any industry. But it might also be fair to note that the actual benefits to consumers might be relatively modest, even if such new rules were to become part of the framework of mobile “consumer protection and choice,” as it is certain the matter would be sold.

Presumably, the value of unlocked devices will becomes a bigger actual value to consumers only when Long Term Evolution fourth generation networks are fully established in the U.S. market, for some simple reasons.

Unlike many other countries, subscribers and networks are at the moment split into GSM (AT&T and T-Mobile USA) and CDMA (Verizon Wireless and Sprint) air interface camps. An unlocked CDMA device cannot be used on the AT&T and T-Mobile USA neteworks, while a GSM unlocked device cannot be used on the Verizon or Sprint networks.

So while the idea “sounds nice,” the actual amount of consumer value is much less than most probably would think. That is not to say there is “no” value, only that the actual value might wind up being rather minor.

And some would say it doesn’t make sense to cause potential major damage to obtain a relatively small amount of benefit.

But the value of unlocking might be more subtle than many expect. If unlocked phones are sold at full retail prices, when consumers have the choice of a subsidized device, it seems likely to expect most consumers still will continue to opt for a subsidized device. That is especially true for the popular higher end devices.

Not many consumers are going to prefer shelling out full retail price for the latest Apple iPhone, even if they can, when the alternative is a lower device acquisition price, even at the cost of higher monthly recurring costs than might be possible if subsidies were not offered and available.

Beyond that, unlocking might help some consumers and provider segments, especially users on the “value” end of the market, and some firms that specialize in refurbishing and selling reconditioned devices.

That might be helpful for some businesses, and some U.S. consumers. ReCellular has been said to be one of the largest U.S.-based mobile phone refurbishers, and a mandatory “unlocked” phone regime might help such firms by boosting the value of used devices, at least marginally.

ReCellular resold or recycled 5.2 million mobile devices in 2010. ReCellular sells about 60 percent of its phones in the U.S. market and the rest mostly to dealers in Asia, Africa, Latin America and Eastern Europe.

But one might note that the market for used phones is relatively small. Global sales of used phones total a few hundred million units a year, estimates Andy Castonguay, an analyst at consulting firm Yankee Group. That compares with the 1.6 billion new phones sold world-wide last year.

That is only a proxy for the degree to which U.S. consumers might actually take their unlocked phones and switch to a different service provider.

For one thing, most consumers do not seem to keep any single device all that long. According to one U.S. study, the typical mobile device is used 18 months before being replaced. Whether that would be different in an unlocked device context is unclear.

The point is that people in the U.S. market mostly do not seem to want to keep their devices that long, whether they use one service provider or had a device that enabled easy switching. Keep in mind that the 18-month figure, like all “averages,” hides the differences between some users who will keep any device longer, and some who will replace devices even faster than 18 months.

That is not to say device unlocking would have zero advantages for end users and some businesses. It is harder to say what such rules might do for device innovation or the fortunes of mobile service providers.

Service provider revenues might be lower in an unlocked phone regime, since device sales count as “revenue,” and since unlocked device service plans would likely be lower than current plans that include the subsidy recovery.

And it is hard to see how competition between service providers would be less robust, in a full unlocked device regime, than under the current situation.

Service providers might sell fewer phones in the first place, as retail distribution shifts to third party retailers. Whether that helps or hurts service providers is tough to say, with precision.

On the other hand, service providers might benefit. The cost of phone subsidies might drop, so lower “revenue” might also be balanced by lower operating costs.

But service providers might have less ability to “control” customers or stabilize expected revenues that are “less lumpy” because the current two-year contracts reduce churn.

The point is that although the conventional wisdom is that mandatory phone unlocking will help consumers and harm service providers, it is not clear how big those changes might be. Every action has unintended consequences beyond the reactions service providers will undertake.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, March 5, 2013

More Rumors about Verizon Buyout of Vodafone Stake in Verizon Wireless

That there are new rumors about Verizon wanting to acquire the rest of Vodafone’s stake in Verizon Wireless is not surprising. Vodafone recently denied any such talks were underway.

Such denials are commonplace in both politics and business. And though the denials are not always a cover for actual talks, Vodafone’s latest quarterly financial report illustrates the reasons why some analysts and executives at Verizon, might be weighing some action to change the current ownership status of Verizon Wireless.

To be sure, Verizon also has said no such talks are underway. In fact, Verizon recently said no talks about a full purchase of the 45 percent Vodafone stake in Verizon were underway.

That would still leave some room for less complicate measures, such as a gradual purchase by Verizon of Vodafone shares. Some also would say a full-blown merger is a possibility. Sure, it might be, but such a huge deal would present at least some significant regulatory issues.

Where the U.S. Federal Communications Commission would allow Verizon to become that much bigger is a valid question, even though either a buyout of the Vodafone stake, or a full merger, would not immediately affect U.S. mobile market share.

Vodafone posted a worse than expected drop in group revenue for the last three months of 2012, and Vodafone might prefer to liquify its Verizon Wireless stake to pay down debt, for example.

Beyond that, low interest rates make acquisitions attractive at the moment, in large part because organic growth opportunities are limited.

Such denials are commonplace in both politics and business. And though the denials are not always a cover for actual talks, Vodafone’s latest quarterly financial report illustrates the reasons why some analysts and executives at Verizon, might be weighing some action to change the current ownership status of Verizon Wireless.

To be sure, Verizon also has said no such talks are underway. In fact, Verizon recently said no talks about a full purchase of the 45 percent Vodafone stake in Verizon were underway.

That would still leave some room for less complicate measures, such as a gradual purchase by Verizon of Vodafone shares. Some also would say a full-blown merger is a possibility. Sure, it might be, but such a huge deal would present at least some significant regulatory issues.

Where the U.S. Federal Communications Commission would allow Verizon to become that much bigger is a valid question, even though either a buyout of the Vodafone stake, or a full merger, would not immediately affect U.S. mobile market share.

Vodafone posted a worse than expected drop in group revenue for the last three months of 2012, and Vodafone might prefer to liquify its Verizon Wireless stake to pay down debt, for example.

Beyond that, low interest rates make acquisitions attractive at the moment, in large part because organic growth opportunities are limited.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, March 4, 2013

U.K. 4G LTE Frequency Allotments

After some trading activity, the actual spectrum allotments for U.K. 4G LTE providers appear to be set.

The middle block is the Time Division Duplex spectrum, the surrounding ones are uplink and downlink pairs

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...

{kind=link}