Genachowski notes that the United States is the first country deploying 4G LTE networks at scale, and in late 2012 the U.S. had as many LTE subscribers as the rest of the world combined, making the United States the global test bed for LTE apps and services.

The FCC report also notes that Long Term coverage has grown rapidly since 2010, when virtually no customers could buy LTE, from nothing in mid-2010 to 86 percent of the U.S. population as of October 2012.

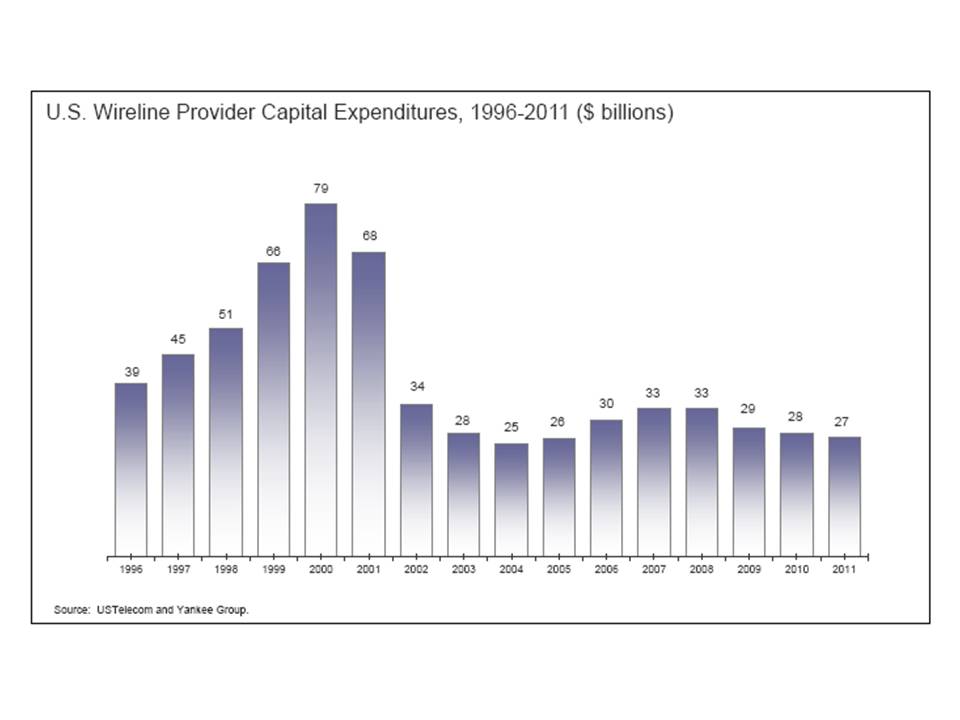

Annual investment in U.S. wireless networks grew more than 40 percent between 2009 and 2012, from $21 billion to $30 billion, while investment in European wireless networks has been flat since 2009, and wireless investment in Asia, including China, is up only four percent during that time.

Genachowski notes that more than 90 percent of smart phones sold globally in 2012 run operating systems developed by U.S. companies, up from 25 percent three years ago.

Also, notes Genachowski, the new mobile apps economy is a “made in the U.S.A.” phenomenon as well.

It is reasonable to look at competition as it exists in rural areas, which always are more difficult for service providers to serve, compared to urban areas.

At the moment, at least 65.4 percent of the rural population can buy mobile broadband service from at least three different providers, and increasingly, people will be able to buy a 4G service.

In addition, 63.6 percent of rural square miles and 87.3 percent of rural road miles in the U.S. were covered by at least one mobile broadband provider, while 90.9 percent of non-rural square miles and 98.7 percent of non-rural road miles were covered by at least one mobile broadband providers, the FCC says.

Based on October 2012 Mosaik data, 97 percent of the U.S. rural population has coverage by at least one mobile wireless broadband provider, up from 92 percent in November 2009.

In contrast, 99.9 percent of the non-rural population is covered by at least one mobile broadband provider.

While rural mobile broadband coverage has improved, 1.3 million people in rural areas have no mobile broadband access.

While 97.7 percent of the population in non-rural areas was covered by two or more mobile broadband providers, only 89.7 percent of the rural population was covered by two or more providers as of October 2012, up from 69.1 percent as of August 2010, according to the FCC.

Furthermore, 65.4 percent of the rural population was covered by at least three providers and 37.4 percent by at least four providers, compared to 97.7 percent and 92.4 percent, respectively, for the non-rural population as of October 2012.

This represents an increase in coverage to the rural population since August 2010 when only 38.1 percent of the rural population was covered by three or more providers and only 17.1 percent was covered by four or more providers, according to the FCC.

With regard to rural road miles, 87.3 percent are covered by at least one mobile broadband provider, compared to 98.7 percent of non-rural road miles.

In addition, while only 67.7 percent of rural road miles are covered by at least two mobile broadband providers, 95.8 percent of non-rural road miles are covered by at least two mobile broadband providers.

In addition, only 35.7 percent of rural road miles are covered by at least three mobile broadband providers and only 14.2 percent by four mobile broadband providers compared to 86.6 and 71.8 percent, respectively, of non-rural road miles.

There are other potential implications as well, namely the growing likelihood that AT&T and Verizon, among others, will use LTE as ways to provide new broadband access alternatives to fixed networks in rural areas.

“Mobile wireless Internet access service could provide an alternative to wireline service for consumers who are willing to trade speed for mobility, as well as consumers who are relatively indifferent with regard to the attributes, performance, and pricing of mobile and fixed platforms,” the FCC says.

in 2010, Verizon Wireless launched the “LTE in Rural America Program” to expand LTE coverage in rural areas.

Under this program, Verizon Wireless leases portions of its 700 MHz Upper C Block spectrum licenses to facilities-based mobile wireless service providers in rural areas where Verizon Wireless currently lacks coverage and does not intend to build out.

The rural partners also gain reciprocal roaming rights on Verizon Wireless’s nationwide LTE network, while Verizon Wireless’s customers can roam on the rural providers’ LTE networks when traveling in such areas.

As of September 2012, the program included 18 small, rural providers that planned to launch LTE to areas covering 2.7 million people across 14 states.1207 In April 2012,

Will consumers really care if the out of pocket monthly payments for T-Mobile USA service are marginally lower, in the case of services without subsidies but with an installment plan?

Will consumers really care if the out of pocket monthly payments for T-Mobile USA service are marginally lower, in the case of services without subsidies but with an installment plan?