PwC expects entertainment and media spending to keep growing. Video subscription service providers might not agree that can hold up over the long term. While it might be true that advertising spending is growing, especially in the online and mobile areas, it might not be so true to forecast continuing end user spending on video services.

PwC thinks consumers will keep spending five percent a year more, for the next several years. But no market grows to "infinity," and there are abundant signs that younger consumers do not watch television so much, do not own televisions, and do not want to pay for television, even when the cost of doing so is not an issue.

All the while, new experiments with Internet-delivered video continue to grow. Intel plans a new streaming service. Netflix, iTunes, Google, Dish Network, Amazon Prime, Hulu and others are going to keep expanding their menus. Aereo appears ready to disrupt the broadcast TV revenue stream.

And even though video service providers allow some streaming to keep their traditional video subscription service customers, all it takes is a change of heart by the content owners, and a willingness to go "direct to the end user," for significant change to happen.

On the other hand, consumer budgets are not infinite, either. So a reasonable supposition is that most people will substitute one form of spending for another. In other words, if able to buy discrete programs or channels, and stream them, they will spend less money on traditional video subscription services, increase spending for online alternatives, and then likely increase the amount of money they spend on broadband access, as well.

But it wouldn't be unreasonable to predict that the net change in recurring spending will not be much different from what people spend now. Perhaps oddly, many consumers might find they do not actually wind up saving much money. The lower video service payments will be matched by new online subscription fees and higher broadband access spending.

So one might predict that average spending on broadband access could grow, at some point, as traditional video service spending falls. But recurring payments would probably be equal to, or less than current payments. In fact, spending should be less, overall.

The reason is that people are rational. They will decide whether they can save money overall by switching. If they can't save money, there is little incentive to switch.

Sunday, April 7, 2013

Will Some "Entertainment" Spending Shift to "Communications" Spending?

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Saturday, April 6, 2013

Bet on it: Austin, Texas is Getting Google Fiber

It seems virtually certain that Google Fiber is going to be built in Austin, Texas. In fact, the news apparently was mistakenly posted on the Google Fiber website.

Speculation has been building since Google and the city of Austin are holding a press conference on April 9, 2012 to announce something.

And though there are other possible explanations, the big rumor is that Austin will be the next community to get 1-Gbps Google Fiber.

So once again observers will speculate on what Google might ultimately intend, aside from prodding big ISPs to invest faster in gigabit broadband access networks. Maybe Google is not even so sure itself.

If Google can leverage a few such 1-Gbps networks to get major ISPs to invest their own capital to match, Google wins. It gets the faster networks that support its business without having to invest capital better spent elsewhere.

And though some of us might doubt that Google can dramatically change the economics of gigabit fixed network access, does it matter if Google ultimately can eke out a capex cost reduction?

It might, though not because of any 30-percent theoretical cost savings. The bigger issue is whether the overall business cases is a positive number, after revenue, capex and opex expenses are tallied.

It might be a stretch, but there is some combination of subscriber adoption, monthly recurring revenue and then amortized capex and operating expense that would allow Google Fiber to be a going concern, on a sustainable basis.

The challenge is simply that the assumptions are formidable.

When Verizon launched FIOS almost a decade ago, it estimated a cost of about $1,350 per home passed. But Verizon now says costs are far lower, possibly in the $700 range.

If Google can set new standards for marketing and operating cost, and if it can get high penetration, perhaps it can demonstrate that 1-Gbps networks are feasible on a wider scale.

That is a big “if,” some might say. Consider a business case where Google Fiber costs 30 percent less than what Verizon paid for FiOS. Actually, that is easily doable, some might argue. Assume 30 percent operating cash flow.

As it turns out, adoption (subscriber penetration) then becomes the key variable.

Even if one assumes 75 percent adoption, which is the biggest assumption of all, Google Fiber might not offer a payback. And 75 percent penetration would be a historic achievement in the era of competitive communications and video entertainment.

So Google Fiber would have to make history, overturning all prior assumptions about take rates, to prove financially viable, some would argue. Alternatively, Google Fiber might consider some other ways to generate more revenue per subscriber, thus lowering the breakeven level of penetration. But it is hard to see what additional services could materially lift average revenue per user.

Should Austin actually become a second Google Fiber site, and there now are many reasons to believe that will happen, the effectiveness of the prod to other ISPs will hinge, in part, on penetration.

If Google Fiber upsets the typical market share structure of a competitive triple-play market, you will see investment increase almost across the board.

And that, for Google, is winning big.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

$30 Billion in Annual Economic Losses--1/2 to Small Businesses--From Patent Trolls

There's a fine line between copyright and patent protection and patent and copyright abuse. But a study by James Bessen and Michael J. Meurer of Boston University School of Law suggests the annual cost to firms to defend themselves against "patent trolls" ("non-practicing entities" that buy patents only to sue others for infringement) runs as high as $29 billion annually.

That amount includes the actual direct costs of litigation and non-litigated legal expenses, plus diversion of resources, delays in new products, and loss of market share.

Much of this burden falls on small and medium-sized companies. The median company sued had $10.8 million in annual revenues. Some 82 percent of the defendants had less than $100 million in revenue and these accounted for 50 percent of the defenses.

Small and medium-sized companies account for 37 percent of the accrued direct costs, the study estimates.

The annual wealth lost from NPE lawsuits--for public companies--is about $80 billion, another study also estimated.

To be sure, some might argue that such lawsuits allow some small inventors to make more money. But that has to be balanced against the damage such litigation imposes on firms trying to innovate.

Also, to be fair, one firm's "expense" is another firm's "income." There is a good reason attorneys like NPEs: it is revenue for them, even if that comes at social and economic expense for technology innovators.

That amount includes the actual direct costs of litigation and non-litigated legal expenses, plus diversion of resources, delays in new products, and loss of market share.

Much of this burden falls on small and medium-sized companies. The median company sued had $10.8 million in annual revenues. Some 82 percent of the defendants had less than $100 million in revenue and these accounted for 50 percent of the defenses.

Small and medium-sized companies account for 37 percent of the accrued direct costs, the study estimates.

The annual wealth lost from NPE lawsuits--for public companies--is about $80 billion, another study also estimated.

To be sure, some might argue that such lawsuits allow some small inventors to make more money. But that has to be balanced against the damage such litigation imposes on firms trying to innovate.

Also, to be fair, one firm's "expense" is another firm's "income." There is a good reason attorneys like NPEs: it is revenue for them, even if that comes at social and economic expense for technology innovators.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Friday, April 5, 2013

Less Chance Verizon and AT&T Could Buy Vodafone Than Any of Them Buying Several Smaller Mobile Operators

Perhaps it would have been just a "bridge too far," but any joint AT&T-Verizon Communications bid to buy all of Vodafone would have been breathtaking, if only because of the size of Vodafone, Verizon and AT&T on a global basis.

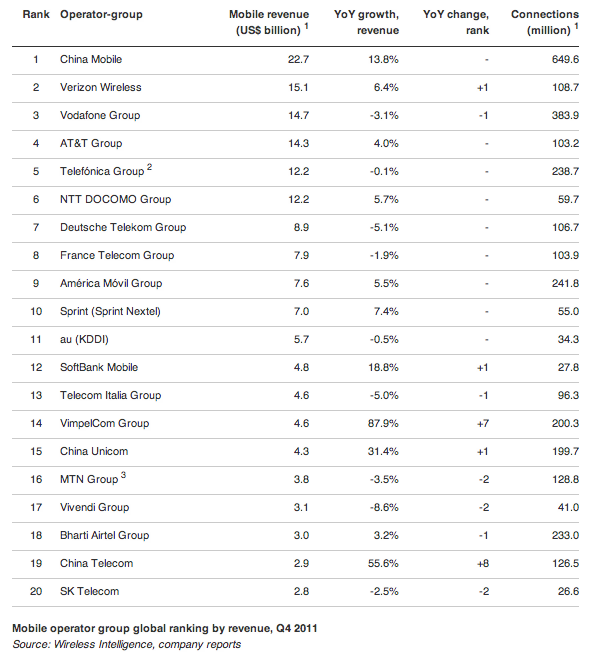

China Mobile, Verizon Wireless, and Vodafone might be the largest mobile operators globally, counting by revenue.

A different ranking is obtained if one counts by number of subscribers. Yet a third ranking is obtained if one measures according to monthly revenue per customer. But there is no doubt all three of the carriers rumored to be part of a potential bid are huge.

So you can see the problem Verizon or Vodafone would face, if either tried to buy the other. The recent announcement by Verizon Communications that it had no interesting in buying all of Vodafone is interpreted by some observers to mean that Vodafone rejected Vodafone rejected Verizon’s terms, not that Verizon was not pursuing such a deal.

Some might therefore speculate that, aside from Verizon acquiring the rest of Verizon Wireless it does not already own, it would make more sense for Vodafone, China Mobile, Verizon and AT&T to buy any of the smaller mobile operators whose revenue is an order of magnitude lower than those of China Mobile, Verizon, Vodafone and AT&T.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Why WISPs Do Not Worry About "Dumb Pipe"

Wireless ISPs do not seem to worry much about becoming “dumb pipe” providers. Having no large “service” businesses in voice or video to lose, WISPs seem professionally comfortable with “primarily” providing Internet access, even though many also sell voice and video entertainment.

The point is that telco or cable company fundamentally is an ISP, whatever else those firms do. WISPS seem to have little trouble “getting” that element of their businesses.

That might be why it seems so natural for a WISP executive to say “I think we are entertainment transport providers, more than anything,” as Doug Watkins of Blast Communications, has noted.

Referring to online and over the top apps such as Netflix, Hulu, Amazon Prime and YouTube, the phrase indicates the key challenges WISPs face these days, namely coping with growing demand by their customers for bandwidth sufficient to “watch video.”

Though other service provider executives reflexively rail against the notion that their business is, substantially, getting to be a “dumb pipe” business, there possibly are new signs that reality is sinking in. And that reality is that. like it or not, the future of the business is substantially built on “dumb pipe” access to the Internet, most of which is related to entertainment video.

“Built on” Internet access does not mean “exclusively” built on such “dumb pipe.” Video entertainment services, voice, machine to machine services or computing, storage or software as a service will be delivered as services riding on top of the access.

People sometimes use phrases such as “smart pipe” or “happy pipe” to try and make the point that “there are other things we do.” That sort of misses the point.

In large part, future communications suppliers will be “Internet service providers,” which largely is a dumb pipe service. Some ISPs might try introducing access with quality of service features, which might legitimately allow those ISPs to claim they are in the “smart pipe” business.

No matter. There is no inherent reason why any form of Internet access has to be a “low gross margin” business, or a “low gross revenue” business.

Nor is an ISP restricted from selling other services that are not, in fact, “Internet” services (such as carrier voice and video entertainment, machine to machine and cloud services).

That said, broadband Internet access is the foundation for the rest of the services suite, including those services using IP, but which are not “Internet” services, such as branded carrier voice and video entertainment.

The point is that telco or cable company fundamentally is an ISP, whatever else those firms do. WISPS seem to have little trouble “getting” that element of their businesses.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tablet Adoption in Emerging Markets Could Affect Fixed Broadband Prospects

It would clearly be rational to argue that the smart phone is going to be the most ubiquitous device used to access the Internet, in most emerging markets. But tablet importance is going to grow, especially if smart phone communications are grafted onto a greater number of tablet models.

In some ways, it might not matter whether people rely on smart phones or tablets as their primary Internet access device, especially if it is a mobile network that provides the access. But the balance of tablets and smart phones in use for primary Internet access might have huge consequences for ISPs.

The reason is that if the tablet emerges as the key Internet access device, the odds of fixed networks being used would rise commensurately, if the assumption is that tablets will use Wi-Fi access, not a mobile 3G or 4G connection.

Right now, smart phones have the higher installed base. But tablet use is growing faster, from a much smaller base.

Smart connected device volume in emerging markets grew by 41.3 percent in 2012 with the tablet volume growing by 111.3 percent and smart phone volume by 69.7 percent year over- year.

By the end of year 2017, IDC predicts that the tablet and smart phone markets will have huge growth in the emerging markets.

In emerging markets, tablet unit shipments are expected to increase by 300 percent, while smart phone unit shipments are expected to double.

"In emerging markets, consumer spending typically starts with mobile phones and, in many cases, moves to tablets before PCs," says Megha Saini, IDC research analyst.

That could have important implications for providers of fixed broadband service in many markets, even if mobile networks remain the main way most people get access to the Internet.

Smart Connected Device Year-over-Year Growth by Region and Product Category, 2012-2017

Region

|

Product Category

|

2012

|

2013*

|

2017*

|

Mature Market

|

Desktop PC

|

-4.8%

|

-5.5%

|

-2.9%

|

Mature Market

|

Portable PC

|

-8.1%

|

-3.1%

|

-1.4%

|

Mature Market

|

Tablet

|

62.8%

|

41.4%

|

8.3%

|

Mature Market

|

Smartphone

|

20.6%

|

15.1%

|

4.6%

|

Total Market

|

15.6%

|

13.8%

|

4.2%

| |

Emerging Markets

|

Desktop PC

|

-3.8%

|

-3.5%

|

0%

|

Emerging Markets

|

Portable PC

|

-0.8%

|

4.1%

|

7.1%

|

Emerging Markets

|

Tablet

|

111.3%

|

60.7%

|

13.4%

|

Emerging Markets

|

Smartphone

|

69.7%

|

35.1%

|

12.2%

|

Total Market

|

41.3%

|

26.6%

|

10.9%

| |

Worldwide

|

Desktop PC

|

-4.1%

|

-4.3%

|

-1.0%

|

Worldwide

|

Portable PC

|

-3.4%

|

0.9%

|

3.7%

|

Worldwide

|

Tablet

|

78.4%

|

48.7%

|

10.6%

|

Worldwide

|

Smartphone

|

46.1%

|

27.2%

|

9.8%

|

Total Market

|

29.1%

|

21.2%

|

8.5%

|

Source: IDC

Smart Connected Device Market by Product Category, Shipments, Market Share, 2012-1016 (units in millions)

Product Category

|

2012 Unit Shipments

|

2012 Market Share

|

2017 Unit Shipments*

|

2017 Market Share*

|

2012—2017 Growth*

|

Desktop PC

|

148.4

|

12.4%

|

141.0

|

6.0%

|

-5.0%

|

Portable PC

|

202.0

|

16.8%

|

240.9

|

11.0%

|

19.3%

|

Tablet

|

128.3

|

10.7%

|

352.3

|

16%

|

174.5%

|

Smartphone

|

722.4

|

60.1%

|

1,516

|

67%

|

109.9%

|

Total

|

1,201.1

|

100.0%

|

2,250.3

|

100.0%

|

87.3%

|

Source: IDC

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Thursday, April 4, 2013

"Unsubsidized" Phones Actually Would Change Very Little for End Users, Lots for Carrier Advertising

In many ways, the discussion about whether major service providers are better off selling only

non-subsidized phones misses the point. If a carrier allows subscribers to buy on installment plans, out of pocket costs of service might not change much.

The hit to operating earnings likewise might not change very much. What would change is the “headline” price for a monthly mobile service, which presumably could be lower by the amount of the avoided amortization of the smart phone “purchase.”

In reality, most consumers would still continue to pay the installment fee, so the consumer’s out of pocket expense might not change much, if at all. But the advertised headline price might be low enough to prevent some users from downgrading from a postpaid account to a prepaid account, probably provided by a rival supplier.

Verizon Wireless is not opposed to the idea of separating headline recurring service costs from any forms of consumer device purchases. Even if such changes did not really affect end user out of pocket recurring costs very much, the policies still would allow Verizon to advertise “lower prices.”

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...