Oddly enough, for some of us, a debate over access network architecture, specifically fiber to the home or fiber to the node, appears to be an issue in upcoming Australian elections.

One might argue that, given escalating demands for bandwidth, and national policies aiming to boost speeds to 100 Mbps by 2020, for example, that fiber to the home makes more sense. But others argue that the less-expensive fiber to node architecture will suffice.

The argument is an old one. Verizon Communications opted for fiber to the home. AT&T opted for fiber to the neighborhood (essentially, fiber to the node). U.S. cable operators likewise have opted for a fiber to the neighborhood approach.

But those older debates are more complicated than in the past, because of huge changes in revenue expectations. It never was necessary to build fiber access networks to support voice. All-copper networks work just fine for that application.

The other problem is that the voice business is shrinking, as users opt for mobile phones as their preferred way of calling. Mobile also is the preferred platform for messaging.

So the argument for fiber to the home explicitly relies on an assumption that new revenue sources can be found. In that respect, the argument is that fiber to the home works better, long term, for high speed access, and that video services also can be supported.

The former argument makes sense, but has not yet proven to be a show stopper, though Google Fiber’s symmetrical 1 Gbps for $70 a month could help settle the argument.

The latter argument, that fiber to the home is required for linear TV, likewise has not proven decisive, as both Verizon and AT&T are able to deliver linear TV services using either architecture.

Beyond that, there are concerns about the longevity of the video revenue stream, and questions about how much speed consumers will really want to pay for. Of course, Google Fiber hopes to upset those expectations.

Given all that, ironically, the debate over network architecture remains unsettled. Some rationally will argue the best policy is to invest as little as possible in fixed networks and emphasize mobile networks.

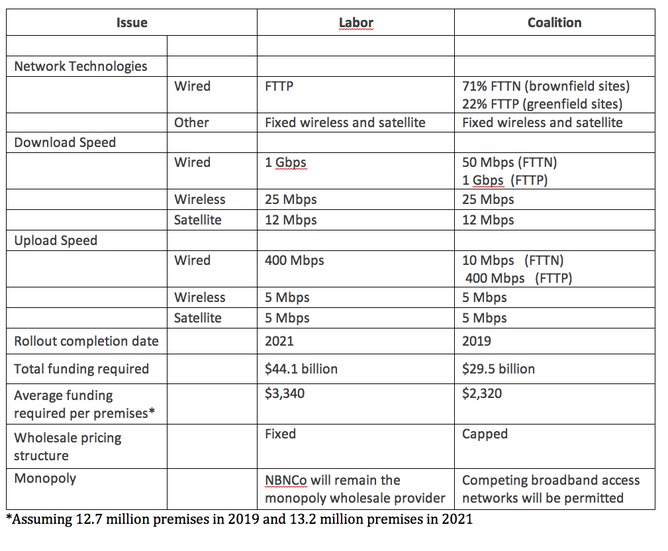

Under either scenario--fiber to home or fiber to node--the NBN would be a wholesale network. The fiber to home network has been estimated to cost A$44.1 billion and be finished about 2021.

The FTTN network could be finished by 2019, at a total cost of A$29.5 billion.

The FTTN network will provide download speeds of 50 Mbps network, while the fiber to home network will initially provide download speeds up to 1 Gbps.

But the analysis is more complicated than that. Under either scenario, rural areas will be served by satellites. But the access in other areas is mixed. The “fiber to home” proposal actually uses fixed wireless in many moderately-dense areas while only urban areas get fiber to the home.

Under the “fiber to the node” plan, satellites still would be the only viable option in rural areas, while fiber to the node would be used for retrofit areas, and fiber to the home deployed in all areas of new home construction.

The differences are exacerbated by uncertainty about future demand. The average Internet connection speed in Australia is currently 4.2 Mbps, for example.

But usage also seems to climb over time. For that reason, some believe broadband customers will be buying services of more than 100 Mbps by 2020 and about 1 Gbps by 2035.

Some argue that it simply makes more sense to put in fiber to the home now, even if it costs more.