It’s hard to overstate the gamble Steve Jobs and Apple in creating the iPhone back in January 2007. Not only was he introducing a new kind of phone — something Apple had never made before — he was doing so with a prototype that barely worked, in an industry notoriously controlled by the mobile service providers.

Fred Vogelstein's book “Dogfight: How Apple and Google Went to War and Started a Revolution” will be published in November 2013 and promises to be an excellent read.

Friday, October 4, 2013

The Big iPhone Gamble

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Walmart Drops Price of Apple iPhone 5c to $45 With 2-Year Contract

Walmart originally had priced the Apple iPhone 5c at $79 with a service contract. Now Walmart has dropped the price of the Apple iPhone 5c (16GB) to $45 with a two-year contract.

Best Buy is selling Apple's iPhone 5cfor $50 with a two-year contract.Besides beating Best Buy's price by $5, Walmart has another advantage: pricing is good at least through the end of the holiday season, while Best Buy's pricing is only good through Oct. 7, 2013.

RadioShack will discount the phone to $50, a price that will be good through Nov. 2, 2013.

"This is what we do: low prices is what we do," said Sarah Spencer McKinney, Walmart director of corporate communications. "As a price leader, we are always looking for ways to surprise our customers with low prices and disrupt the competition.

Best Buy is selling Apple's iPhone 5cfor $50 with a two-year contract.Besides beating Best Buy's price by $5, Walmart has another advantage: pricing is good at least through the end of the holiday season, while Best Buy's pricing is only good through Oct. 7, 2013.

RadioShack will discount the phone to $50, a price that will be good through Nov. 2, 2013.

"This is what we do: low prices is what we do," said Sarah Spencer McKinney, Walmart director of corporate communications. "As a price leader, we are always looking for ways to surprise our customers with low prices and disrupt the competition.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Consumers, Providers Profoundly Disagree about What A La Carte Video Might Cost

There is a huge disconnect between consumer and content owner or service provider expectations about what a TV channel should cost, if it were possible to buy channels one by one. Consumers think they will save money; distributors and content owners are just as certain they would not save money.

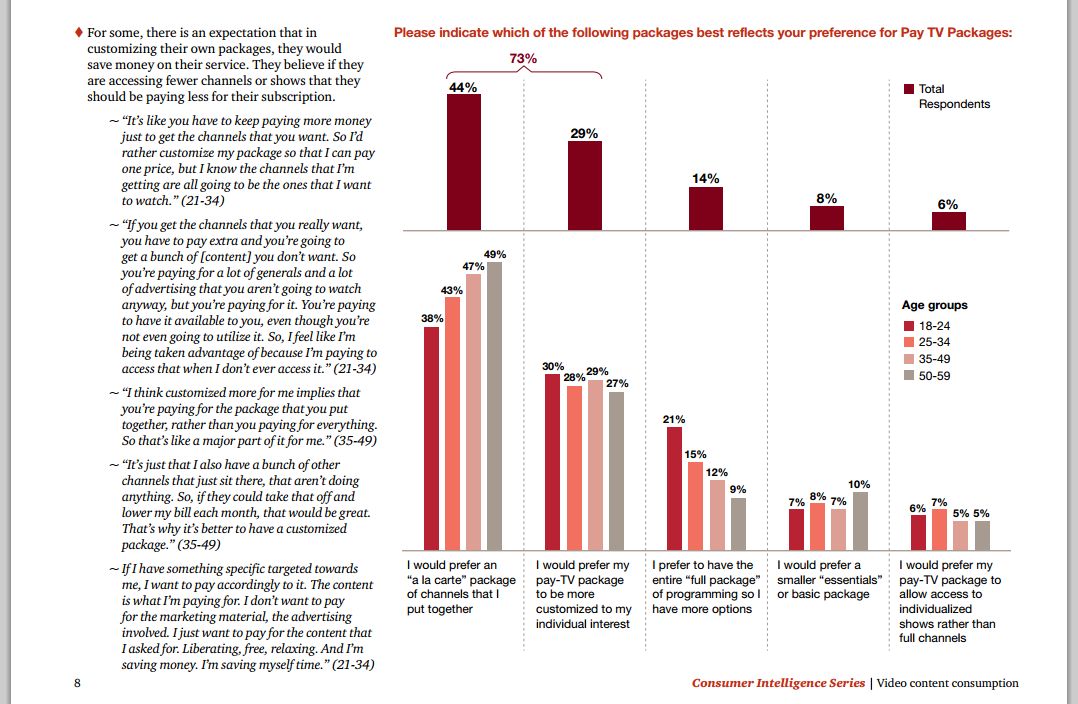

A study by PricewaterhouseCoopers indicates that 44 percent of consumers would like a the ability to buy all their channels one at a time.

Including the 29 percent of respondents that would prefer at least more customization of packages than is currently offered, some 73 percent of consumers surveyed would prefer either the full a la carte purchase option or at least some ability to customize.

Only 14 percent of respondents appear to be satisfied with the current method of packaging.

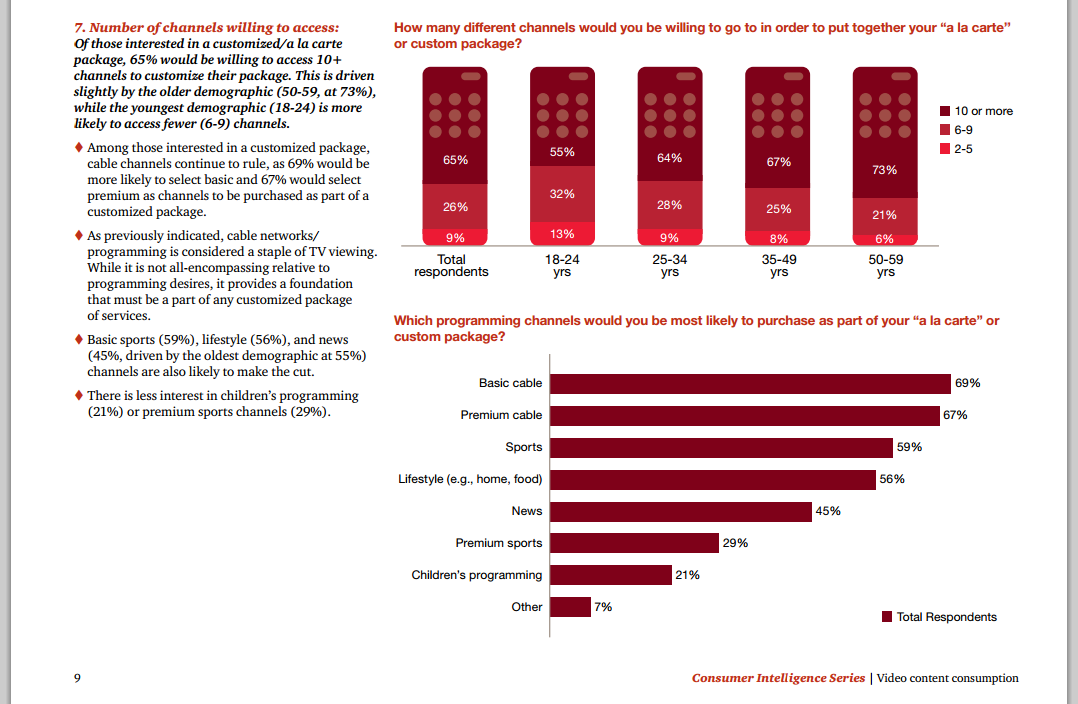

Of those interested in a customized or a la carte package, 65 percent would be willing to access 10 or more channels in a customized package. Older users (50-59) are more likely to want to buy 10 or more channels, while 55 percent of those 18 to 24 are more likely to prefer a package of 10 or more channels.

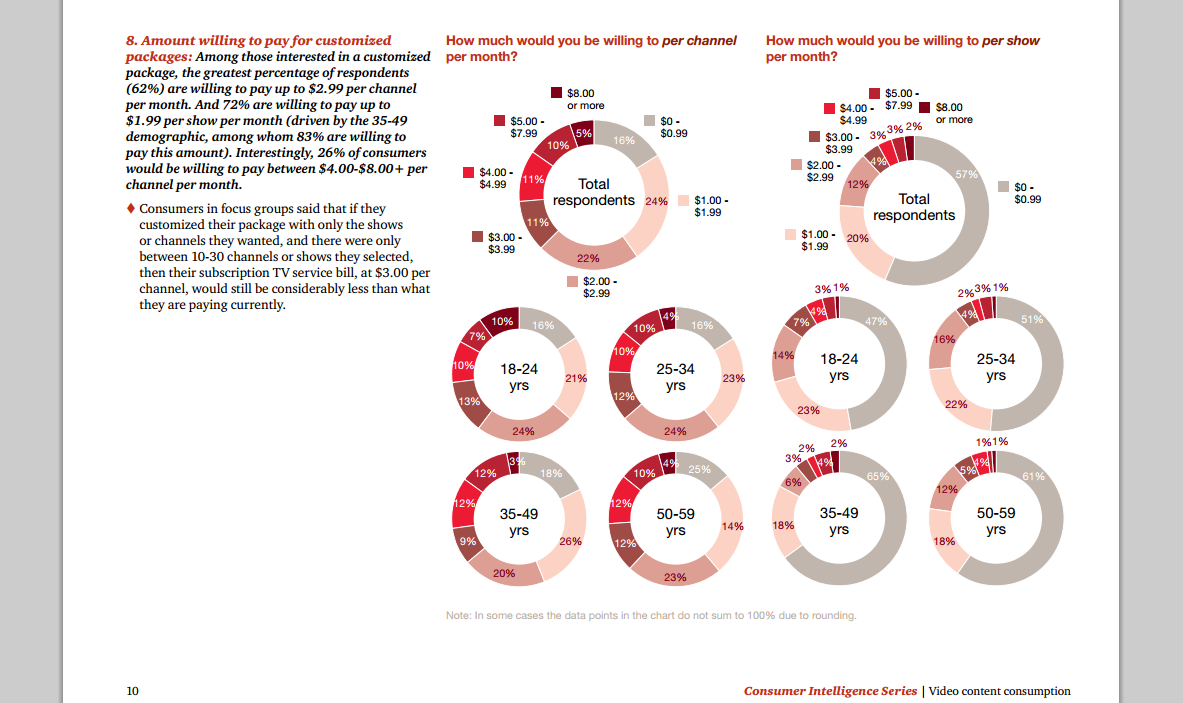

The expected pricing “per channel” is where the biggest disconnect exists. About 16 percent of respondents say they would not pay more than 99 cents a month for a channel. Some 24 percent will pay $1.99 and 22 percent will pay $2.99.

At $8 a month per channel, only about five percent of respondents indicated they would pay.

When asked about what they would pay for a single show, the survey found that 57 percent would not pay more than 99 cents a month for access to an individual show each month.

Some 20 percent indicated they would pay $1.99 for access to one TV show for a month (not per episode) and 12 percent would pay $2.99 for such access.

Only two percent would pay $8 a month for a show. If one assumes four episodes a month, tha indicates a fee of $4 per episode was considered too high.

Of respondents interested in a customized package, some 62 percent are willing to pay up to $2.99 per channel per month. About 72 percent are willing to pay up to $1.99 per show per month, driven by the 35-49 demographic, among whom 83 percent are willing to

pay this amount.

But 26 percent of consumers indicated they would be willing to pay between $4.00 to $8.00 per

channel per month.

Studies by the Federal Communications Commission seem to have concluded that unbundling could save money, or wouldn't save money, depending on how many channels a consumer buys under an a la carte regime, compared to what they buy now.

One of the studies suggested “consumers that purchase at least nine networks would likely face an increase in their monthly bills" when buying a la carte.

Likewise, one of the FCC studies suggested bill increases ranging from 14 percent to 30 percent under a la carte, while the other suggests a consumer purchasing 11 cable channels would face a change of bill ranging from a 13 percent decrease to a four percent increase, with a decrease in three out of four cases.

The point is that it is very hard to tell, conclusively, what might happen if providers shifted to a la carte viewing.

An economist might say the typical video bundle works because it allows distributors to apply scale and scope economics.

The corollary is that most networks, which are advertising supported, want to be part of a "no choice" basic tier for business reasons of their own, namely the ability to better sell the advertising that underpins their business models.

According to some studies, relatively few networks actually make a $100 million or more in annual ad revenue, though. That suggests they might have to make up the revenue shortfall some other way, in an a la carte regime.

When multichannel video distributors say a bundled approach creates economics that favor smaller, niche networks to thrive, they are right, economists might say.

Deprived of carriage on a broad "enhanced basic" tier, perhaps 60 percent of networks might find themselves immediately imperiled, as going concerns, some would estimate.

An end to bundling would likely harm most smaller, more-lightly-viewed networks. To the extent that content and program diversity is a desired end user benefit, "choice" in all likelihood would decline in a full a la carte environment, because most people would not buy most channels.

The possible advent of over-the-top TV viewing worries most in the current ecosystem for one compelling reason: "households view less than one quarter of the networks they are forced to buy in the bundle," the Consumers Union noted in an past analysis assuming a 50-channel offering.

Even today, with hundreds of available channels, end user behavior does not seem to have changed much. Most people watch a dozen or so channels on a regular basis.

And there are costs besides content fees. Cable operators have argued that end-user costs might actually climb in an a la carte environment, for a number of reasons. Higher customer care costs, operating and marketing are likely, cable operators have argued.

The point is that it is very hard to tell, conclusively, what might happen if providers shifted to a la carte viewing.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Does "Piracy" Explain Music Sales Decline? Maybe Not

Music piracy does not harm the commercial music business, a new study by the London School of Economics and Political Science argues.

The evidence does not support claims about overall revenue reduction due to individual copyright infringement, the study claims.

Some will contest that claim, as there is no getting around the fact that recorded music sales, as have sales of video content in packaged good form, have declined.

The point is not so much that piracy “does not matter.” Perhaps the more important implication is that punitive measures against individual online copyright infringers does not have the impact claimed by some in the creative industries.

The study notes that concert revenue and now mobile contributed revenue is offsetting the decline in recorded music sales.

One needn’t endorse content piracy to believe that in a digital era, new forms of monetization already have arisen, though.

And though one might argue “piracy” accounts for the dramatic decline in sales of recorded music is “caused” by piracy, one might argue that what has driven the change is a preference for renting rather than owning.

In essence, both buying an iTunes song and listening to Pandora are forms of renting rather than owning music.

One might further claim that piracy is killing the print content business, but that business was in decline at least a decade before the Internet was commonly used by most people. And some now say consumer attitudes about owning real estate or automobiles also are changing. Piracy certainly is not involved there.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

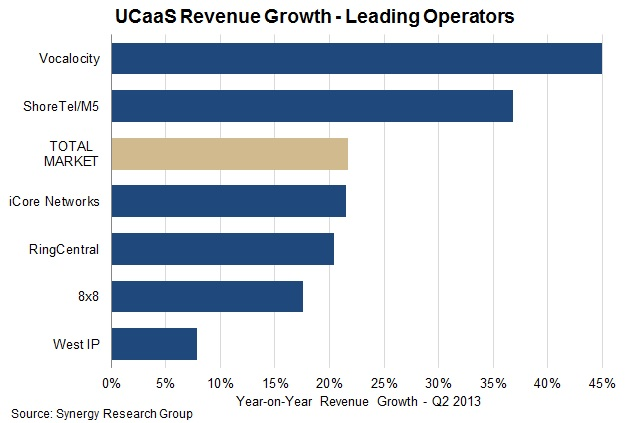

Is Hosted IP PBX Business Finally Getting Major Traction?

In any new market, for any new product or service, one typically looks for signs that adoption is about to move from early adopters to the mass market. Quite often, in the consumer space, that happens when total adoption reaches 10 percent of households. There obviously is no direct business-to-business product.

But one wonders whether hosted IP PBX, hosted IP telephony or unified communications as a service (you can pick your preferred nomenclature) has passed an important inflection point, at least in the U.S. market.

At the moment, hosted IP telephony providers seem to be seeing relatively strong double-digit rates of growth, at least in the U.S. market, with an average of about 20 percent revenue growth, per year. Even if one concedes that some of that growth comes from a low installed base, that is healthy.

That growth would stand in some contrast to some estimates of broader unified communications and collaboration revenue growth, which by some estimates continues to be a slow-growing market or alternatively a smallish segment of the communications or information technology markets.

Of course, it always is difficult to ascertain with precision what revenue elements get included in the UC and C market. Many such estimates, especially in the smaller business market, include access revenue, since the broadband connection is bundled with the unified communications features and voice service.

Still, the reported 20 percent growth for hosted voice suggests it is possible an important adoption hurdle has been leaped.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

On Second Anniversary of Steve Jobs Death, His Approach to Product Development Remains Singular

On the second anniversary of Steve Jobs' death, we might reflect on one attribute of Apple's product development process that continues to strike some of us as highly unusual, for a company of its size and influence.

On the second anniversary of Steve Jobs' death, we might reflect on one attribute of Apple's product development process that continues to strike some of us as highly unusual, for a company of its size and influence.If you have spent any time working with organizations that create products or services, you know that it typically is considered valuable and reasonable to ask customers and prospects what they want from the product, and then try to create those features for them.

That takes the form of informal meetings with buyers and most other forms of market research. Unusually, Apple under Steve Jobs did not actually act that way, which is shocking.

"Some people say, 'Give the customers what they want,' Jobs said. "But that’s not my approach."

"Our job is to figure out what they’re going to want before they do," said Jobs.

"People don’t know what they want until you show it to them," Jobs famously said. "that’s why I never rely on market research."

That is a highly unusual, perhaps singularly unusual way of thinking about, and creating products. I can't think of a single other company that actually operates that way.

People will argue about whether Apple created new markets or only reshaped them. Nobody will argue that Apple won or lost based on a misreading of market research. It never really relied on user feedback.

If you want to argue about whether some other company is "the new Apple," you would have to show me that such a firm has such a profound confidence in its own understanding and abilities that it will create without benefit of being "lead by customers."

Observers will differ about whether Apple can ever be the same company, after Steve Jobs. People will disagree about whether Apple can sustain its ability to envision and execute on industry-creating products.

What most might agree upon is that no other large enterprise actually develops its products by envisioning what people will love, rather than asking them what they want.

Granted, business to business markets arguably are different from consumer markets. But the extreme rarity of the Apple approach ("we know best") is among the enduring Apple legacies.

That "end users don't know what they want" approach is fundamentally foreign to B2B developers, virtually all of the time. Rational developers ask customers and prospects what they want, and try to give it to them.

There's a role for that, of course. What remains unclear is whether disruptive new products get created that way.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

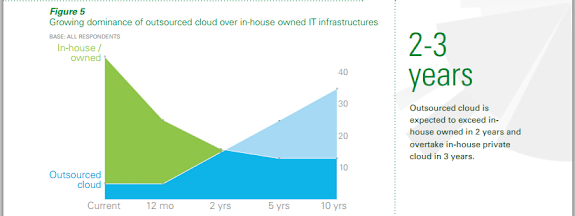

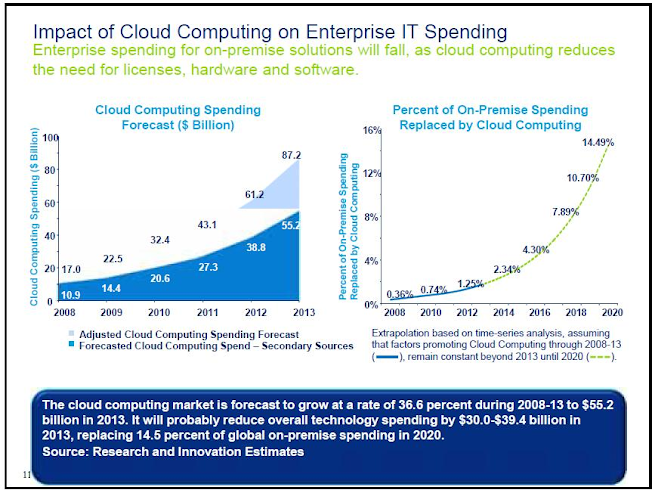

Cloud Computing Inflection Point?

If the predictions of a new Vanson Bourne study prove accurate, enterprise use of cloud computing in the United States, Canada, United Kingdom, Germany, Japan, Hong Kong and Singapore already has passed an important adoption inflection point, and is entering a phase of rapid majority enterprise adoption.

In fact, though 65 percent of surveyed organizations now use on-premises, owned and operated computing facilities, the study suggests we are but two years away from a situation where where cloud and in-house approaches briefly are equal, followed just three years later by dominance of cloud computing.

Also, the study suggests enterprises will outsource nearly 70 percent of their information technology infrastructure by 2018, almost a complete reversal of the present practice, where about 65 percent of enterprises operate using internal and owned facilities, according to a new study by CenturyLink-owned Savvis.

That rate of adoption might strike some as implausible, suggesting that the Savvis-sponsored study includes a disproportionate share of early adopters. But the findings will make more sense if public cloud adoption is considered.

The study suggests adoption of public cloud approaches in fact has not yet hit the 10-percent threshold, even if private cloud, colocation and managed services already have passed the inflection point, using the 10-percent standard.

That would be a major shift in virtually any industry, and will happen in just five short years, the study suggests. At the end of that period, enterprises in the studied countries will have shifted largely to use of outsourced cloud facilities as the dominant model, where today most operate internal facilities.

In fact, the study found that just five percent of enterprise respondents surveyed today depend on the outsourced cloud for the bulk of their IT resources. The shift to an outsourced, cloud-based model will represent the majority of organizations within about three years, the study suggests.

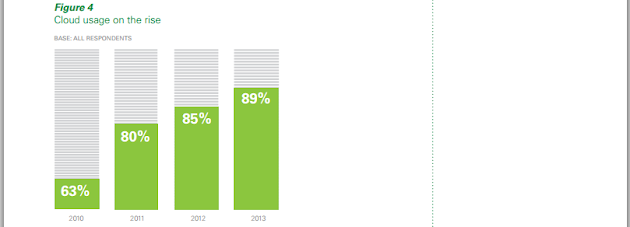

In 2009, about 60 percent of respondents said cloud would be a priority for their organizations at some point in the future, but 71 percent said it wasn’t near the top of their current list.

In 2010, 63 percent of organizations had started to use a cloud solution of some kind. By 2012 85 percent of respondents had some cloud apps in use.

In 2013, 89 percent of survey respondents reported that they are using at least some cloud apps. That suggests the next wave of growth will come from organizations that start to use cloud for additional apps that are more crucial.

Most organizations will use hybrid approaches to colocation and managed-service models, the study also suggests.

"The next five years will bring a dramatic shift in the way organizations approach IT," said Jeff Von Deylen, president, Savvis. "Clearly, cloud is part of the picture but it's not the whole picture. As businesses grow and move more IT infrastructure to outsourcing providers, they will adopt a strategic mix of colocation, managed-hosting and cloud services."

That is a classic case of non-linear adoption of a new technology, once an inflection point is reached.

But some might view the projection as unusually aggressive.

Most successful consumer technologies, for example, do experience a more-rapid adoption curve after the point where 10 percent of households have adopted. Cloud computing, if the new survey is characteristic of all enterprises in the studied countries, passed that threshold sometime before 2010.

After the 10-percent adoption threshold, the adoption rate dramatically accelerates.

But that is the issue. Does the sample survey represent all similar enterprises in the markets studied? And does the adoption of cloud technology represent the use of on-premises data centers, use of full cloud apps, volume of usage across all apps or volume across the mission-critical apps? There is much room for interpretation on that score.

Other forecasts are significantly less robust, at least measured as a percentage of total IT spending.

Savvis commissioned research firm Vanson Bourne to conduct the survey of 550 IT decision

makers in the finance, media and entertainment, retail, healthcare, software and automotive industries.

Respondents generally report they have been outsourcing applications that are not mission critical. Up next are data-center facilities, storage and content-management applications, the study said.

Though in-house IT infrastructure models are most common today, colocation becomes the environment of choice in two years, managed services take the lead in five years and cloud eclipses all forms shortly thereafter, the study suggests.

As you would expect, while the top benefit of IT outsourcing remains "cost reduction or containment," said to be important by 42 percent of respondents, "improved quality of service" and "infrastructure scalability and flexibility" also rank high on the list of advantages, with each indicated "important" by more than 35 percent of survey respondents.

Nearly 90 percent of respondents say they use some type of cloud service today, with more than half doing so for storage and email applications. Slightly less than half of IT leaders employ cloud for intranet, website and microsite applications.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

AI: Correlation is Not Causation

Is productivity higher for people and firms that use artificial intelligence software? And, if so, did the AI "cause" the changes?...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...