It appears that much of the hysterical reaction to a U.S. Appeals Court ruling in Verizon v. FCC willfully or inadvertently confuses two very different principles: actual blocking of lawful content by an Internet access provider, and quality of service mechanisms.

They aren't by any means exclusive, anti-consumer or damaging to application provider ability to innovate, though they create business advantages, as do content delivery networks.

But you haven't heard anybody at all argue that CDNs should be outlawed because they lead to "blocking" of end user access to lawful applications. Content delivery networks improve end user quality of experience.

And, yes, unless a content provider or application provider creates or pays for CDN services, that quality of packet delivery feature is not available. But it is a choice.

Some app providers use CDNs, but probably most do not. CDNs have not destroyed the openness of the Internet. CDNs are not "blocking."

Everybody agrees, from the Federal Communications Commission to the smallest U.S. ISP, that lawful applications cannot be blocked. The FCC has, as part of its Open Internet Principles, stated in plain language that lawful applications cannot be blocked, period.

In the one or two instances where actual blocking ever has occurred, the Commission worked quickly to intervene. So the FCC already has shown its lawful authority to prevent content or application blocking.

"Blocking" is not the issue. Quality of service is the issue, as CDNs are about quality of service as well.

Many of us would argue that application and content providers have the right of freedom of speech. They should not be interfered with simply because a government or private entity is irritated by what they say or the lawful services they provide.

That remains true whether or not any application owner chooses to use a CDN or not. No freedom is lost, either way, whether you believe the "right to freedom" protects the speaker, or the audience.

The "best effort" Internet exists side by side with the existence of quality of service mechanisms that ensure packet delivery in an expedited way. Today. Now.

So long as the best effort Internet continues to exist, and all ISPs support that principle because the FCC says they must, freedom is maintained.

But it is untruthful--simply untruthful--to argue that the best effort and expedited packet delivery access do not already coexist, today, with no apparent ill effects.

Saturday, January 18, 2014

Even Relatively Balanced Net Neutrality Commentaries Miss the Point

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, January 17, 2014

Will Video Break Mobile ISP Economics and Business Model?

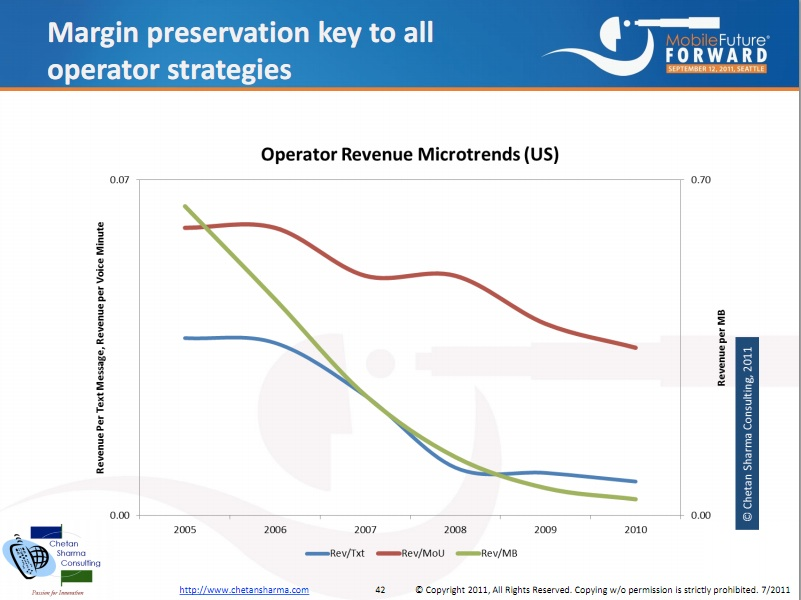

It is easy enough to explain why video entertainment consumption poses a huge--some would say nearly fatal--challenge to mobile operators: there if a fundamental mismatch between revenue and bandwidth required to deliver narrowband services (voice, messaging) and that required to support full-motion video.

Simply, revenue per bit for messaging and voice can be as much as two or more orders of magnitude higher than for full-motion video or Internet apps.

The revenue per bit problem is easy to describe. Assume a fixed network ISP sells a triple-play package for a $130 a month retail price, where each component--voice, Internet access and entertainment video--is priced equally (an implied price of $43 for each component).

How much bandwidth is required to earn those $43 revenue components? Almost too little to measure in the case of voice; gigabytes for Internet content consumption and possibly scores of gigabytes for video.

By some estimates, where voice might earn 35 cents per megabyte, revenue per Internet app might generate a few cents per megabyte. At one level, a network engineer might argue that such fine distinctions do not matter. The network has to be sized to handle the expected load.

McKinsey analysts have argued in the past that a 3G network costs about one U.S. cent per megabyte. The problem, in many developing markets, is that revenue could drop to as little as 0.2 cents to 0.4 cents per megabyte, for any mobile Internet usage.

That implies a strategic need to reduce mobile Internet costs to as little as 0.1 cent per megabyte, or an order of magnitude. Tellabs similarly has warned about revenues per bit dipping below cost per megabyte, leading to an "end of profit" for the mobile business.

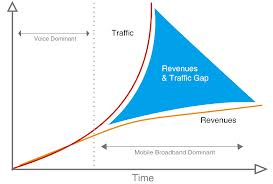

Of course, all of that analysis occurred under conditions where it was web browsing that largely represented Internet bandwidth demand. Streaming video is another order of magnitude or two orders of magnitude sort of problem, though, in part because it is so hugely bandwidth intensive and because it will represent as much as 70 percent of all Internet bandwidth consumption, in a few short years.

Consider the wide variance in revenue per bit represented by a few different potential mobile Internet use cases.

One use case is a $20 a month smartphone data plan and 2GB of usage, representing retail revenue of $10 per gigabyte.

A Netflix subscription generates no direct revenue but could represent network consumption of between a few gigabytes and 30GB of traffic, if usage approaches fixed network levels. Revenue arguably is zero dollars per gigabyte.

A Netflix subscription generates no direct revenue but could represent network consumption of between a few gigabytes and 30GB of traffic, if usage approaches fixed network levels. Revenue arguably is zero dollars per gigabyte.

A work environment might represent $100 a month revenue and consumption of between 10 GB and 50GB. So revenue might range between $2 to $10 per gigabyte.

And that’s the problem with video: much of it does not actually represent revenue for the ISP. But even if it does, what is the revenue and cost per gigabyte? Even if one assume use of one hour of standard definition video, and that product is owned by the ISP, revenue might be $1 to $2 per gigabyte.

Some would argue the cost per gigabyte for a mobile ISP is higher than that. And it is almost nonsensical to think that a standard linear video service, representing perhaps $40 to $80 a month of revenue, will fare well if viewing habits in the mobile realm are what they are in the fixed network realm, where it might not be uncommon to have a single device receiving content for four to six hours a day, representing consumption of perhaps 4 GB to 6 GB per device.

And that assumes only one user, or one stream, is in use. In a multi-user household, demand could be two to three times that amount. In that case, hundreds of gigabytes would be the account load for a single month.

That will destroy revenue per bit metrics, unless you believe consumers really will pay $200 to $400 a month--or more--in mobile Internet access charges, to say nothing of the actual retail price of the content service.

Marketers might argue that revenue per account is what matters, for a multi-product business. That is true, up to a point. An ISP might fare okay if providing a mix of products with disparate revenue per bit values.

Marketers might argue that revenue per account is what matters, for a multi-product business. That is true, up to a point. An ISP might fare okay if providing a mix of products with disparate revenue per bit values.

The revenue earned from text messaging is almost arbitrarily high, as SMS is a byproduct of using the signaling network. Voice revenue might be moderately high, if users can be coaxed or compelled into paying for access to the feature, rather than for usage.

Ericsson hs calculated the cost per bit for a mobile network at about one Euro per gigabyte. So total revenue per bit has to exceed that cost.

Heavy video consumption--especially of third party content-- is likely to exceed cost per bit under almost any scenario.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Deutsche Telekom Puts T-Mobile US Asset Where a Sale Would be More Advantageous

Deutsche Telekom has transferred its 67 percent stake in T-Mobile US into a different holding company offering tax advantages in the event of a sale of T-Mobile US. That doesn't mean any sale is imminent, but does suggest it is viewed as a reasonable development by Deutsche Telekom.

Soon, the attention will shift to which buyer emerges, and then whether U.S. regulators will allow the transaction to proceed. Deutsche Telekom has been there before, as the proposed AT&T acquisition was abandoned because of regulatory and antitrust opposition.

It won't be especially easier this time around, either.

Soon, the attention will shift to which buyer emerges, and then whether U.S. regulators will allow the transaction to proceed. Deutsche Telekom has been there before, as the proposed AT&T acquisition was abandoned because of regulatory and antitrust opposition.

It won't be especially easier this time around, either.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

To "Move the Needle" on Market Share, Mobile Carriers Must Win"Family" Plan Accounts

Over the past decade or so, a big change in retail mobile service plans has happened. In the business as a whole 68.5 percent of postpaid customers are on family plans. Just 26 percent of plans are “individual” plans.

About five percent of the market consists of business-paid accounts.

Verizon has 72 percent of its customers on family plans and seven percent on corporate plans.

There are all sorts of practical implications. For starters, any disruptive attack on market share almost has to affect the family plans, since they represent about 69 percent of the customer base.

The other practical matter is that one would get a wrong result when comparing “individual plans” across countries, especially where most of the buyers are prepaid, not postpaid, and where most sales are of “individual” plans, not “family” plans.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Are U.S. Mobile Carriers Customer Bases Differentiated?

It is a commonplace observation that the largest four U.S. mobile service providers are differentiated on the dimensions of churn and average revenue per account. Basically, Verizon Wireless and AT&T Mobility customers churn at half the rate of Sprint and T-Mobile US customers.

But there might also be a significant differentiation based on why customers choose their service providers.

When Cowen and Company analysts asked customers why they chose their service provider, AT&T and Verizon chosen for "network coverage and quality,"

Sprint was chosen for "unlimited data plan and better price," while T-Mobile US likewise was chosen for "better price and unlimited data plan.

The distinctions are clear: customers who value coverage and quality tend to buy AT&T and Verizon. Customers who value unlimited data and price chose Sprint and T-Mobile US.

So the question, assuming you believe a big marketing war will escalate, is how big each of those customer segments are. For that might limit the gains either Sprint or T-Mobile US can gain and hold, over the long term.

It will be easier for AT&T and Verizon to match price offers than for T-Mobile US and Sprint to dramatically expand their footprints.

But all that assumes no major change in market structure. With the possibility that something happens with T-Mobile US (merger with another provider), and if Dish Network does enter the market, along with activation of assets from one or two of the mobile satellite firms that want to repurpose their mobile satellite spectrum, tomorrow's market could look different.

But that will occur within a context where it appears customers fall into two broad camps: buyers who value coverage and quality, even at higher price; and customers who value unlimited usage and want lower price.

Coverage might not matter for the latter, while lower price, while helpful, still is not why the former customers make their fundamental choices.

How much the contestants can structure their operations to attract the "other" type of customer will become a bigger issue.

But there might also be a significant differentiation based on why customers choose their service providers.

When Cowen and Company analysts asked customers why they chose their service provider, AT&T and Verizon chosen for "network coverage and quality,"

Sprint was chosen for "unlimited data plan and better price," while T-Mobile US likewise was chosen for "better price and unlimited data plan.

The distinctions are clear: customers who value coverage and quality tend to buy AT&T and Verizon. Customers who value unlimited data and price chose Sprint and T-Mobile US.

So the question, assuming you believe a big marketing war will escalate, is how big each of those customer segments are. For that might limit the gains either Sprint or T-Mobile US can gain and hold, over the long term.

It will be easier for AT&T and Verizon to match price offers than for T-Mobile US and Sprint to dramatically expand their footprints.

But all that assumes no major change in market structure. With the possibility that something happens with T-Mobile US (merger with another provider), and if Dish Network does enter the market, along with activation of assets from one or two of the mobile satellite firms that want to repurpose their mobile satellite spectrum, tomorrow's market could look different.

But that will occur within a context where it appears customers fall into two broad camps: buyers who value coverage and quality, even at higher price; and customers who value unlimited usage and want lower price.

Coverage might not matter for the latter, while lower price, while helpful, still is not why the former customers make their fundamental choices.

How much the contestants can structure their operations to attract the "other" type of customer will become a bigger issue.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Spectrum Management Heading for a Historic Change

Spectrum not only is the foundation for all wireless and mobile services, it is a foundational matter for would-be service providers. And big changes are coming.

New spectrum formerly used for TV broadcasting is being reallocated to mobile communications. And at least some of that reallocation process will involve methods of adjusting the behavior of networks and devices dynamically, based on interference issues.

New thinking is happening about sharing existing spectrum as well. It simply is too expensive and time-consuming to conduct widespread "clear and auction" operations across much of the communications-capable spectrum below 3 GHz.

So much attention now is focused on how existing licensed users can be persuaded to share their frequencies with new commercial users as well. Incentives will play a key role: existing licensees will have to see clear financial benefits for doing so, and since so much licensed spectrum below 3 GHz is licensed to government and military users, such incentives will be tricky.

And the ways mobile operators use mobile licensed spectrum, unlicensed spectrum and fixed network assets is changing. Already, even without formal business relationships, perhaps 60 percent to 80 percent of mobile device Internet access occurs on Wi-Fi connections.

Some would say that reveals a key strategic weakness for mobile operators, whose costs of providing Internet bandwidth are too high to survive massive adoption of mobile video consumption.

And though there is more attention paid to global standards, the U.S. market will in some ways remain a bit different.

In some ways, the continental-sized U.S. market has allowed the U.S. communications business to develop based at times on local standards not shared with most of the rest of the world. The primary past example is use of CDMA air interfaces alongside GSM, where in most of the rest of the world GSM was the sole standard.

Frequency plans within the United States will be the salient example of this in the next phase of the mobile business, as most of the rest of the world tries to create a common 700-MHz band for mobile communications across Europe, Africa, Asia and Latin America.

Once again, because of past spectrum allocation decisions, the U.S. will remain a market without full frequency harmonization with most of the rest of the world. How important that might be is not so clear, though.

Global frequency coordination is helpful for manufacturers, as it allows more scale when developing handsets. It is helpful for international travelers who then can roam almost at will when traveling (assuming they don’t mind the international tariffs).

But advances in radio agility are important. In principle, it is possible to equip a device for frequency agility that can compensate for different frequencies used in different countries. And since all mobile carriers have agreed on Long Term Evolution as the common air interface standard (even if there are differences in modulation), frequency might ultimately be less an issue.

The issue for European regulators and industry concerns is whether the 2012

World Radiocommunication Conference of 2012, which decided to open up the 700MHz band across the EMEA region for mobile communications, will be able to come up with enough consensus to allow a further decision at the 2015 WARC meeting.

Of course, that process will be contentious, as TV broadcasters will have to be induced to surrender their use of spectrum to mobile interests. That has not proven easy, wheneve it has had to happen.

But such decisions now are among the growing range of ways national regulators are playing a fundamental role in setting the stage for the next phase of mobile communications growth. Though observers might disagree on how much additional spectrum is required, nearly everybody believes more spectrum will be needed.

And much of the focus will be on ways to find new ways to use spectrum already licensed for some other purpose, to some other users, as very little of the spectrum most useful for communications actually is unclaimed. That means a historically new look at ways to enable sharing of licensed spectrum, more use of frequency-agile networks and devices, and a new business role for unlicensed spectrum.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, January 16, 2014

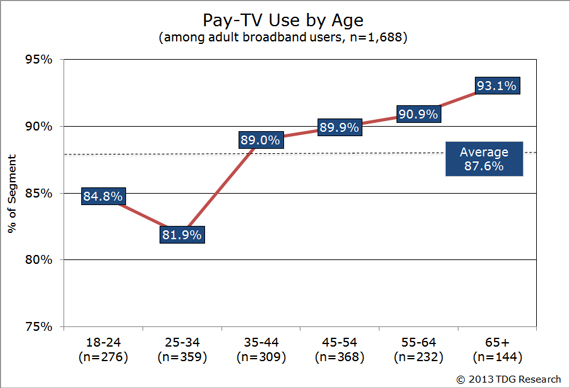

Erosion of Subscription Video is About 1% a Year

The strategic problem faced by traditional video subscription services is not that massive customer desertion is happening now. In fact, attrition, though real, is rather low at the moment.

According to The Diffusion Group, nearly 88 percent of all adult broadband Internet access users in the United States subscribe to a cable, satellite, or telco-TV service.

“The notion that we’re on the edge of a ‘mass exodus’ from incumbent pay-TV services to online substitutes is not supported by the data,” says Michael Greeson, co-founder of TDG and director of research.

The longer term problem is that younger consumers do not seem to buy the product as heavily as older consumers. And unless that changes, trouble lies ahead.

For example, TV subscription rates among those 25 to 34 are 82 percent, and 85 percent among those 18 to 24.

Note that the TDG metric is adoption of subscription TV among “broadband households.”

Of course, since household adoption of broadband Internet access is itself a percentage of all occupied U.S. homes, the adoption of video entertainment services as a percentage of all occupied U.S. homes might be lower than 88 percent.

U.S. broadband penetration is estimated at 78 percent of U.S. homes. If 88 percent of those homes buy a video service, then video penetration hypothetically (some homes buy video service but not broadband or dial-up access) could be as low as 69 percent.

Nobody believes video subscription rates are that low, estimating that more than 102 million U.S. homes actually buy a subscription. That compares to about 115.6 million TV households altogether, including homes that only watch over the air TV.

If there are about 130 million occupied homes, that implies video subsription penetration of about 78 percent, oddly enough the same penetration rate as broadband.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

Enterprise Leaders Say They Now Use Generative AI Tools Routinely

A new survey by the Wharton School (University of Pennsylvania) Human-AI Research suggests that enterprise leaders now use generative arti...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...