Are there any “dominant providers” of fixed network voice services? One might argue that particular concept, as it applies to “voice service regulation,” is way out of date, and does not reflect reality.

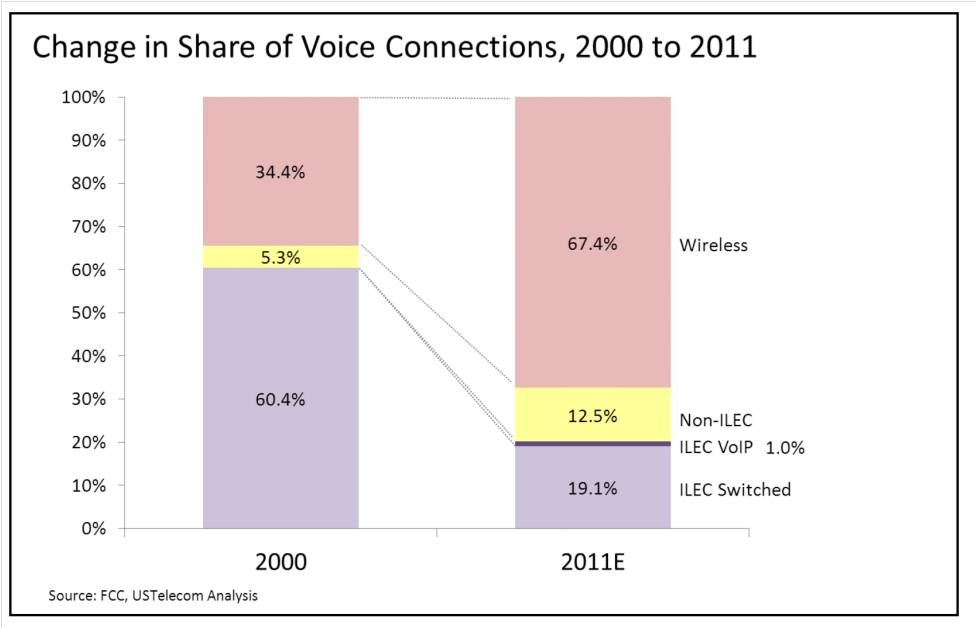

Mobile is the way most U.S. consumers use “voice services,” and new providers--mostly cable TV providers--are the leading providers of fixed network voice services.

Also, high speed access has emerged as the strategic foundation for tomorrow’s business, not voice.

There, one might arguably maintain that cable TV operators are the dominant providers.

The top cable companies accounted for 83 percent of the net broadband additions in the first quarter of 2014, according to Leichtman Research Group.

Looking only at the 17 largest cable and telephone providers in the US, which serve about 93 percent of all high speed access customers in the U.S. market, about 1.2 million net additional high-speed Internet subscribers were added in the first quarter of 2014.

The top cable companies added about 970,000 subscribers, while the top telephone companies added about 200,000 net new subscribers.

Given enough time, that will lead to cable TV domination of high speed access in the U.S. market.

The 17 firms collectively serve about 86.5 million accounts. Cable TV firms have about 59 percent of the installed base, serving 50.3 million accounts, while telcos serve 35.2 million customers, representing about 41 percent of the installed base.

In other words, eventually, is it possible that the dominant providers in most markets could be cable TV operators, or other independent providers, such as Google Fiber. At that point, if telcos are laggards in both voice and high speed access, any regulation of them as “dominant” providers will be misplaced.

Of course, telco leadership of the mobile market will have to be considered, in an overall sense. But regulation of telco fixed network services already is growing strained, given the ongoing shift of market share leadership to new providers.

Suppliers with a wholesale access revenue model will want regulation to continue. Others might argue wholesale obligations should be applied to all access providers. The facilities-based providers obviously would prefer that nobody have wholesale access requirements.

One way or the other, change will have to come.