Sprint reported improved churn performance and improvement in its net account additions, with a small loss for its first quarter of 2015, ending in June 2015.

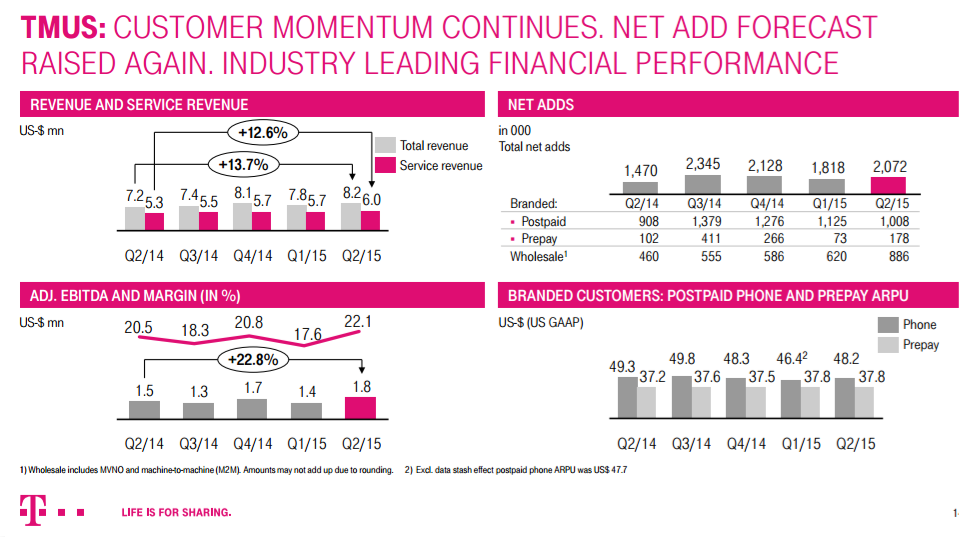

But some also would note that, for the first time in recent memory, the market share rankings for the top-four U.S. mobile providers actually changed, with T-Mobile US becoming the third-largest U.S. mobile service provider, while Sprint slipped to fourth.

Sprint now has 57 million customers, while T-Mobile US with 58.9 million. T-Mobile US gained two million net new customers while Sprint added only 675,000.

For the most part, the quarter was a continuing saga of reversing prior operating trends. Sprint platform postpaid churn of 1.56 percent was a record low, with total net additions of 675,000 accounts.

In addition, the company reported net operating revenue of $8 billion, operating income of $501 million and Adjusted EBITDA of $2.1 billion.

Sprint also raised guidance for its fiscal year 2015 Adjusted EBITDA outlook from the previous expectation of $6.5 to $6.9 billion to $7.2 to $7.6 billion, excluding any accounting impacts from potential lease financing.

Postpaid net additions of 310,000 compared to net losses of 181,000 in the prior year quarter, with an improvement of 491,000 year-over-year.

For the first time in nearly two years Sprint recorded monthly postpaid phone net additions in both May and June.

This marked the fifth consecutive quarter of sequential improvement and compared to losses of 620,000 in the prior year quarter.

The 608,000 year-over-year improvement was driven by lower churn and a 13 percent increase in gross additions, including a 47 percent increase in gross additions with prime credit quality, Sprint said.

Sprint also said it was net port positive for the second consecutive quarter, meaning it activated more transferred accounts than it lost to other providers.

On the Sprint branded platform, total net additions of 675,000 compared to net losses of 220,000 in the prior year quarter.

The 895,000 year-over-year improvement was mostly driven by fewer postpaid phone customer losses.

Prepaid net losses of 366,000 compared to net losses of 542,000 in the prior year quarter.

Wholesale net additions of 731,000 compared to 503,000 in the prior year quarter. The year-over-year growth was mostly driven by connected devices.

Still, operating revenues of $8 billion decreased nine percent year-over-year as consolidated adjusted EBITDA of $2.1 billion grew 14 percent from the prior year period.

Operating income of $501 million was relatively flat from $519 million in the year-ago quarter as higher depreciation expenses offset the growth in Adjusted EBITDA.

Net loss of $20 million, or loss per share of $.01, compared to a net income of $23 million, or earnings per share of $.01, in the year-ago period primarily due to higher interest expenses.