Facebook’s Internet Basics initiative now plans to test demand for Wi-Fi in 100 Indian villages. As always, sustainability is an issue.

Initially, Internet Basics will help create service in 25 villages, buying bandwidth from BSNL for a minimum period of three years, allowing time to test the extent of demand for a “for-fee” service.

Internet Basics has partnered with an Indian rural Internet access provider, AirJaldi, to manage the operation of the “Express Wi-Fi” service.

As currently configured, Express Wi-Fi costs 10 rupees, or about 15 cents, for one day’s access to 100 megabytes of data. For $3, users can buy use of 20 gigabytes of data, which can be used over the course of a month.

There are, according to Professor Rekha Jain, of the Indian Institute of Management, 640,000 villages in India, containing 180 million houiseholds.

Those households hve monthly household income of US$230, with US$24 a month in per person spending.

So part of the challenge is convincing those consumers they should spend money buying Internet access. By way of comparison, the typical Indian mobile account repersents a bit less than US$2 a month in spending.

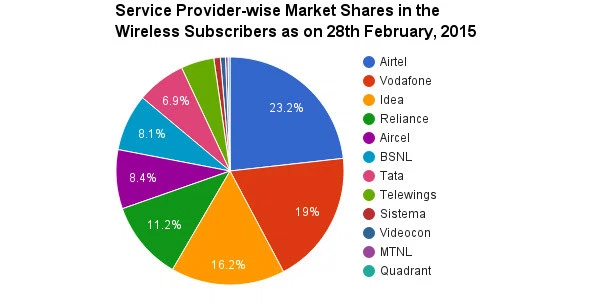

The government of India has said it will create facilities offering public Wi-Fi in 2,500 cities and towns across the country over three years, with the network built and operated by state-owned Bharat Sanchar Nigam Ltd (BSNL).

Use of Wi-Fi as an Internet access platform in India is growing, even if that might seem a difficult proposition in country with fixed network facilities. BSNL is among those who now are deploying public hotspot networks.

The city of Delhi also separately is working on a municipal Wi-Fi plan of its own, that might use a freemium business model.

For its part, Bharti Airtel Limited (Airtel) announced that Uber riders across India will be able to pay for their trips using Airtel Money, the firm’s mobile wallet service. As part of that plan, Uber vehicles will be outfitted with Airtel 4G connections, offering free Wi-Fi inside Uber vehicles.