In 2015, the average U.K. household buying fixed network Internet access consumed 82 GB of data each month, a 41 percent increase compared to the 58 GB per month recorded in June 2014.

Higher consumption of over the top entertainment video was a driver of the change, as well as faster speeds. As always, faster speeds mean more data can be consumed in any given unit of time. Also, faster speeds mean each household user can consume more data in any given unit of time.

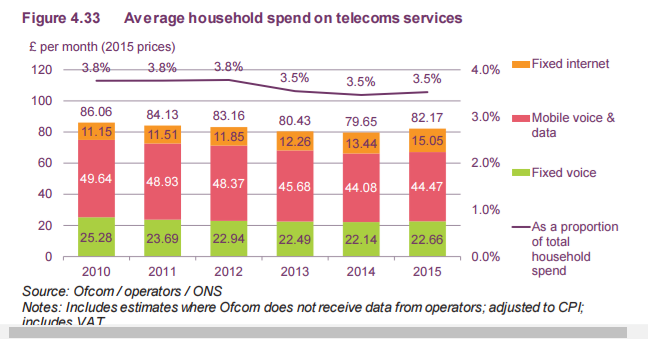

That noted, well over half of all U.K. household telecom spending (54 percent) is for mobile services. Some 18 percent of telecom spending is for fixed Internet access. About 28 percent of spending is for fixed network voice (inflated, to a certain extent, because digital subscriber line service also requires purchase of voice service).

U.K. telecom revenue grew in 2015, up £0.2bn (0.5 percent) to £37.5 billion, propelled by (Figure a £0.5 billion (4.2 percent) increase in retail fixed revenue, itself driven by a 12.6 percent rise in fixed internet revenues. Some 0.9 million more Internet access connections were added in 2015, representing growth of 3.9 percent.

Mobile revenue actually fell 0.4 percent, while wholesale revenue fell 4.2 percent.

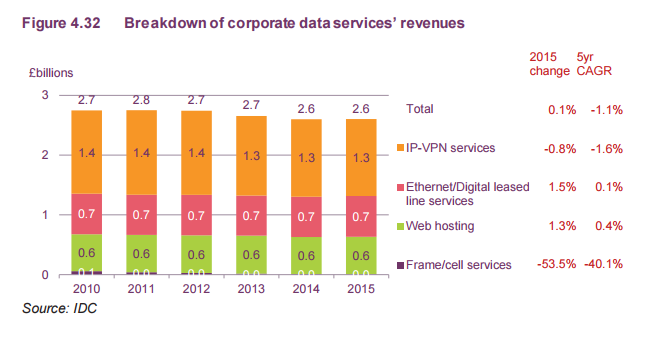

Enterprise data revenue also fell by one percent.

In the consumer segment, average revenue per account drove a 3.2 percent increase in telecom spending.

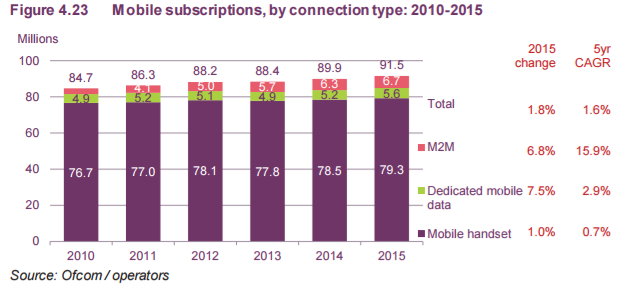

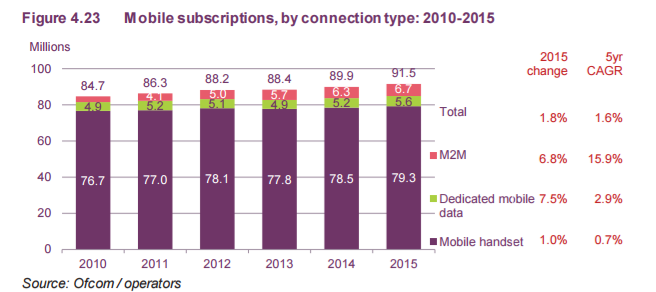

Fixed network voice lines decreased 0.3 million, or one percent. Mobile subscriptions grew 1.8 percent (including machine-to-machine accounts).

Fixed network voice call minutes fell by seven billion minutes (9.2 percent) to 74 billion minutes in 2015 and mobile voice call minutes increased by five billion minutes (two percent) to 143 billion minutes.

The total number of outgoing SMS and MMS messages continued to fall in 2015, down by eight billion messages (7.6 percent) to 101 billion messages, although this was a smaller fall than in either 2013 or 2014, in large part because people are shifting to over the top messaging alternatives.