An argument can be made that a growing number of tier-one service providers cannot invest profitably in their networks, even if markets require ever-more capacity. In the recent past, that might have been thought a problem for fixed network operators. Now it appears to be becoming an issue for mobile operators as well.

An analysis by A.T. Kearny suggests that only the top four players in any Southeast Asian geography are able to earn positive financial returns. More importantly, only the top two players in a geography seem to consistently make returns in excess of their cost of capital. Some have argued that is a problem for firms such as AT&T and Verizon as well, arguably pertaining mostly to their fixed networks.

Researchers at PwC studied the financial performance of 78 fixed-line, mobile and cable operators with a collective annual capex of some $200 billion, nearly 66 percent of the industry’s total spend.

The research found that, over the past decade, the average long-term return on investment (ROI) has been just six percent. That is three percentage points less than the cost of the capital itself. In other words, operating revenue is not covering the cost of capital.

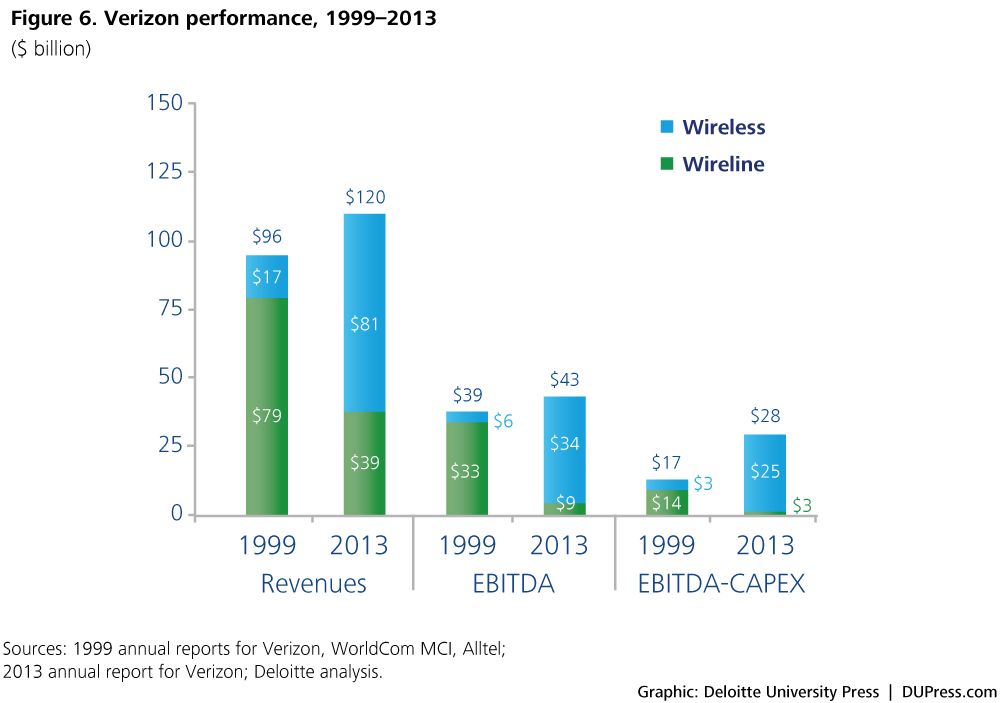

Consider Verizon, which earns very little from its fixed network operations, and almost all earnings from the mobile business, or AT&T, which earns a bit more from its fixed network, but still earns most of its money from mobility services.

In 2013, Verizon generated 21 percent of total earnings from its fixed network, and 79 percent from mobile services.

Mobile represented 68 percent of revenue in 2013, while fixed operations generated 32.5 percent of total revenue. In other words, mobile creates significantly more profit margin than the fixed network.

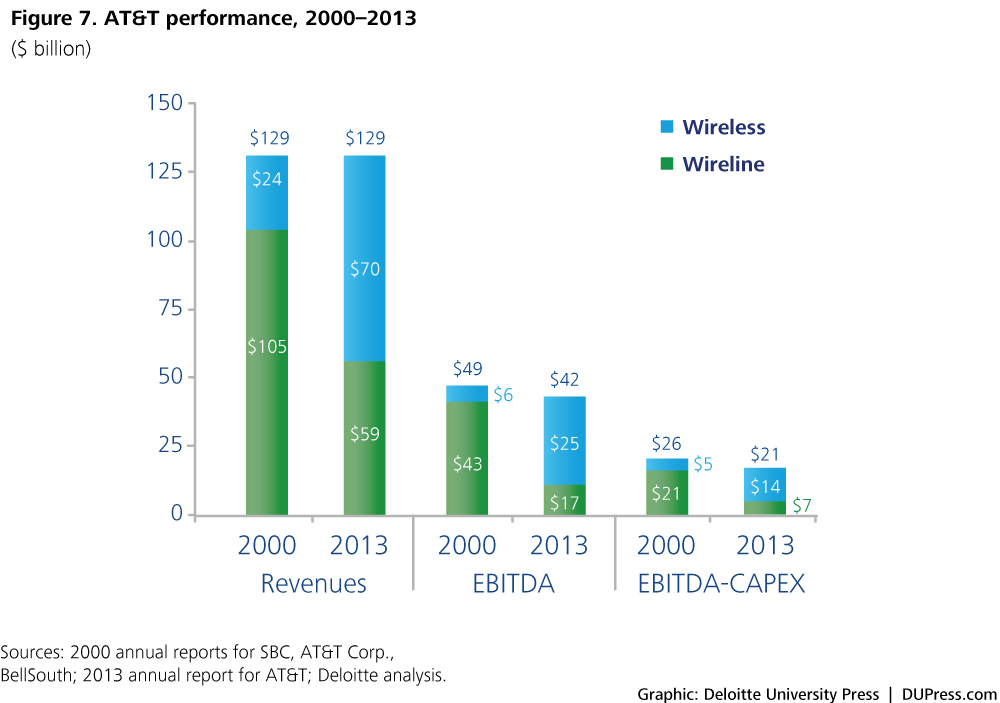

AT&T shows the same pattern, if different magnitudes. In 2013, mobile represented 54 percent of revenue and 60 percent of profit; the fixed network 46 percent of revenue and 40 percent of profit.

And capital intensity seems to be rising.

That mismatch between profit and investment explains why fixed network internet access speeds have lagged, compared to cable operator speeds. A rational executive would invest where there is growth, higher profit and strategic advantage--the mobile network--and harvest the proceeds of the legacy fixed network.

While it is understandable that policy advocates and regulators call for more investment by tier-one telcos in their fixed networks, “how” to make that investment at a profit is the issue. Tier-one service providers with mobile assets long have assumed mobile would lead their businesses. The only issue has been what to do with the fixed assets, which have been declining n value.

Calling for ubiquitous fiber to the home deployment arguably is a losing proposition, as it no longer is clear that investment would ever generate a return.

Other telcos without mobile assets might be able to use new shared spectrum or unlicensed spectrum assets to upgrade using fixed wireless platforms. In some cases, wholesale access might provide an opportunity to upgrade, as well.

What seems rather abundantly clear is that U.S. telcos already have lost the competition with cable companies for leadership of the internet access business. Cable operators have for a few years gained all of the net new additions in the market, and, on average, offer top speeds two orders of magnitude (100 times) faster than what telcos offer.

Most popular advertised service tiers

| ||||||||

Platform

|

Company

|

Speed Tiers (Download)

| ||||||

DSL

|

AT&T DSL

|

1.5

|

3

|

6

| ||||

AT&T IPBB

|

3

|

6

|

12

|

18

|

24

|

45

| ||

CenturyLink

|

1.5

|

3

|

7*

|

10

|

12

|

20

|

40

| |

Frontier DSL

|

1

|

3

|

6

| |||||

Verizon DSL

|

0.5-1

|

1.3-3

| ||||||

Windstream

|

3

|

6

|

12

| |||||

Cable

|

Optimum

|

25

|

50

|

101

| ||||

Charter

|

60

|

100

| ||||||

Comcast

|

25

|

50

|

75

|

105

|

150

| |||

Cox

|

15

|

25

|

50

|

100

| ||||

Mediacom

|

15

|

50

|

100

| |||||

Time Warner Cable

|

15

|

20

|

30

|

50

|

100

|

300

| ||

Fiber

|

Frontier Fiber

|

25

| ||||||

Verizon Fiber

|

25

|

50

|

75

| |||||

Satellite

|

Hughes

|

5

|

10

| |||||

ViaSat

|

12

| |||||||

“Cable based ISPs are driving the growth in new high speed service tiers,” the Federal Communications Commission says. In fact “the maximum advertised download speeds among the most popular service tiers offered by ISPs using cable technologies have increased from 12-30 Mbps in March 2011 to 100-300 Mbps in September 2015.”

“In contrast, the maximum advertised download speeds that were tested among the most popular service tiers offered by ISPs using DSL technology have, with some exceptions, changed little since 2011,” the FCC report notes.