A few skeptics might argue that there is no need for 5G, or that the business model will not work or that consumer demand does not exist. That noted, the movement, globally, seems unstoppable, and for existential reasons. Whether 5G works out largely as planned (it actually produces new revenue streams, business models and applications), it is a gamble that must be taken.

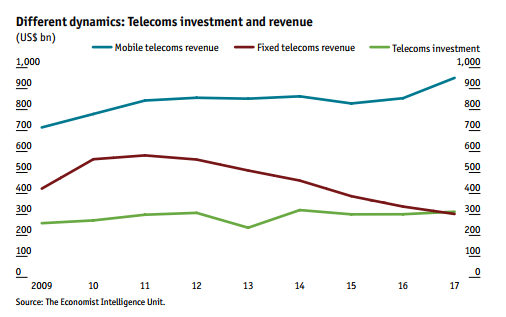

In fact, for fixed network telcos, the odds of failure are growing, as revenue earned from investments increasingly is less than the capital investment.

For that reason, there is a good reason for arguing that either capex or opex, or both must be reduced to match potential revenues earned by those investments.

In fact, the importance of cash flow, rather than other traditional measures of “profit,” indicate the shift. In past years, it was mostly unprofitable startups whose progress was measured in terms of cash flow.

But the big issue is simply that, with all existing revenue sources flat, diminishing or poised to become flat and diminish, the broad telecom industry must find big new revenue sources to replace those being lost, or face decline, if not death.

Since 5G is being purpose built to support new applications (internet of things, machine-to-machine communications, connected cars, fixed line replacement), it is a necessary gamble on the ability to create and sustain big new businesses in those areas.

There can be no certainty, at this point, about the degree of success. What there is certainty about is that doing nothing risks industry failure. So 5G is going to happen. It has to.