For the first time in many decades, the business case for optical fiber access facilities in the U.S. market has changed. In the past, optical fiber was considered necessary to provide entertainment video and higher-speed internet access as retail services to consumers.

Consumer internet access still matters. The issue is how much the business case is changed, and on what scale, if distribution fiber and small cells support wireless access (mobile or fixed), without a full fiber to premises deployment.

In that sense, the question is really the payback from “fiber deep” distribution fiber, plus wireless access, compared to direct fiber to home alternatives, at least for fixed network telcos.

Where mobile carriers operate out of region (without existing fixed access network assets), and all the largest four mobile carriers do so for 100 percent to about 50 percent of the U.S. land mass, distribution fiber arguably is more crucial than access fiber. In other words, fiber to “small cell” locations is necessary.

That, in turn, could enable a fixed wireless strategy.

Just how much all that will cost is unclear at the moment.

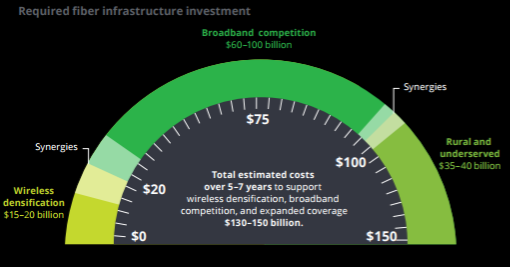

U.S. telecom service providers need to invest between $130 billion and $150 billion in deployment of fiber facilities over the next five to seven years, according to new research from Deloitte, for a variety of reasons.

You would not be surprised if Deloitte sees the bulk of that investment related directly to consumer internet access. What seems to be different is that substantial portions of that investment, plus new fixed wireless opportunities, might allow new financial synergies between the consumer fixed network investment and investment to support the mobile network.

Such synergies might represent some 27 percent of the total fiber investment cost. In other words, the way distribution fiber is laid can cut about 27 percent off the full cost of fiber investment for all purposes (consumer and business, internal and retail services, urban and rural, mobile and fixed uses).

5G services will likely be commercialized on the back of an ultra dense network infrastructure–also fundamental to evolving LTE to support LTE-Advanced and LTE-Advanced Pro features–with a heavy emphasis on small cells.