AI will be good for smaller firms trying to innovate.

Saturday, July 29, 2017

Innovation can be Democratized in Era of Artificial Intelligence and Big Data

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

5G Will be About Enterprise Use Cases

|

|

|

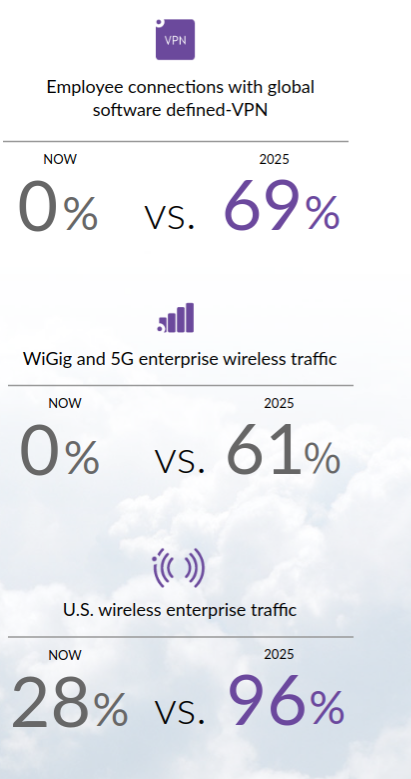

By 2025, the percent of enterprise traffic, now at perhaps 28 percent of total, could reach 96 percent of total, according to Bell Labs.

If you want to know why some of us believe the future for 5G is enterprise use cases, that is part of the reason.

On a separate level, Bell Labs also predicts that as much as 61 percent of all enterprise traffic will be terminated or originated using some wireless mechanism.

If 5G and some variation of Wi-Fi account for 61 percent of traffic, that leaves about 35 percent of total enterprise traffic that is neither 5G nor some form of Wi-Fi, but still wireless.

You might therefore guess that some of that traffic will be fixed wireless local access or some other form of wireless access, including specialized low-power, wide area networks of sensors.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

By 2025, 69% of Enterprise Employees Might Use a Software-Defined VPN

Software-defined wide area networks (SD-WAN) are the current rage in enterprise networking circles, and probably for good reasons. According to Bell Labs, by about 2025, perhaps 69 percent of enterprise employees will be connecting by a software-defined virtual private network, which is what an SD-WAN provides.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Third Telecom Era Approaches

As revolutionary as was the change from telecom monopoly to competition, we appear to be on the cusp of a third era.

For a number of fundamental reasons, “telecommunications” roles are becoming more porous, diffuse and shared. The notion that “anybody can be an internet service provider,” in contrast to “there is only one lawful provider of service,” illustrates the point.

Depending on the use case, an enterprise (public hotspot) or even consumer (cable homespot, mobile tethering) can act as the ISP. For purposes of delivering e-books, Amazon acts as a special purpose ISP. Google and Facebook act as ISPs in a variety of settings and roles. Google Fiber competes directly with telcos and cable companies as a general purpose fixed internet services supplier.

In India, Google and Facebook partner to operate Wi-Fi hotspots in public locations and villages. There may be other roles and platforms in the future.

Beyond that, as we move towards an era of pervasive computing. Value moves inexorably “up the stack,” to applications and use cases, and away from the simple value of internet access.

And that same process also means that traditional telecom apps (voice, messaging, content delivery) can be supplied by third parties, over the top of any specific internet connection. That further increases the potential amount of competition, and therefore will affect potential profit margins.

All that illustrates the point that industry revenue streams and business models are non-exclusive and open to challenge. Declining average revenue per account is one example of the trend. Declining profit margins are another direct result.

That, in turn, drives firm strategy. More scale helps with gross revenue and profit margins. That is why a major global wave of consolidation is likely--or virtually certain--over the next decade.

The U.S. market, for example, has not yet started to consolidate in the same way that India’s market already has started. In fact, it is likely the Indian mobile market will shrink in half, in terms of facilities-based suppliers, within a year, from eight to four.

It is only a straw man, but assume something similar happens in the U.S. market. That would potentially reduce the number of leading suppliers in half (across the fixed and mobile domains). Where there are perhaps nine leaders (across the fixed and mobile segments, including two cable operators, four mobile suppliers and three big fixed network suppliers), there could, over perhaps a decade, be just four left, with varying global roles, as well.

Any way you look at it Sprint, T-Mobile US, Dish Network are virtually certain to be involved in the next big merger wave in the U.S. telecommunications market. Charter Communications or Comcast are possibly going to be involved, as well as a few content firms.

While it remains possible that a Sprint tie-up with T-Mobile US could be proposed, it is not the only combination that makes sense, and many of those other mergers would likely have a better chance of regulatory approval.

That consolidation would mirror similar big market structure moves in India, which long has been among the mobile markets with the most facilities-based contenders.

So far, all we’ve seen in the U.S. market are talks and rumors. But the action is coming, for obvious strategic reasons. As profit gets wrung out of the business, more scale is the short-term answer, at the very least buying additional time and resources to work on the long-term objectives of changing the value proposition.

A reasonable and workable objective is to achieve a balance of “access” and “application” revenues that might approach 50-50. To be sure, nobody has done that yet. Eventually, it is likely to be necessary for survival.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, July 27, 2017

Underestimating Demand is as Bad as Excessive Optimism

The launch of AT&T’s DirecTV Now streaming service reminds me of its launch of the Apple iPhone. As you will recall, the iPhone launch appeared to have caught AT&T somewhat by surprise, in terms of the added usage of its data network.

Roughly the same thing seems to have happened with the DirecTV Now launch. In both cases, customers complained about quality issues that appear related to capacity to support the new services.

You can guess what comes next. AT&T took steps to fix the capacity problems related to iPhone customer behavior patterns, and likely has spent the last few months figuring out how to better support scaling of its DirecTV Now service as well.

You might well expect a renewed growth spurt, as a result. It’s just a reminder of how networks are dimensioned: you have to make assumptions about consumer behavior. Overprovision and you waste capital. Underprovision and consumers will have a troubled experience. It is hard to get it right, for new services that prove quite popular.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

AT&T DirecTV Acquisition Seems to be Working

AT&T’s acquisition of DirecTV was not universally acclaimed when it happened. Some observers said AT&T needed to spend the money on better internet access. Others pointed out that the linear video business already was in decline.

Supporters argued that the move made AT&T a nationwide quadruple play supplier for the very first time. Others pointed out that the free cash flow almost singlehandedly would fund AT&T’s dividend for some time. Some added that the additional scale would improve economics for the firm’s video business now, while creating a much-stronger platform for OTT video to come.

So the new way to reassess that particular choice is whether you think AT&T or Verizon is in a better position, today, strategically.

If you believe all access providers will have to replace half of current revenues within 10 years, the only question is how to do so. In principle, you can make horizontal or vertical acquisitions, invest in new lines of business or grow organically.

Organic growth helps. How much that can help depends on whether a firm can take market share in a market or mostly has to defend its share, whether the markets are mature or young.

An attacking firm with low share always can grow by taking market share from incumbents. New entrants with different cost structures, attacking from “outside” an industry, with different assets, often have a much-easier time than incumbents attacking each other, with the same asset bases.

But most observers would argue that organic growth, in markets that are saturated, does not provide the scale of new revenue, fast enough.

And some critics might say AT&T faces issues with its DirecTV performance, in the form of subscriber losses in linear video. But the DirecTV Now OTT service, despite some issues, seems to have kept the video base at flat levels, in a business that is shrinking.

Average revenue per user is an issue, but AT&T seems to be reaping bundling rewards.

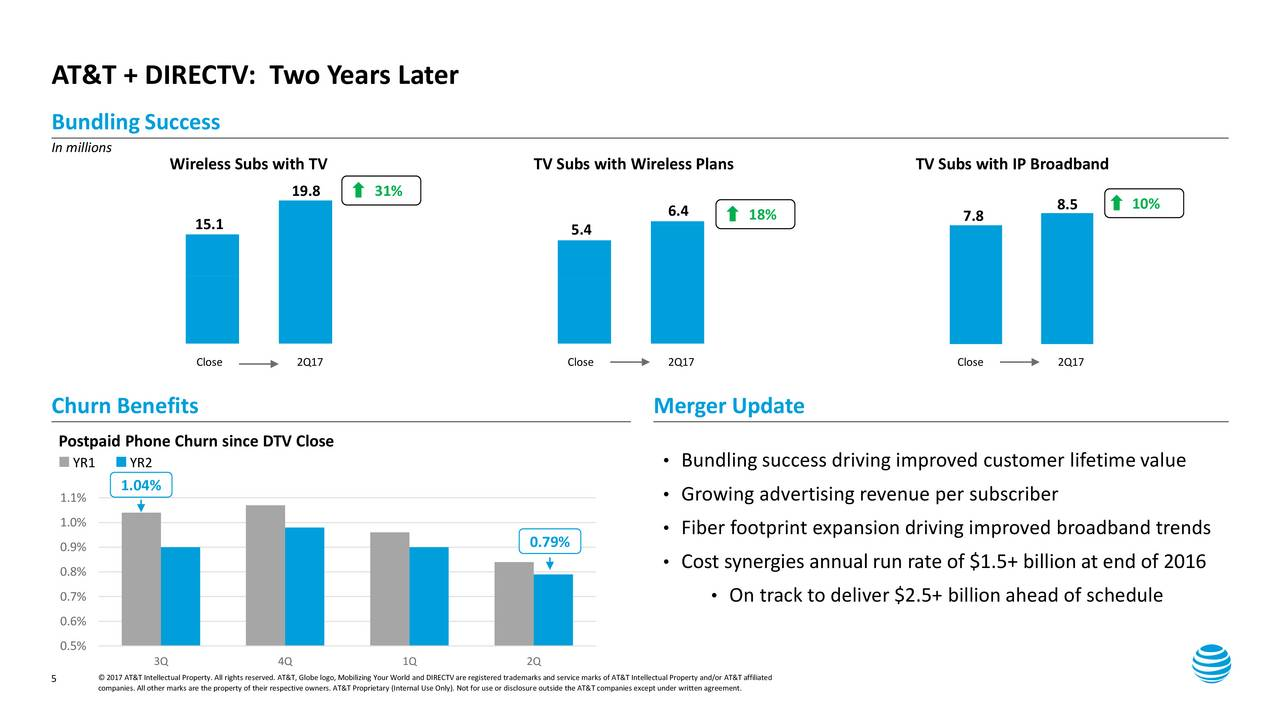

“Half of our DTV Now subscribers are coming from traditional pay-TV, mainly from our competitors, and the other half had no pay-TV service at all,” said John J. Stephens, AT&T CFO.

AT&T has “reached nearly 0.5 million subscribers,” keeping This has the video account base “essentially flat” from year ago levels, he said.

Importantly, the bundling of video and mobile services seems to be working. The number of wireless subscribers who also have a TV service from us has increased by more than 4 million, or up 31%, since the close of the DTV deal. Conversely, TV subscribers with wireless plans have increased by nearly 1 million, or 18%.

The number of mobile subscribers with DTV has increased by 72 percent, while the number of DTV subscribers with AT&T Wireless has increased by 1.7 million, or 52 percent.

The number of DTV subscribers in AT&T’s wireline footprint with IP broadband has grown by more than 2.7 million, to 67 percent of DIRECTV customers, said Stephens.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, July 26, 2017

Go Horizontal or Vertical in Acquisition Strategy?

Access services are a mature market in developed countries, and eventually will become mature even in developing markets, even as new revenue sources are created to replace declining legacy services. That has business consequences.

Most large tier-one service providers (cable, telco, satellite) eventually grow more by acquisition than organic growth. That is not the pattern for smaller firms, but you get the point. In any “mature” market, where accounts are essentially saturated, any provider tends to get account growth mainly by taking an account away from another existing provider.

So supplier consolidation is a long-term process in the global telecom industry. The only question is how fast, and how intense, that process is at any moment in time.

But what sorts of acquisitions make sense? The easy answer has been to make “horizontal” acquisitions to gain scale in the existing business. In other words, acquire more access assets.

That is the thinking when analysts float trial balloons such as Comcast buying Verizon, or Verizon buying Comcast or Charter, or when smaller telcos do the same sort of thing.

At least in the near term, doing so is a faster, surer way to boost gross revenue, and boost profit margins, than investing in “long game” moves “up the stack.”

To be sure, in the near term, such horizontal acquisitions are likely to be the main trend in the global telecom industry (in terms of revenue accretion). Moving up the stack takes time, and might often contribute less incremental revenue than a simple horizontal acquisition.

But taking the “long game” route to moving up the stack is possible.

Consider Comcast, which is among the U.S. access providers with the best execution “moving up the stack.” In the first quarter of 2017, Comcast booked $20.5 billion in total revenue. The access part of the company booked $12,9 billion in revenue, while the NBCUniversal portion of the company generated $7.9 billion in revenue.

So the “up the stack” (content) part of the company represented about 39 percent of revenue, access about 61 percent of total revenue.

If any other major telco could claim it now earns 39 percent of revenue from “application layer” sources, it would be considered a major strategic success.

In the second quarter of 2017, AT&T earned virtually all its $39.8 billion in quarterly revenue from access services. That will change, assuming AT&T’s acquisition of Time Warner is approved.

In the first quarter of 2017, Time Warner booked $7.7 billion in revenue. In other words, after the acquisition, AT&T would earn just about as much as did Comcast in its most-recent quarter. That would boost content revenue at AT&T to about 16 percent of total.

It might not seem like much, but that would mean AT&T earns significant revenue, for the first time, from “up the stack” sources. AT&T of course will eventually want to do the same in enterprise and business areas related to internet of things, for example. But that will take time, both because the IoT market is nascent, and because the available acquisition targets therefore also are small.

Verizon has made a similar, if smaller move, by acquiring first AOL and then Yahoo, to create a new advertising business. In the first quarter of 2017, Verizon booked $29.8 billion in revenue. Revenue from its telematics unit was negligible as a percent of total, while, revenues from the “Oath” unit were not disclosed. The point is that Verizon has not yet gotten to a point where “up the stack” revenues are significant.

But you see the point. Moving up the stack is hard, risky and often not able to move the revenue needle quickly. So the an emphasis on horizontal acquisitions is going to be hard to resist. But if you believe the access business is going to be fundamentally challenged, moves to gain scale in businesses “up the stack” is necessary.

The issue is, how to balance horizontal acquisition that boosts revenue and profit now, with investments in “up the stack” growth. Or, in an ideal scenario, can access providers move up the stack now, by acquiring assets that throw off enough significant current cash flow, to move the revenue needle immediately?

Comcast is the model for the U.S. market.

That illustrates an asymmetry for Comcast and Verizon, if you wantt to speculate on where value might lie, even if the odds of such an event are slim.

Comcast might value Verizon’s mobile assets, significantly growing the amount of its access revenues. But if you think a reliance on access revenues, going forward, is problematic, then Verizon gains more in any acquisition of Comcast, as it immediately gains “up the stack” assets, in addition to greater horizontal scale.

That is why some observers might argue that vertical acquisitions, where the synergy is clear, make more sense than horizontal acquisitions that increase scale in the access business.

Some will argue AT&T erred in buying Time Warner. Some of us would argue it is the right move, to move up the stack, when total revenue includes almost no “up the stack” contributions. If Verizon remains a buyer of assets, not a seller, “up the stack” makes more sense than a horizontal acquisition that simply adds more scale in access.

Some would focus on strategic angles, such as a faster path to “fiber deep” or “bandwidth deep” assets.

Others of us might argue that firms such as Verizon and AT&T, if they wish to remain leaders in the future (and not sell themselves), must create much more “up the stack” revenue. It is the only way to reposition their value in the ecosystem and escape a “dumb pipe,” low value, low margin existence.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

Enterprise Leaders Say They Now Use Generative AI Tools Routinely

A new survey by the Wharton School (University of Pennsylvania) Human-AI Research suggests that enterprise leaders now use generative arti...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...