As it consolidates horizontally, the telecom industry (access service providers of all sorts) also has no choice but to look elsewhere within the internet ecosystem for growth, as “elsewhere” is where long-term growth is to be found.

That is not to downplay the near-term contributions greater scale will make. In the near term, firms will merge to create greater scale. But consolidation will not be enough, over the long term.

“It is no longer appropriate to develop corporate strategies, or to assess policy situations, with a narrow focus on a single segment of the value chain, A.T. Kearney analysts have argued.

For access providers (telcos, cable TV, satellite access providers and other internet service providers), that means looking beyond access services for growth (“up the stack,” mostly).

The reason is that value within the ecosystem is shifting, while participants increasingly are moving into adjacent or other parts of the ecosystem, perhaps nowhere as extensively as in the apps space.

“As players such as Apple, Facebook, and Baidu expand into adjacent segments, their rationale is based on leveraging scale and integrating services and features into their core products and platforms to create barriers to entry,” A.T. Kearney analysts note.

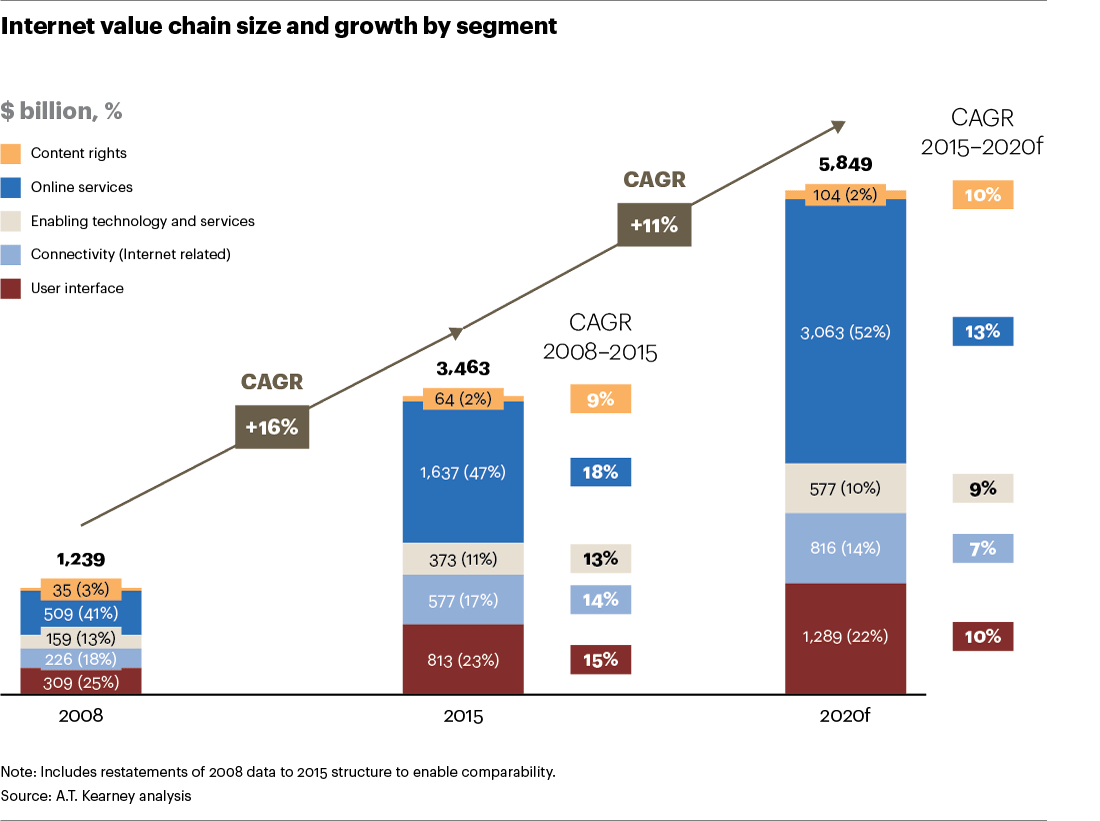

By 2020, perhaps 52 percent of value will lie in applications, while just seven percent lies in internet access. In other words, between 2015 and 2020, the value contribution of internet access will drop 50 percent, as a percentage of total, even if gross revenues climb in many developing markets.

Will early deployment of 5G networks produce gains, and if so, for whom? Some argue that “value” ultimately drives results. If so, then it already is clear that about half of value within the internet ecosystem, as expressed in revenue, lies in applications, about 14 percent in internet access.

So think about 5G. Will early deployment of 5G networks produce gains, and if so, for whom?

Ignoring for the moment broader answers, such as “users, society, the economy were the winners,” and looking only at the “telecom” part of the ecosystem, one might argue 3G was one thing, and 4G another, so 5G might not produce winners where one expects to find them.

The winners might be found disproportionately in the applications or device segments of the business, and less in the network infrastructure or service provider parts of the business, for example, and for different firms in each era.

Roughly speaking, one can argue that 3G produced the biggest winners in the network infrastructure and handset segments of the business, mixed results in the service provider part of the business, and important new inroads by application providers.

One problem is that it is not clear there has been any single killer app, killer use case or killer capability that clearly defines the 3G and 4G eras.

For example, if you had to name a single “killer app” for 3G, what would that be? Some would say there was no killer app for 3G.

So some would say it was “mobile broadband ” or “mobile internet access” was the key advance beyond 2G. And many hoped-for new applications did not materialize in 3G, and arguably only became common features in the 4G era (think video calling).

In fact, some might say text messaging (first introduced by 2G networks) that became something of a killer capability for 3G, even if the 3G network did not introduce it.

Others might say the best example of a killer app was mobile email (think BlackBerry). In fact, it arguably was the rise and fall of that killer app in the 4G era that lead to the demise of Research in Motion (BlackBerry) as a lead force in the devices portion of the ecosystem.

That might lead some to argue it was the “easy to use smartphone” (think Apple iPhone) that suggests the killer feature of 4G networks, or social networking, or multimedia social networking.

Likewise, the killer app for 4G is similarly elusive. Some might argue it was tethering (internet access) that was a killer use case. And it might well turn out that it is entertainment video that ultimately becomes the killer app for 4G.

Right now, we can only guess at whether a 5G killer app, feature, use case, capability or business model might actually emerge. There are two areas where supporters currently believe such developments could occur: internet of things and full substitution for fixed network internet access.

And there is the worrisome 3G precedent: the hoped-for innovation in value and revenue really did not happen until 4G. So it is unfortunately possible that 5G will be more like 3G than 2G or 4G: producing less than hoped for innovation in new services or revenue.

Or, perhaps more accurately, might 5G produce less new revenue than older revenue streams are cannibalized? At a very high level, voice revenue is being cannibalized by mobile data revenue because better mobile internet access means substitute products are available.

The safest bets right now are that internet application providers are going to win, as well as some handset suppliers. Some infrastructure suppliers will benefit, for a while. But it is not so clear that all service providers will win, or will win to the same degree. In fact, there always is the precedent of 3G.

Though the problem with 3G in some markets was operator overpaying for spectrum, and though that is not likely to happen in the 5G era, the business model could still emerge as a big issue.