Tough revenue models are an underappreciated element of the 5G business case. It is easy to toss around notions that the three big buckets of opportunity are mobile broadband for humans; low-latency services and massive internet of things apps.

The problem is that it seems increasingly likely that each potential use case has competition. For enhanced mobile broadband, 4G keeps getting better. As it does, it limits the value proposition for 5G mobile internet access.

Likewise, as important as massive IoT might be, 4G alternatives also are coming to market, and even for low-latency applications, 4G is making improvement in that area as well.

The point is that we might well find, in the early going, that there is not as much incremental revenue from 5G as might be hoped.

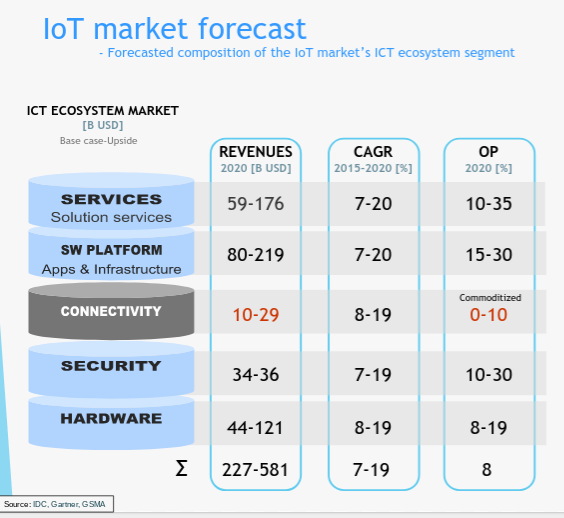

In other words, as important as internet of things and services for non-humans are likely to be for mobile operator revenue models, IoT connectivity revenue is likely to be disappointing for most mobile service providers.

Of a total of US$227 to US$581 billion in total IoT revenue in 2020, perhaps $10 billion to $29 billion will be earned by supplying connectivity services. That represents something between four percent and five percent of industry revenues.

Most of the upside will come from devices, security services, applications and platform services.

|

sources: IDC, GSMA, Gartner, John Kjellemo

|

For some of us, that points out the possible importance of fixed wireless services as an early driver of 5G revenues. In some markets, where there is high demand for fixed broadband connections, but where there also are some challenging gigabit access deployment scenarios, 5G fixed wireless might be the clearest, most tangible new revenue stream to reach any scale.

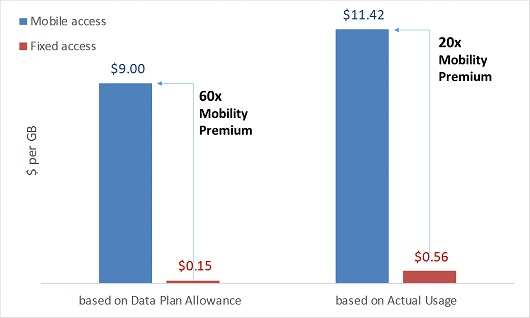

Until quite recently, though stand-alone fixed wireless networks have proven to have a positive business model for wireless internet service providers, in many cases, mobile networks have not been effective substitutes for fixed service to the same extent.

Neither average or peak mobile specs, nor the cost of using mobile data have been anywhere close to comparable to fixed network specs or prices per consumed megabyte.

In fact, fixed network data costs, on a cost-per-megabyte basis, routinely have been in the 20 times to 60 time lower scale than mobile data. Where fixed network data might cost cents per gigabyte, mobile data costs dollars per gigabyte.

Long Term Evolution-Advanced (LTE-A) will prove an important break, in that regard, by offering access speeds more equivalent to fixed networks, at costs more equivalent as well.

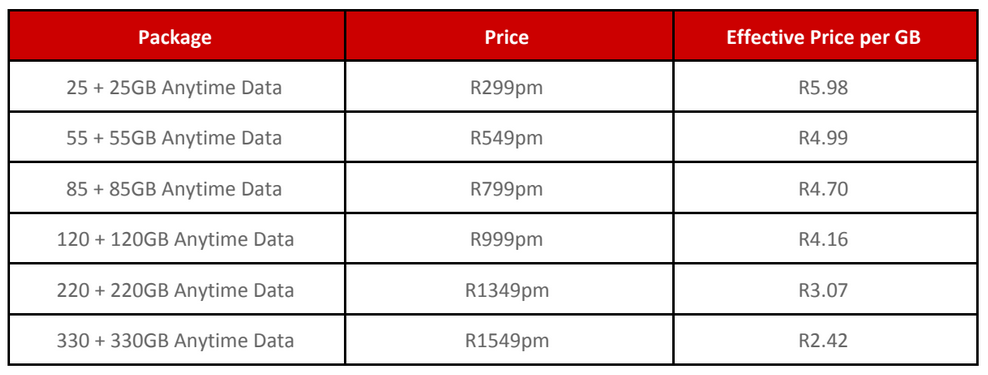

In South Africa, internet service provider Afrihost has created LTE-A usage plans that feature a cost-per-gigabyte of about 18 cents per gigabyte.

For many accounts, that is comparable to the value of a fixed network connection.

Traditionally, mobile and fixed network access have been highly different in their consumption modes, so the new plans are important in that they move in the direction of unified plans with a “mobile” or “per device” character instead of a per-location character.

In some markets, for example, monthly usage allowances for a fixed internet access connection might be in the neighborhood of 300 gigabytes. The new Afrihost plans support that amount of usage, for the biggest usage plans, per device.