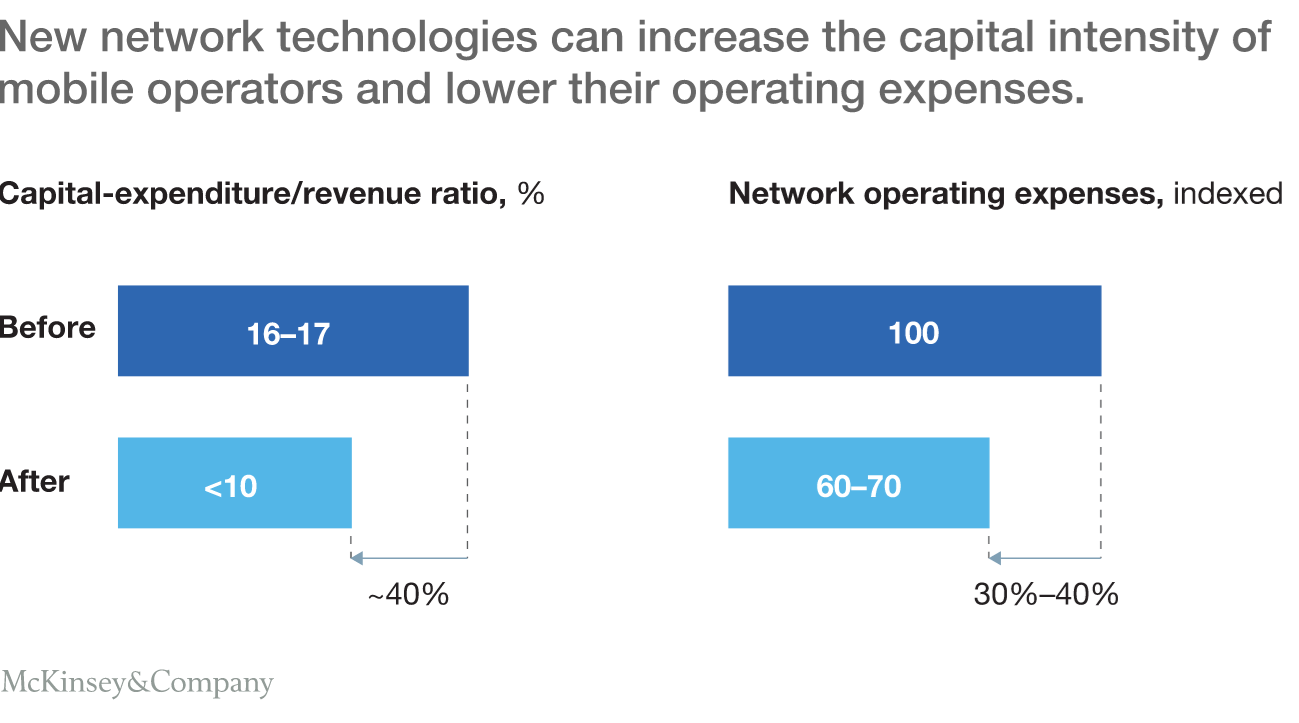

McKinsey analysts believe a range of new technologies, including artificial intelligence (augmented intelligence) can help service providers reduce capital investment up to 40 percent and network-related operating expenses by 30 percent to 40 percent.

“We estimate that just 20 to 30 processes generate 45 percent of the average operator’s operating costs. Using advanced technologies, such as machine learning, to simplify and digitize those processes can cut costs by as much as one-third,” McKinsey consultants estimate.

“Our analysis suggests that a cost reduction of 30 to 40 percent and increasing cash-flow margins from 25 to nearly 40 percent is possible,” they said.

“One company we know had 600 IT systems; another had 3,000 prepaid plans,” the consultants said. “Self help” systems also can help.

“A mobile operator we know reduced the number of support calls it fields by 90 percent after it set up sophisticated systems to track and anticipate the problems of its customers and to give them resources to solve those problems on their own,” McKinsey consultants say. “Providing self-service guides and automatic tips about possible problems can help customers solve 75 percent of the issues themselves. Customers can solve an additional 15 percent of problems by using advice from instant-messaging chats (with employees or artificial-intelligence agents) or from online discussion groups. This leaves just 10 percent of problems to be handled at the costliest level of support: a phone call with a customer-service agent.”

“With predictive models fed by customer information, mobile operators can develop cross-selling offers that appeal to individual customers and determine how best to reach them, down to the time of day,” McKinsey said. “This approach, we believe, can add as much as two percentage points to a wireless operator’s EBITDA margins.”

“One company increased its sales from cross-selling campaigns by 25 percent once it started using analytics to plan those efforts,” they add.

By running massive sets of customer data through machine-learning models, a service provider can identify people who appear likely to cancel their service. Then it can woo them with offers aimed at the causes of their dissatisfaction.

“Research by one mobile operator determined that two percent of its customers had a 48 percent likelihood of canceling their service in the next three months, a rate much higher than the five percent likelihood among its other customers, McKInsey found.

So the company divided the “likely churners” into segments based on the reasons they might cancel. Offers that sought to address churn drivers reduced cancellations by 15 percent, McKinsey found. Also, the mobile operator spent 40 percent less than it usually did to carry out such programs, the consultants said.