The biggest business problem telecom service providers face is use of the internet, and internet protocol, as the core of the network. The issue is not technology, but the business model. By separating use of the network from ownership of the network, telecom has lost the ability to “control” applications running on the network, fears voiced by many notwithstanding.

That loss of control means inability to generate revenue.

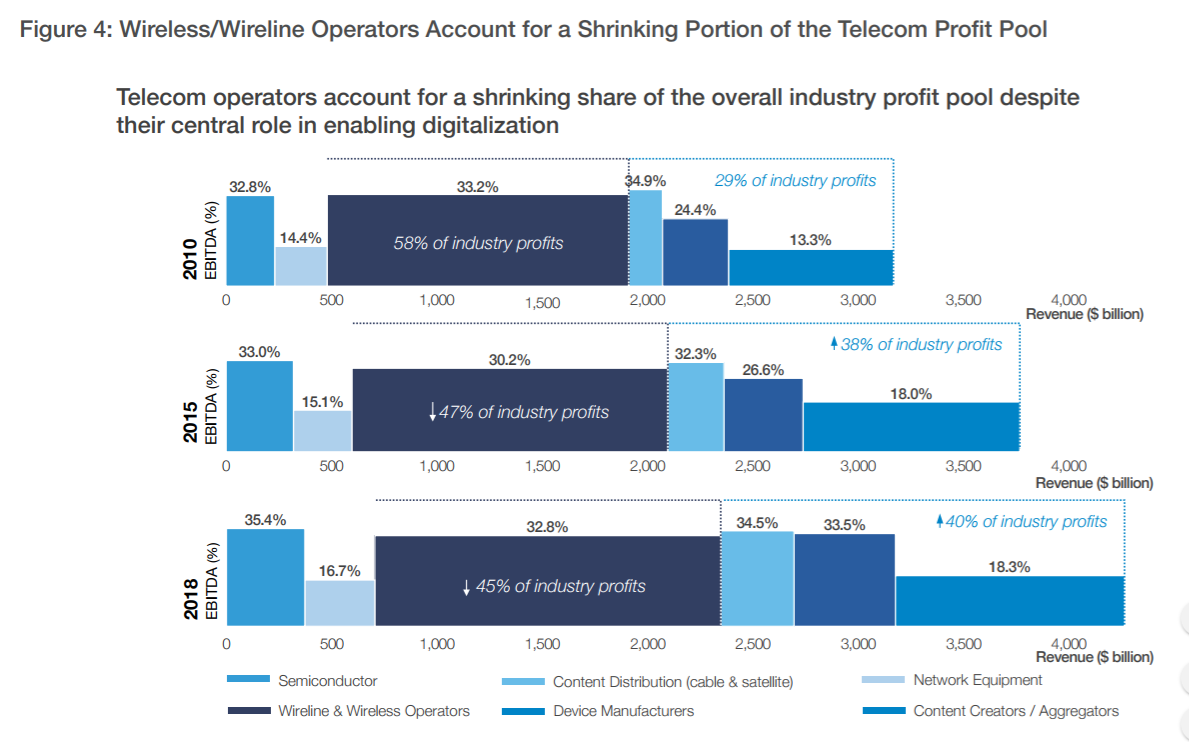

“The role that telecom operators have played in accelerating digital business and service models for external industries, as well as their own initiatives to refocus business models, have not translated into new value for the operators themselves,” says a report by the World Economic Forum. “They now account for a smaller portion of the overall industry profit pool than five years ago and this share is forecast to fall even further.”

Telecom service provider share of the broader internet profit pool (including all other segments of the ecosystem, such as devices, apps and over-the-top services) declined from 58 percent in 2010 to 47 percent in 2015, and is forecast to drop to 45 percent in 2018, says the World Economic Forum.

That is a change from historical reality, where the telecom service providers were the center of their own ecosystem. Today, internet access (and therefore a goodly portion of the former “telecom” industry) is a part of the internet ecosystem.

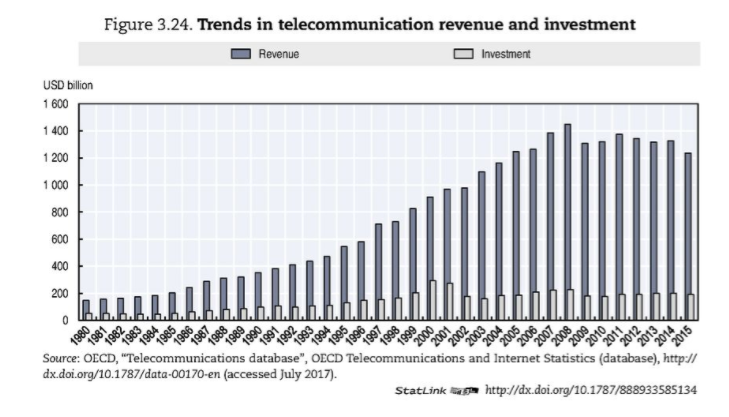

That is a historic change: legacy connectivity revenue is shrinking and therefore access providers are forced to look for big new revenue streams beyond connectivity.

The big problem. In a nutshell, is the positioning of the potential opportunities. As the WEF sees matters, the issue essentially is the ability to capture X percent of new digital revenues to be created across the ecosystem.

Though opportunities to move “up the stack” are not evenly distributed across all telecom segments and firms, big retail providers will have to do so.

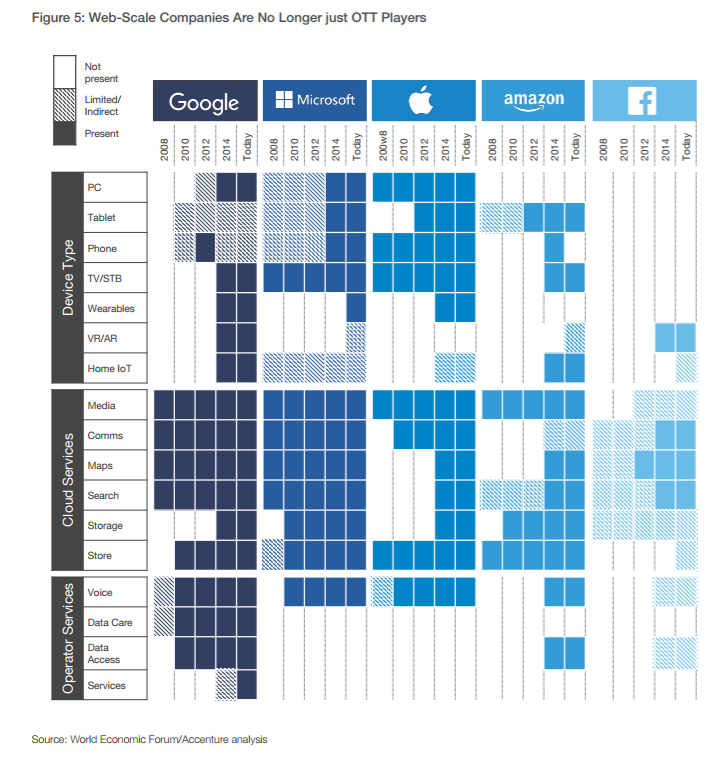

Keep in mind that app, software and device suppliers are themselves moving “down the stack” into parts of the ecosystem traditionally dominated by “access providers.”