Former Cisco CEO John Chambers has had a well-known theory about transitions: essentially, managing transitions underpins the business. “What Cisco has always done...is I focused on market transitions,” Chambers has said. “We moved from routing to switching...from switching to voice.”

We did the same thing with video, then we did the same thing in the data center,” he adds.

One might argue that firms such as AT&T are involved in precisely the same sort of management and strategic shift.

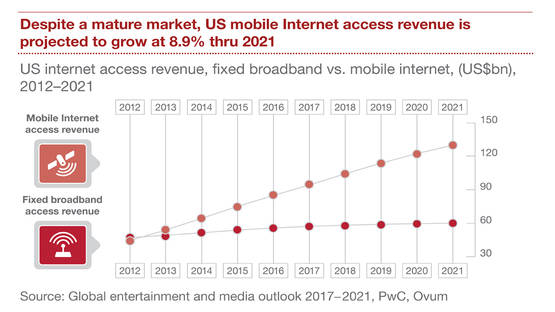

In developed markets, the key issue is what actors can do in the face of declining demand and revenue from all legacy services. Beyond efficiencies and acquisitions that increase scale, what fundamental strategy makes most sense.

And that is where opinions diverge. Analysts with a proper “near term” financial focus often urge firms such as AT&T to invest more in internet access capabilities, not content assets, the logic rationally being that if the foundation service of the future is internet access, a leading telco cannot afford to lost the market share battle to competitors.

Others might argue that the business itself is changing, that the key competitors really are app providers, not other access providers, and that the best transition model already has been pioneered by Comcast and firms such as Cisco.

In that scenario, the telecom industry is in a big transition from “access” revenues to “app” revenues (essentially a return to past practice, when nearly 100 percent of revenue was earned from apps such as voice).

So access providers have to diversify their revenue streams from “mostly access” to “access and apps and content.” And that change in industry dynamics is driven from outside, by the likes of Google and Facebook, not necessarily actions taken by access competitors, though that also is happening.

So it is that AT&T executives face questions about the wisdom of that firm’s content strategy. To be sure, AT&T also says it is moving fast towards gigabit network capability, so it is not neglecting investments in the access networks.

On the other hand, AT&T has taken criticism first for its DirecTV acquisition (on fears the linear business was shrinking) and now the Time Warner acquisition (more a move into content assets).

Proponents of the view that tier-one access providers must move up the stack and diversify their core revenues will simply note that revenue growth for most developed market tier-one service providers in recent years has come from video revenues.

“Since the day we bought DIRECTV, we assume that traditional linear video would be in a declining mode since kind of the nature of it, OTT and the ability to consume video on mobile devices, we believe would be the trend and the way where things went, we wanted to be in the leadership position,” said Randall Stephenson, AT&T CEO.

“We run these transitions all the time, right?” said Stephenson. “When you have technology transitions or business model transitions whether it's fixed phone service to mobile, whether it's a private line kind of service for business to VPN, whether it's -- you can kind of go down the list of whether it's feature phones to smartphones, we run these transitions and we think we're pretty good at it.”

Yes, there is a secular change from linear to on-demand consumption modes. But assets in linear are the building blocks for the move into on-demand subscription modes. Yes, there are gross revenue implications. But video entertainment represents the bulk of “new” consumer segment revenue sources larger developed market telcos have uncovered in recent years.

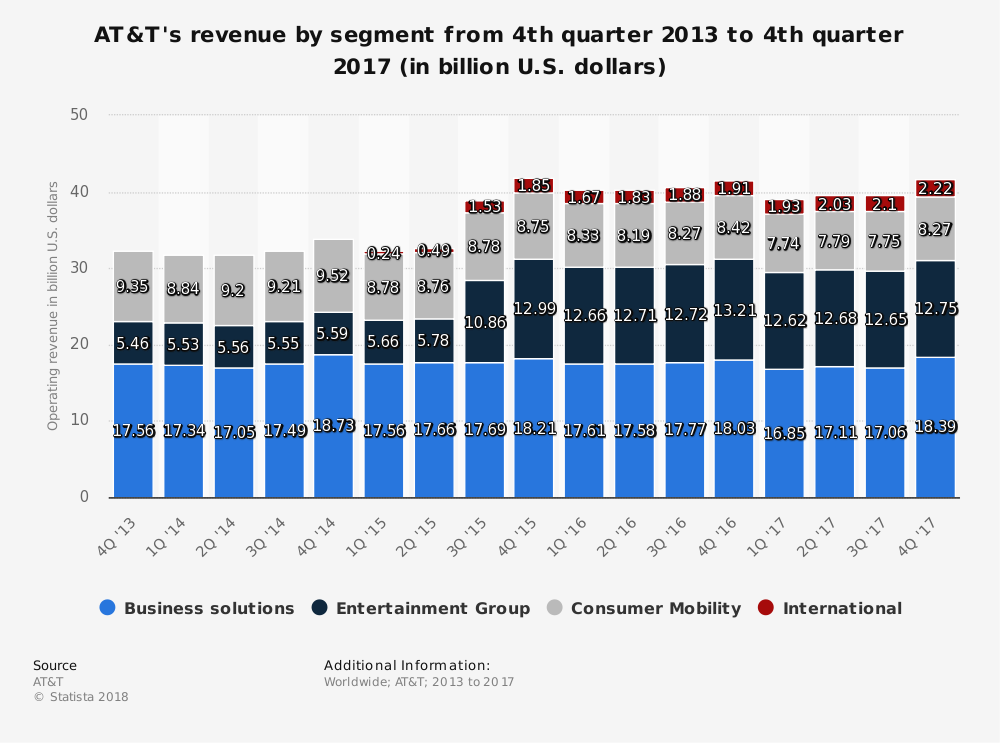

That can be seen in AT&T’s revenue contributors. Between 2013 and 2017, though business solutions and international revenues have grown fractionally, while consumer mobility declined, it was video (entertainment group) that showed clear growth of 134 percent.

That same sort of change will have to happen in the business revenues segment as well, in some ways related to internet of things. It is now all about handling the transitions, as Chambers always said.

{kind=link}