It might be apparent to all--from regulators to providers to infrastructure and applications providers--that global telecom business models are under duress. That is to say, any honest analysis would conclude that the core business revenue model is under extreme pressure.

So we should not be surprised to find that the telecom supplier base also is under duress. One only has to note the evisceration of the North American core infrastructure industry (Nortel bankrupt, Lucent acquired by Alcatel, acquired in turn by Nokia; the emergence of Huawei as the leading global supplier; financial struggles at Ericsson and Nokia as examples.

At the same time, open source solutions, white box and alternative platforms are emerging, in part because service providers know they must dramatically retool their cost structures, from platform to operations, even as they seek new sources of revenue and roles in the ecosystem.

So 5G “will not be a capex windfall for the vendors,” says Caroline Gabriel, Rethink Technology Research research director. “Operators will prioritize coexistence with 4G and architecture to prolong the life of existing investments.

“There will be heavier reliance on outsourcing and on open platforms to reduce cost and transfer cost further than ever from capex to opex,” Gabriel argues.

In fact, Gabriel believes mobile operators will try to spend as little as half the capex on 5G roll-out that they did on 4G.

That is one answer to the question some raise: whether mobile operators can even afford to build 5G networks.

And many of the network enhancements--virtualized RAN and hyper-densification and massive MIMO antenna arrays--also will be applied to 4G, extending the useful life of advanced 4G.

That might be important in allowing 5G to focus on support for new categories of use cases, apps and revenue models.

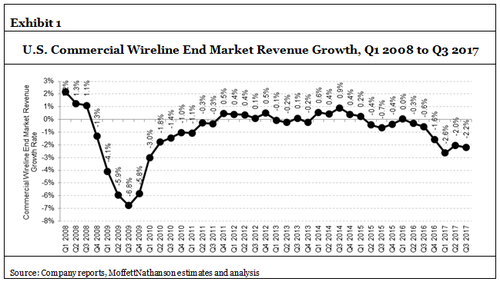

Matters are largely the same in the fixed network realm. As a whole, U.S. fixed line service providers have had a tough time generating any net revenue growth since 2008, according to MoffettNathanson figures.

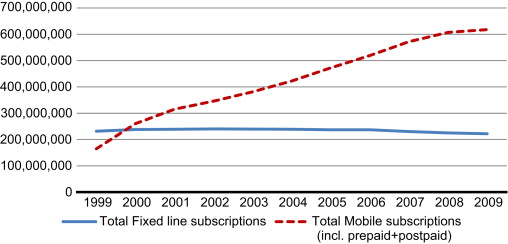

Much the same trend can be seen in Europe’s fixed network markets as well, as there has been zero to negative subscription growth since 1999. And the trend is happening even in the more-developed of South Asia countries, as fixed access declines (voice losses balanced by fixed internet access) and mobile grows.

That means, if anything, that cost pressures will be even heavier in the fixed network segment of the business, as any incremental capex or opex has to support an arguably-dwindling revenue potential.

{kind=link}

{kind=link}