If all you have is a hammer, every problem looks like a nail. So it is with a list of problems at Facebook, Google, Apple or Amazon that, it is said, only antitrust action to "break them up" can fix.

Privacy, algorithms, "tying a new service to an existing service" and promotion of a general climate of innovation are valid issues to debate and consider. But none of those issues is necessarily a problem that antitrust action can fix, sustainably.

If network effects exist (and everybody agrees they do exist), then bigness cannot be helped. Over time, firms that best supply consumer demand will get big, and become more profitable, than all other firms without requisite scale.

So here's the question: Can we repeal the “laws” of economics that suggest scale economics and network effects often matter for internet-based firms?

Privacy, algorithms, "tying a new service to an existing service" and promotion of a general climate of innovation are valid issues to debate and consider. But none of those issues is necessarily a problem that antitrust action can fix, sustainably.

If network effects exist (and everybody agrees they do exist), then bigness cannot be helped. Over time, firms that best supply consumer demand will get big, and become more profitable, than all other firms without requisite scale.

So here's the question: Can we repeal the “laws” of economics that suggest scale economics and network effects often matter for internet-based firms?

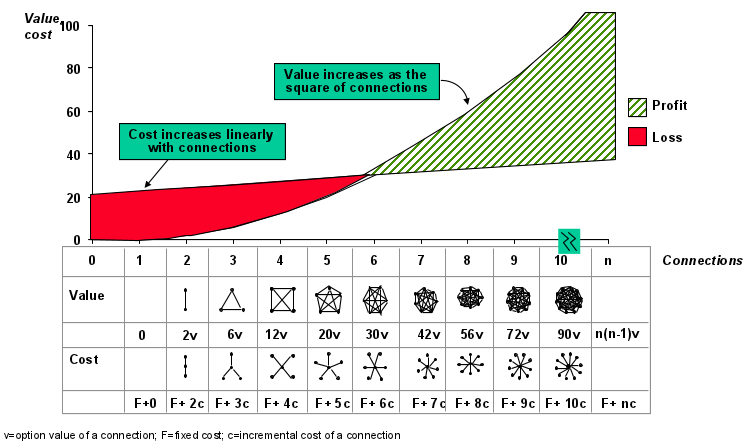

A network effect (also called network externality or demand-side economies of scale by economists) occurs when the value of any specific product or service grows with the number of people using it.

So here is the problem in a nutshell: an industry where network effects exist will always favor larger networks. Small networks simply will not have sustainable profit potential; large networks almost always will have large profit potential.

That is why many believe “platforms” are so important. Platforms are simply examples of nearly-ubiquitous scale. A market so competitive that no single provider has requisite will, over time, reform itself into one or two scale providers who are able to take advantage of the network effect.

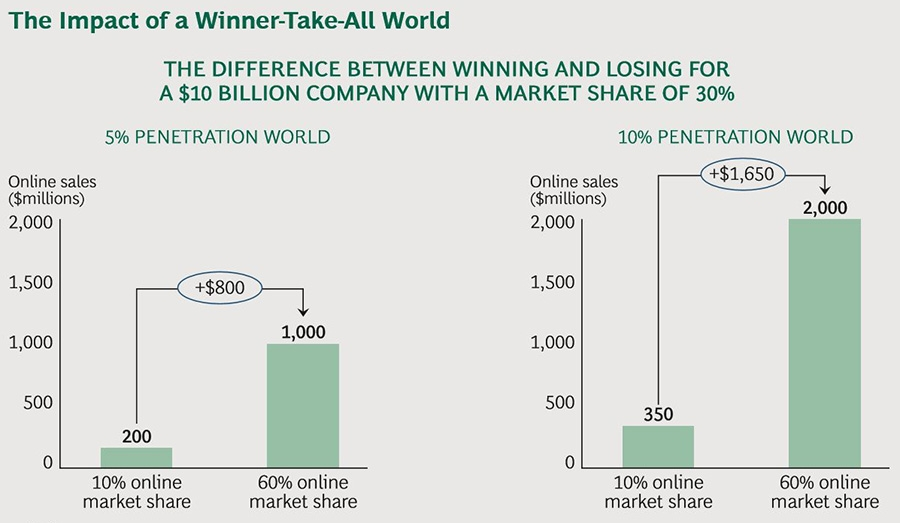

In a winner takes all market the best performers are able to capture a very large share of the rewards, and the remaining competitors are left with very little. That is an example of network effect.

Our “problem” is that the internet itself--and the competition it enables--seems to create such winners.

In fact, winner take all markets seem quite common across industries affected by the internet.

The percentage of total revenue at publicly-traded U.S. corporations earned by the top 100 firms was 53 percent in 1995, for example, growing to 84 percent over the next two decades.

In other words, scale seems to matter more than it used to, when price transparency, logistical systems and other barriers prevented more-robust competition.

Are there problems with Google or Facebook’s practices around privacy and algorithms? Yes. Can those problems be resolved without antitrust? Probably.

But as calls to break up Google, Facebook Apple and Amazon are growing more numerous, it is fair to consider a couple of contentious assertions, among them the notion that our traditional understanding of antitrust law is outmoded.

Specifically, even if “consumer protection” has been the rationale for past efforts to reign in monopoly, now “competitor protection” essentially is urged as the new standard.

To be clear, competitor success is the mechanism for consumer welfare benefits, so it is not crazy to say antitrust action is required to promote and protect consumer welfare.

But the proponents of new antitrust action (breaking up Google, Facebook, Apple and Amazon) focus on “social or political” impact of bigness rather than “economic impact” of bigness.

But some will argue that such social or political criteria are not the appropriate reasons to apply serious economic remedies.

But that has to be argument, after all, as even the new antitrust partisans admit “Google's dominance of the web-search market has no direct effect on consumer prices; we consumers get to use its service for free.”

So why take action? Not for such economic reasons. “The lack of competition in search means that Google has enormous power over what we see and access on the internet, and critics have charged repeatedly that it's used that power to favor its own services.”

So the new antitrust advocates are using the “media concentration” argument (“protect many voices”) argument for dismantling companies, not consumer harm.

That is important. It means the rationale for potential antitrust action is, in fact, not direct consumer harm but “competitor protection.”

Antitrust advocates admit that “Facebook's dominance of the social-networking market doesn't affect the price consumers pay; like Google, it offers its service for free.” So consumer harm cannot be demonstrated.

“But from the widespread dissemination of fake news to the leaking of profile data on likely more than a billion users, there are big problems related to Facebook's enormous size.”

Yes, there are issues--and important issues indeed--to be solved here. But antitrust does not solve them.

The “big is bad” proponents have to deal with scale economies, which is why bigness has happened across the application and internet ecosystem in the first place. Simply, in industry segments where value grows with the size of the network, bigness is an inevitable foundation for economic success.

If we “break up” the firms with scale, all the new contenders will simply continue competing until, again, some new provider with the requisite scale emerges. Scale means both lower costs, higher revenues and higher profits. That is just the way scale economics (network effects) work.

One can agree or disagree on what we are trying to accomplish with antitrust protections.

Some argue it is about “protecting smaller suppliers in the market,” “promoting innovation by breaking up big dominant firms,” or some other objective explicitly aiming to help new firms and small firms take market share from a few big firms.

Others will argue antitrust is about protecting consumer welfare first and foremost. Where consumer welfare is harmed, then antitrust remedies might make sense, and those remedies always involve limiting the dominance of leaders in any market.

But harm to consumer welfare remains the key test, and that is true even where network effects, scale economies and network externalities exist. And that harm still has to be demonstrated in tangible ways related to excess or “monopoly” profits (economic rent).

If we have issues with privacy or algorithms, those can, and should, be dealt with. But if economic harm, requiring antitrust action, cannot be demonstrated, that is the wrong solution to the wrong problem.