Clarity of thinking about “all things digital” remains rampant in the telecommunications business, for good reasons. There seems no universal agreement about what “becoming digital” means, and whether that applies mostly to internal processes or products sold to customers, or both, in what proportion.

That is why there is perhaps no more-controversial idea than telecom service provider strategy options over the next couple of decades.

Fundamentally, “strategy” is controversial because it is likely most service providers have few opportunities to move beyond the connectivity services they presently offer, and become “platforms” or providers of services beyond connectivity.

The reason is simply that becoming “platforms” and creating the foundation for partnerships requires scale, and most firms will never have the requisite scale (coverage, customer base, capital, skills).

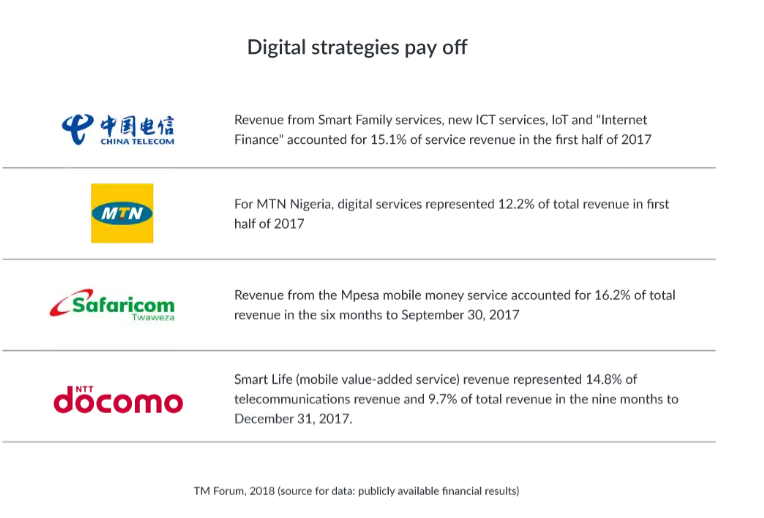

Still, a handful of service providers now earn 10 percent to 15 percent of total revenue from “non-core” sources, and are making headway towards developing revenue sources beyond connectivity.

Others are building potential platforms around advertising (SingTel, AT&T, Verizon); enterprise or small/medium business cloud services (BT, China Mobile); payments (China Telecom, Vodafone; internet of things (DT, SK Telecom, Swisscom, Telefonica, Verizon).

But those are initiatives requiring some amount of scale, and most service providers globally simply will never reach that scale. So, fundamentally, the choice is simply to become a lower-cost supplier of connectivity services.

On the other hand, there are many potential new competitors for connectivity services within most countries. And that is among the key risks. To be sure, connectivity must be provided. But it is something of an open question “who” will be providing such services in two decades.

“The idea that the telecom business will die is preposterous, although it is possible that CSPs could lose control of parts of the retail market,” the The TM Forum report says. In a functional sense, that is true.

But we already have many examples of features and functions that remain vital, even if the business model supporting such operations changes drastically. The reason global voice and messaging revenues are becoming less important revenue drivers for service providers is that those apps are becoming features offered by many suppliers, and are not “for fee” services.

“It is also possible that the telecom industry will experience an inexorable stagnation of revenue and industry consolidation, but this does not necessarily mean that the industry will become less profitable,” since “greater automation could mean that cost-cutting outpaces revenue decline.”

That might be true, but only if the amount of direct competition does not increase, and also if outside firms do not become major suppliers of connectivity functions, almost certainly with business model drivers to make those functions available without charge, or at very low cost.

Broadly, the strategy options are said to include focusing on connectivity almost exclusively; becoming a digital platform or a digital partner. But few service providers will have the scale to attempt the platform or partner strategy. Cloud computing, payments, advertising and IoT are, or will be, scale businesses.

One issue is that “the term platform is used loosely,” TM Forum says. “In many cases CSPs describe a service as a platform business if they have more than 100 partners but it’s not clear that they have built partner ecosystems.”

The “digital partner” strategy always is equally tough to characterize, as it involves the access provider becoming an enabling platform for services delivered to end users. In the internet era, that generally is tough, as use of internet protocol means any lawful app or service entity can market directly to potential customers.

Also challenging is the tasks of converting internal support processes into actual services that can be sold to third parties, as Amazon Web Services converted an internal function (cloud-based services) into a retail offering for third parties.

Twilio, which provides application programming interfaces for communication features, is cited as a prime example. Basically, Twilio allows developers to add communication features to any app or service.

But this approach is problematic, the report authors suggest. This approach requires “exposing core retail services” to firms such as Amazon, Facebook or Google.

That could allow such firms to become competitors in the connectivity business, as Google’s Project Fi already has done.

Even the GSMA eSIM standard reduces the power of mobile operators, by allowing end users to toggle between service providers on demand.

“The GSMA’s eSIM specification enables remote SIM provisioning of any mobile device, allowing consumers to store multiple operator profiles on a device simultaneously, and switch between them remotely,” the report notes.

Network slicing might become a means of creating partnership models in a new way, however, the report suggests. Network slicing creates virtual private networks that might offer service differentiated by coverage, capacity, latency, throughput, security or time of day access, for example.

The report suggests one key problem: most service providers not be able to move up the stack.

“The connectivity services delivered by CSPs (communication service providers) have remained largely unchanged for the last 10 to 15 years, except for the type of traffic carried across networks,” say the authors a new report issued by the TM Forum.

Though the report is largely sanguine about prospects, the challenges and threats seem very real.

{kind=link}