Can a “mobile-only” business strategy succeed when markets reach saturation? In other words, once every potential customer already buys the service, can some combination of higher usage, new products or vertical integration offset pricing and profit pressures in zero-sum markets where market share gains can only come at the expense of other mobile operators?

It is, at present, an open question. Optimists argue that mobile operators will grow revenue from new customers, new applications, new roles in the ecosystem and even cannibalization of fixed network market share.

Pessimists likely will argue that while this is a possibility for the best-capitalized and largest providers in some markets, in most markets opportunities to grow roles, value, revenues and revenue sources are quite limited.

Still, there are some examples of mobile-only financial performance beating the financial performance of converged suppliers who own both mobile and fixed assets. In the quite-mature European markets, for example, Rewheel analysts say mobile-only providers have outperformed converged suppliers.

Some caveats are in order. Generally speaking, mobile-only attackers have no legacy to protect, and the converged operators include both the former incumbent fixed operators and some attackers who have chosen to be in both mobile and fixed markets. The point is that attackers have more choices.

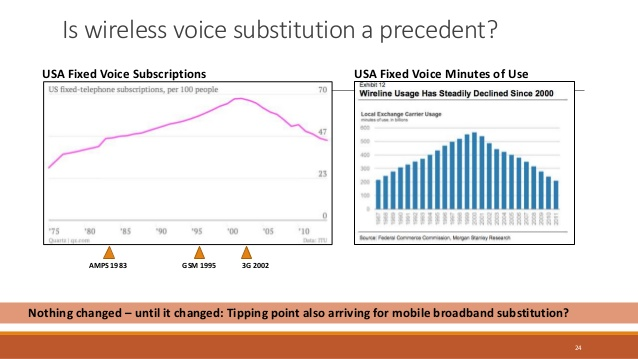

Also, there are structural issues. Fixed network suppliers have lost share in voice, while mobile operators have gained share. Mobile operators have been the exclusive providers of messaging. Now something similar is happening in the internet access market, as mobile alternatives are starting to compete with fixed networks.

When utilization of any network drops--when there are fewer paying customers--per-customer costs obviously grow. Conversely, on any network with higher utilization--more paying customers--such costs drop.

In other words, all other things being equal (they are not equal), any network that gets revenue from only a half of locations the network passes (for example), will have per-customer costs that are literally double the per-passing figures.

Selling more products to a smaller number of customers helps. That is why triple play bundles are so popular. Selling more products means revenue is higher, per account.

The point is that we need to be careful when analyzing strategies. There are multiple reasons why particular suppliers, in particular markets, might achieve higher or lower revenue, revenue growth, profitability and cost-per-customer metrics.

Lower-cost platforms, as a rule, will help, and mobile networks are lower cost than fixed networks. Fixed networks, on the other hand, have had strategic advantages where it comes to the types of products that can be sold. Video entertainment is bandwidth-intensive, so in markets where linear or on-demand video is popular, fixed networks have had a price advantage.

That also has been true for internet access charges. Where demand is heavy, fixed networks have a cost of supply advantage. Generally speaking, older mobile networks have featured costs per gigabyte as much as an order of magnitude higher than fixed networks. That explains the widespread use of offload to Wi-Fi.

For most fixed networks, the key problem is product substitution. In the past, voice revenues have driven financial results, and customers have fled for mobile alternatives. Fixed internet access and video services have helped compensate for voice losses.

The problem is that growth is tough when network utilization grows increasingly negative. That is why some have called the fixed networks business a matter of terminal decline.

At the same time, fixed network suppliers face not only mobile substitution, but also facilities-based new fixed network competitors in some markets. So revenue growth and profit now are bigger issues in some markets.

In other words, fixed networks now are in the midst of a key business model change, where customers, products and roles are evolving. It is conceivable that capex and opex profiles have to adjust to lower potential revenues, no matter how customer sets and perceived value changes. Some argue that fixed network backhaul will drive more value in the 5G era.

It might be tempting to argue that mobile-only business models still make more sense than integrated models combining ownership of both fixed and mobile assets. But many argue that converged business models actually have performed better, financially, than mobile-only operations, across much of Asia, for example.

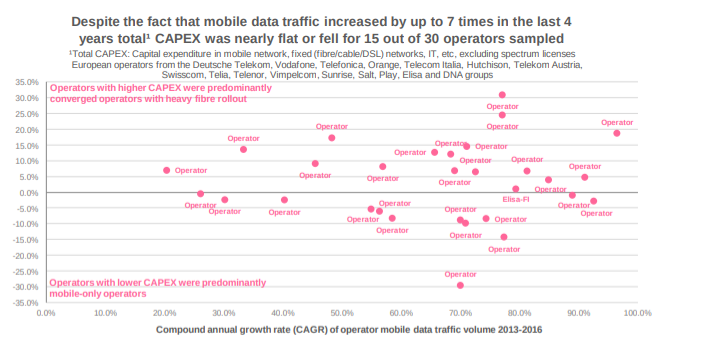

The issue is the growing cost of supplying incremental bandwidth. To be sure, there are three basic positions on this matter. Some believe costs will grow unmanageably. Others believe costs can be managed to match demand. Yet others believe costs will drop.

The outcome likely will be different in various markets, and by firms within those markets. Low-cost or lower-cost providers will generally win, all other things being equal. Of course, all things rarely are truly equal.