Is the video subscription business shrinking? The answer depends on which part of the business one is looking at.

As linear video subscription prices rise, take rates drop. Cheaper streaming alternatives, meanwhile, keep growing, both in terms of revenue and subscribers. So you might think the market is shrinking, in terms of revenue. Maybe not.

Higher prices for linear subscriptions will drive even more consumers towards alternatives, and that will eventually reduce average prices for any single service. What remains to be seen is whether total spending actually will shrink much. As some of you already have discovered, lower prices for linear is balanced by more spending on streaming services.

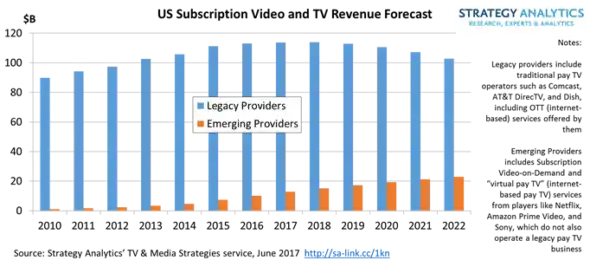

The point is that aggregate video entertainment spending might not actually drop. In fact, there already is evidence that total video scription spending is growing, looking at both linear and streaming formats.

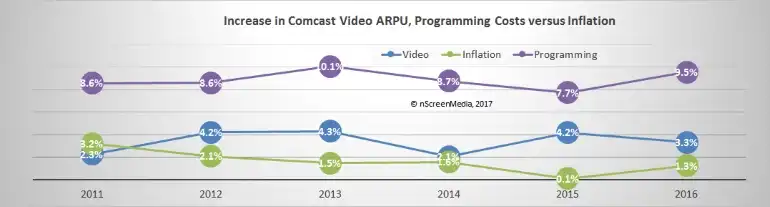

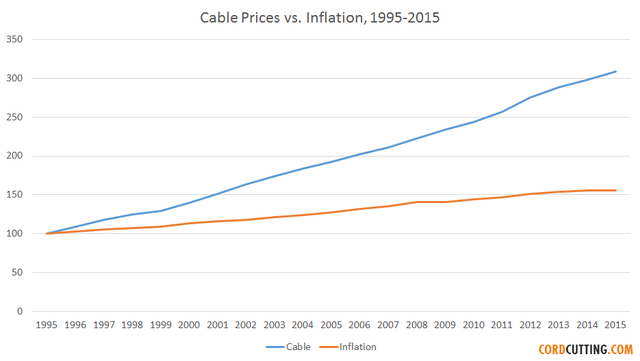

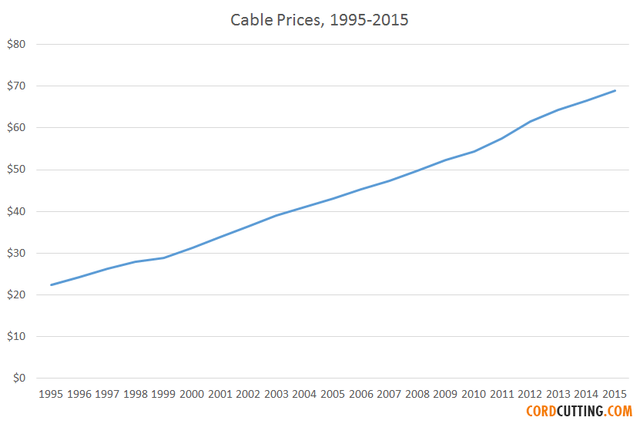

According to Federal Communications Commission reports, U.S. cable TV prices climb every year, though arguably not so much higher than the background rate of inflation. Since the cost of goods (programming) is rising much faster than the rate of cable TV increases, service providers are finding operating cost economies elsewhere in the business.

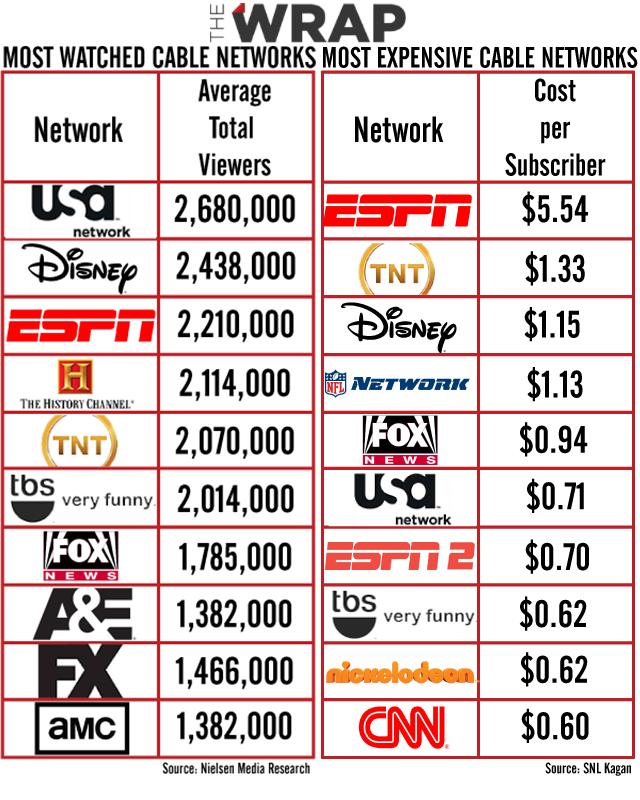

Sports programming costs are one culprit. At around seven percent annual increases, prices double in a decade, so you can see where this is going.

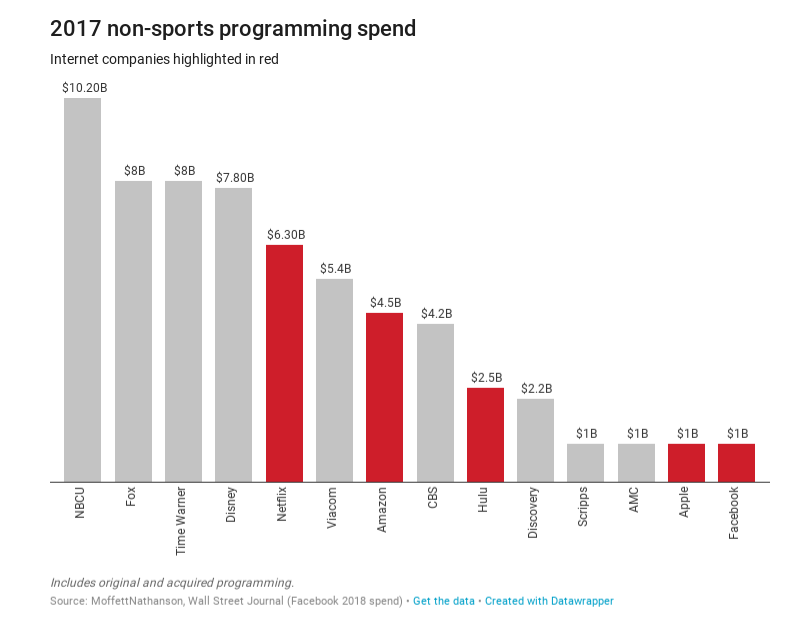

Then there is the Netflix effect, where high spending on original content by internet app firms is forcing all the other competitors to ratchet up their spending as well. In fact, Netflix now spends as much as does Disney, Fox and Warner Media on content, every year.

{kind=link}