Major U.S. “cable TV and telephone” service providers (fixed network suppliers) can be divided into two groups: firms that might realistically consider expanding their service territories, and those that likely would not, or cannot, consider it.

For regulatory reasons, AT&T, Charter and Comcast likely would face antitrust opposition if they wanted to expand their fixed network footprints. CenturyLink likely does not wish to do so, and Frontier cannot afford to do so.

Only Verizon has a glaring need to “catch up” with its major competitors, in terms of fixed network coverage, and likely would not face antitrust scrutiny. That explains the out of market expansion Verizon now plans, using fixed wireless as the access platform.

Comcast could in 2016 reach 110 million U.S. homes. Charter could reach 101 million homes. AT&T reached 122.5 million U.S. homes. Verizon could reach just 55.2 million homes. CenturyLink reached just 49.2 million homes; Frontier Communications only 32.6 million.

The big immediate wild card is 5G, which should, over the next several years, expand the number of providers able to supply 25 Mbps or faster service, for most of the U.S. population, using some form of 5G platform. In early 2018, 20 percent of U.S. homes are mobile-only for internet access.

The point is that, over the next several years, access competition is going to change dramatically, with the number of suppliers selling 25 Mbps or faster internet access service growing by perhaps two to three in most markets (Sprint, T-Mobile or a combined company; plus either AT&T or Verizon in most areas as “new” suppliers).

That assumption is based on attacks by Sprint, T-Mobile US and Verizon in AT&T legacy markets; Sprint, T-Mobile US and AT&T in Verizon areas, and all of the above in CenturyLink and Frontier markets.

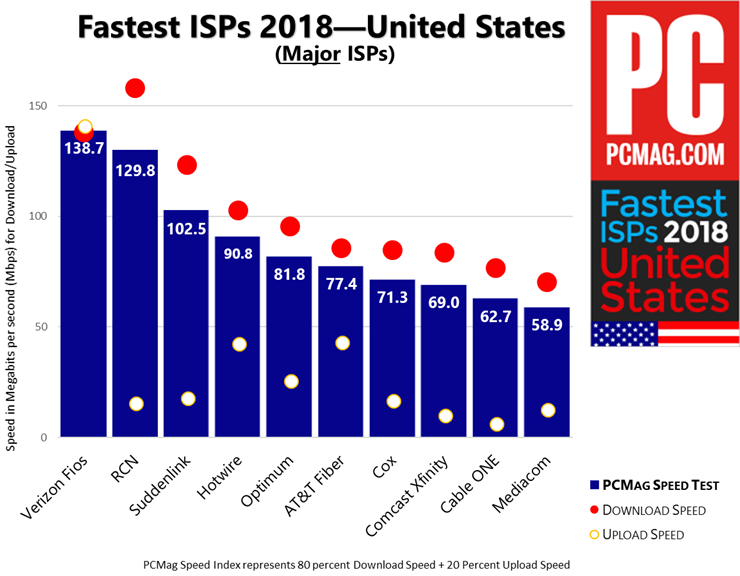

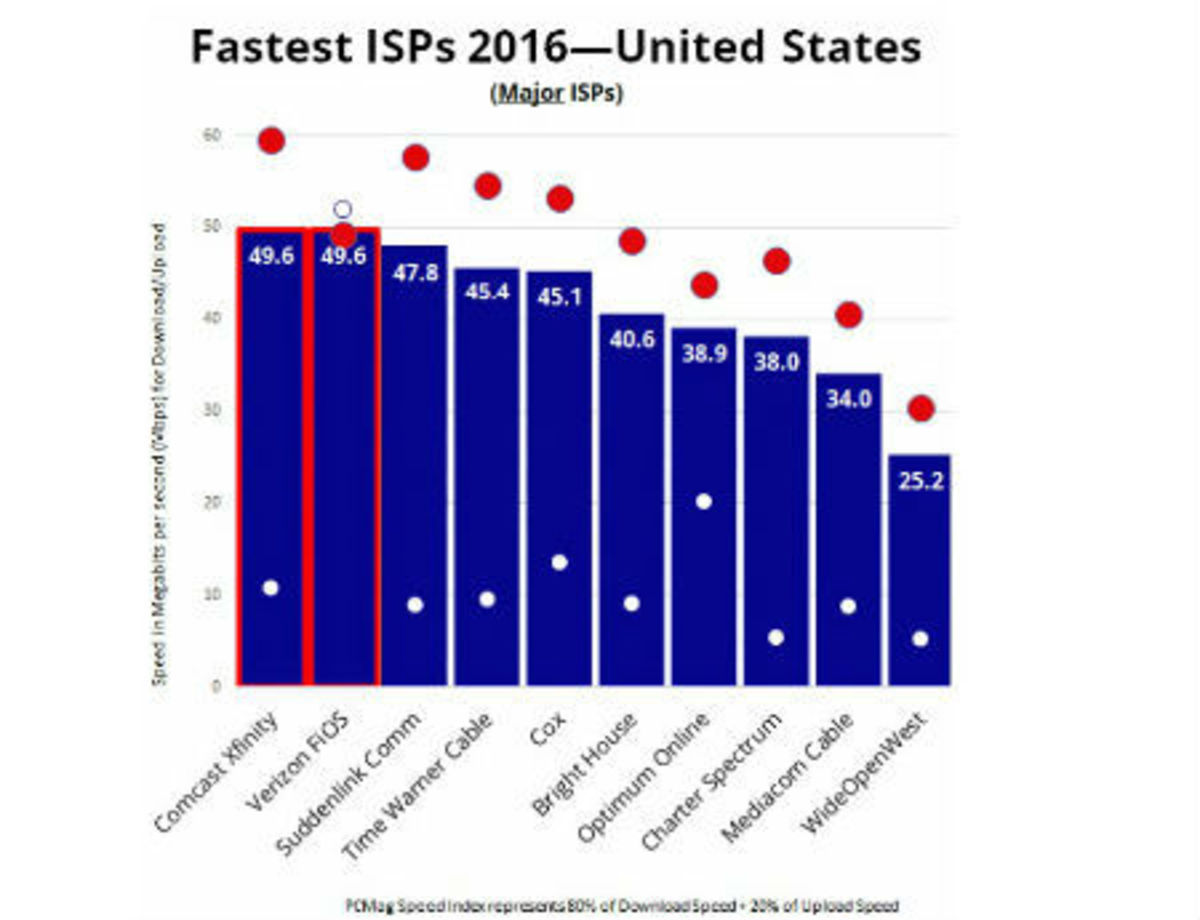

Also, both Viasat and HughesNet sell satellite-based internet access at minimum speeds of 25 Mbps nationwide, as well. And by 2018, speeds had climbed well above 2016 levels, for many of the largest U.S. ISPs, more than doubling over two years.

Competition, service quality and price are rarely what all observers would prefer, but competition and service quality (and possibly price) are going to change radically in the 5G era, when widespread mobile substitution for fixed internet services will be a realistic alternative for the first time.

No, service is rarely as fast, as cheap, and competitive, as some would prefer. But the history of internet access in the U.S. and most other markets is rapidly-falling costs (or cost per bit, if you prefer), faster speeds and more-capable competitors.