Though it is counter-intuitive, “monopoly” internet access service (a single fixed network supplier) might be the best we can hope for, in many U.S. rural areas, and might not, in fact, provide consumer benefit that is worse than a two-provider market would supply.

And internet access prices and speeds, while perhaps not always ideal, are often the same in “monopoly” areas served by just a single provider, as prices are in areas with at least two providers.

Also, wireless providers already offer 25 Mbps service across virtually the entire U.S. market, and 5G will offer even more options.

That is not to say more investment, or more competition in the cabled networks infrastructure is not a good thing for consumers, where it is feasible to support it.

But single-supplier markets, especially in rural areas, often are the result of local market conditions that have a rational basis, and where multiple fixed network competitors might not be feasible.

In many rural areas, service is provided by a cooperative, which tells you quite a lot about how lightly-settled many rural areas are, and how difficult the business case can be.

internet access prices and speeds in single-provider markets are “the same” as prices in markets with two or more competitors, Federal Communications Commission’s Form 477 data from 2015 and 2016 suggests. That, at least, is the conclusion reached by a new study by Phoenix Center Chief Economist Dr. George S. Ford.

Most areas with less competition are rural areas, for obvious reasons: the business case for fixed network or mobile communications is toughest where density is lowest. There are some 11 million census blocks in the United States with populations of less than 30 persons, on average. That is a difficult degree of density to support with any advanced cabled network, no matter what the physical media.

Since communications services in the U.S. market are provided almost exclusively by for-profit firms, return on investment does matter, and rural areas are where it is hardest to make the case for investment at all. That is why we subsidize rural communications: in the absence of subsidies, it is unclear whether any private actor would make the investment.

FCC data from 2014 showed that 38 percent of U.S. residents had access to more than one provider of broadband (using the definition of 25 Mbps downstream as a minimum) service, 51 percent had access to one provider, and 10 percent had no access to broadband service by a fixed network.

That definition excludes any internet access service below 25 Mbps. At year-end 2016, 92.3 percent of all Americans have access to fixed terrestrial broadband at speeds of 25 Mbps/3 Mbps, up from 89.4 percent in 2014 and 81.2 percent in 2012, according to the FCC.

That statistic ignores satellite access, which does offer 25 Mbps or faster speeds over virtually the entire United States, supplied by two providers. Using the 10 Mbps standard, fixed terrestrial service of 10 Mbps/1 Mbps is available to 96 percent of the population, according to the FCC.

Still, over 24 million residents (not households) still lack fixed terrestrial broadband at speeds of 25 Mbps/3 Mbps, Ford notes.

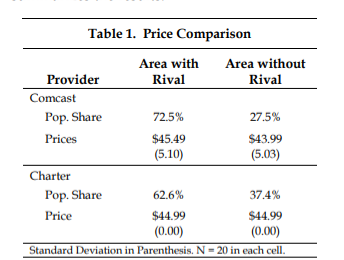

Still, looking only at Comcast and Charter Communications retail pricing for internet access, the prices are comparable whether those firms have competitors or not, Ford notes.

Also, in many of the nation’s rural areas, cooperatives offer broadband service, and in those areas there arguably is no business model for a second fixed network provider.

Nearly 57 percent of cooperative service territories (by population) are served only by the cooperative. Also, only 55 percent of the cooperatives customers have access to 25/3 Mbps broadband, Ford notes.

The point is that the business model--especially in rural areas where cooperatives are the norm--might not support competitive supply.