In the streaming era, ability to offer unique content, and lots of new content, has emerged as a strategic advantage. And that has lead to a new emphasis on production of new and unique content.

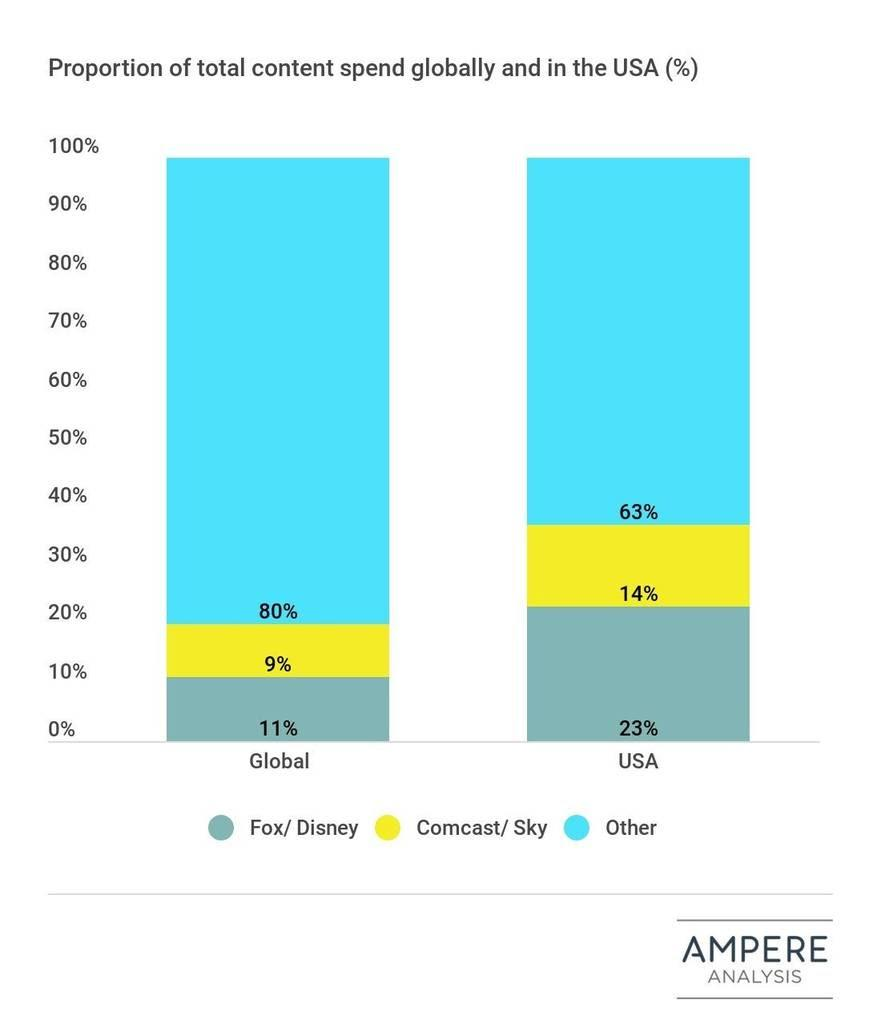

About $43 billion is spent every year by Disney and Comcast to create new content. Altogether, some $116 billion is spent to produce new video content in the United States each year, according to Ampere Analysis.

Such spending on unique content matters now that Netflix has dramatically changed the economics of the content business.

For decades, virtually all suppliers of linear subscription video services offered the same fare: a big bundle of channels. Differences were at the margins, namely the specific mix of channels offered to customers on each tier of service.

In the video streaming business, content exclusivity is the norm. And that emphasis on unique content is going to increase in the future.

The same pattern holds for TV series content. There is some overlap of programs, but most of the video is unique to Netflix, Amazon Prime or Hulu, for example.

Netflix spent about $13 billion in 2018, about 85 percent devoted to creation of new series and original content. By way of comparison, all “Hollywood” investment in new movies might be about $10 billion in 2018.

Eventually, consumers faced with a huge palette of streaming services with mostly-unique content are going to be buying multiple subscriptions to assemble the mix of content they prefer. So aggregation services are sure to arise. Ironically, increasing fragmentation is also likely to increase the perceived value of traditional big bundles, if providers of those services can win rights to offer much of their content in both linear and on-demand fashion.