Even when connectivity providers agree that development of new revenue sources beyond connectivity is essential, much disagreement remains about precisely how to develop those opportunities.

In large part, the differences of opinion arise from scale requirements. Simply put, many new opportunities require scale that most service providers do not have, and cannot get. Consider the matter of ownership of video content, or acting as a distributor of video content.

Telefonica, for example, has been a big believer in the value of revenue sources beyond connectivity, and in recent years has boosted its video subscription revenue to about seven percent of total revenues.

And video revenues also have emerged as a huge driver of “digital” revenues. Video subscription revenue now accounts for more than half of total “digital revenues,” for example.

Digital revenues account for nearly 14 percent of total revenues, and are among the fastest-growing revenue sources available to Telefonica. Digital revenues grew more than 25 percent in the third quarter of 2018.

In part, Telefonica’s optimism about video distribution and content ownership flows from its strategic footprint in Spanish-speaking countries, which create a large market for video assets. Such footprints are hard to assemble.

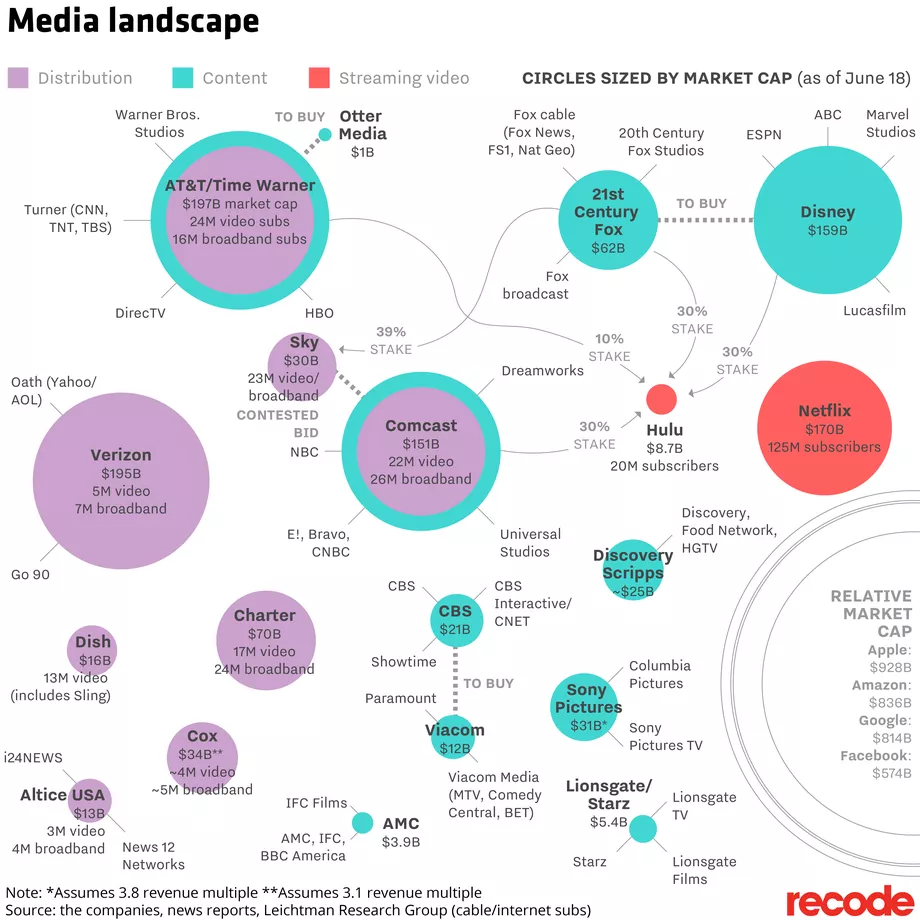

Even if they wanted to become major owners of content assets, as Comcast and AT&T have become, even firms as large as Charter Communications and Verizon cannot afford to do so.

AT&T has joined Comcast as a major owner of video content, movie studios and related assets. But AT&T also has taken on huge amounts of debt to do so.

Verizon, at $126 billion annual revenue, and Charter Communications at about $40 billion annual revenue, do not have subscriber bases, free cash flow and other attributes of scale to acquire major media assets, for example, with CBS, Viacom, Discovery Scripps, AMC and Lionsgate possible acquisition targets, eventually.

Some might argue Netflix remains an acquisition target, but only for a very-well-heeled buyer, and likely far beyond the realm of possibility for a telco or cable company.

Both Comcast and AT&T are big video distribution outlets as well. In fact, AT&T is the largest provider of linear video subscriptions; Comcast the number two provider.

Of course, there also is the example of Netflix, which has become a major owner and producer of original video content, without acquiring major content production assets. Amazon Prime arguably has been less successful than Netflix, to date, but is on the same path.

One might well argue that there are few firms left with the strategic rationale and cash to consolidate the few remaining content assets of any scale in the U.S. market (Disney, CBS). And one might also argue that the logical path forward, for firms with strategic intent, is to follow the Netflix and Amazon Prime approach of directly funding and owning unique content assets.

With the development of the over-the-top streaming, firms such as Netflix and Amazon Prime have found they do not need to build, own or lease network assets to act as video distributors. Importantly, perhaps, the firms already in content include giant technology firms with lots of cash to make acquisitions and investments.

Alphabet, with $59.6 billion in media revenue (advertising revenue or content sales revenue), dwarfs Comcast, with $19.7 billion in media revenue, plus some portion of the 21st Century Fox revenues of $18.67 billion. Facebook already has about $11.49 billion in “media” revenues.

The simple conclusion is that a few connectivity providers have scale to make content ownership a viable strategy. Others will not be able to attempt that strategy, but can make a business out of content distribution. For some, not even distribution will make sense.

For many such firms, horizontal mergers, including out-of-market expansion, might be the only realistic opportunities.