In most parts of the world, ubiquitous competition in the fixed network business is not considered viable. In a smaller number of cases, a duopoly exists, but some observers believe telcos cannot long compete successfully against cable operators.

The reasons for that belief are several. Cable hybrid fiber coax networks cost less than fiber-to-home networks to upgrade and build. That especially is true when stranded assets are considered. Stranded assets are facilities that generate no revenue. And that is a major business model issue in a competitive market.

Assuming two equally-skilled competitors, competition roughly doubles the cost-per-customer of the network. Under conditions where demand is high (95 percent) and one contestant has 65 percent market share, all remaining competitors must fight for perhaps 33 percent of remaining locations. For a new FTTH network, that means customers might be found on only about one home out of every three passed.

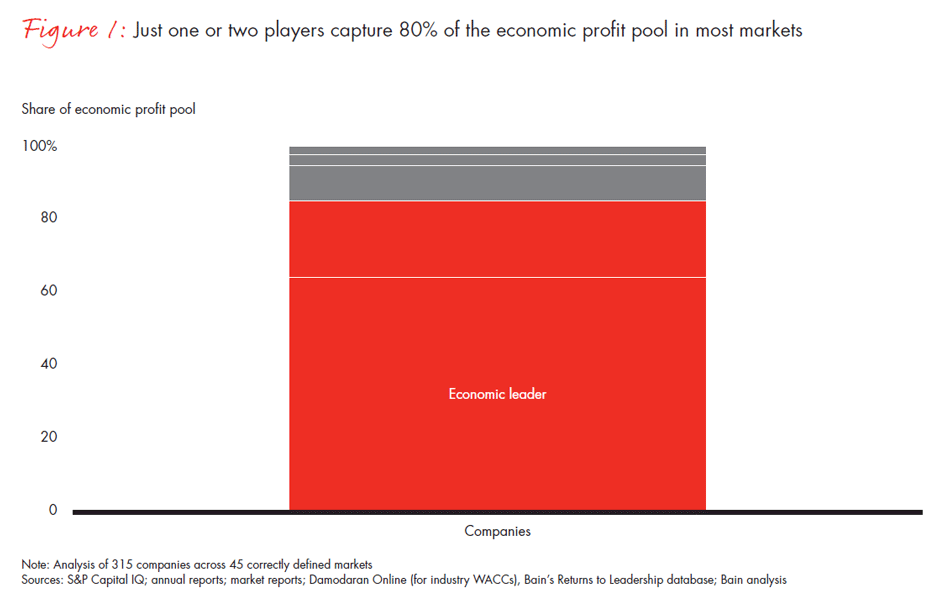

Keep in mind that, in most markets, 80 percent of profit is earned by two firms.

Keep in mind that, in most markets, 80 percent of profit is earned by two firms.

That poses daunting financial return issues. So, sure, many fixed network telcos are reluctant to invest robustly in FTTH networks. But there are huge barriers to doing so, not the least of which is the paucity of revenue that could be gleaned.

Some do not believe that argument, and instead think telcos could earn a return if they invested more heavily. And some analysis of potential upside is therefore required. The numbers are daunting. Challengers often attack niches--parts of metro markets or smaller and rural markets where it is easier to grab market share.

Incumbents have other problems, as they most often are required to serve all parts of a city, and cannot simply choose not to serve some parts of the city. Beyond that, revenue from legacy revenues is challenged, and the revenue upside from consumer fiber to the home is mostly internet access.

The business case for full-city overbuilds can be made. But it probably cannot be made universally.