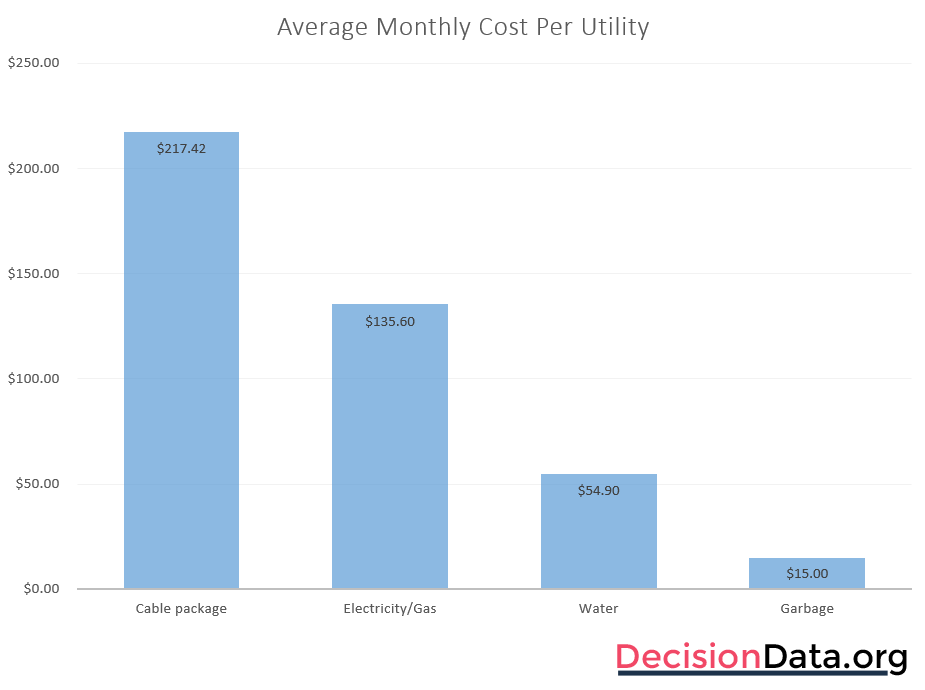

A recent report states that the “average household cable package is now $217.42 per month.” Some will interpret that finding as a case that video subscription prices are too high, or that a “cable package” is too high, compared to other “utilities” consumers purchase. That is a case of facts and truth not aligning.

The key phrase there is “package.” Perhaps 50 percent to 60 percent of buyers of “cable services” buy some form of bundle.

So while it might be factual that the “average household spends $205.50 per month on all major utilities combined (electricity, gas, water, sewage, garbage),” this is not an apples-to-apples (a comparison of services on a like basis) comparison.

A cable “package” can include two to four different services: internet access, linear video subscription, voice service, mobile service. So one might argue that, truthfully, the cost of three or four cable-delivered services are about the same as three of four other “utility” services, and not much more than that.

Also, “average” might mean half of customers pay more, while half pay less, for any of the products (median) or that, considering all bills, the blended costs are as stated. It is not clear which definition is used, in this case. The big point remains that the “package” represents two to four services.

Crudely assuming that half of the cable packages include three services suggests a single component cost of about $71 each. But that is an attributed cost. One derives different numbers assuming just two services per bundle or four services per bundle.

A more plausible estimate is to value internet access at $40 to $50 per month; video at $80 to $100 per unit; voice at about $35 to $40 a month and mobile service at $40 to $50 a month. That would explain the $217 cable bundle “average.”

The analysis of cable bundle prices is plausible and factual. It is not, strictly speaking, “truthful.”