It is a no-brainer that 5G economic impact will be somewhat substantial over the next decade, if only because communications is a significant portion of global economic activity all the time. In 2018, for example, mobility by itself represented nearly five percent of global gross domestic product, by some estimates.

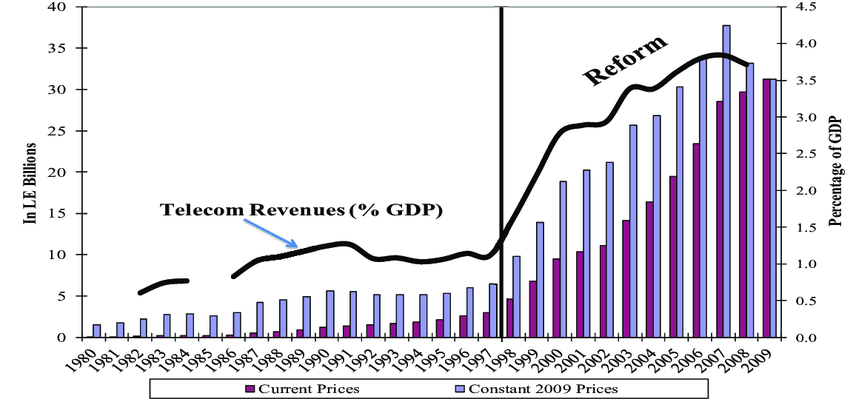

Other estimates often peg all communications spending at about three percent of GDP to 3.5 percent of GDP.

Most economic assessments attempt to include the related economic benefits, in addition to the direct benefits. The multiplier might be in the range of $5 in benefit from every $1 in telecom spending.

Still, direct impact is substantial. If global GDP is $142 trillion, then 3.5 percent in direct telecom spending is $5 trillion. Mobility is not all of telecom spending, but likely represents 65 percent or so. In that case, 5G might be included in the $3.25 trillion, mobility generates. But, of course, not all spending is on 5G. So reduce 5G share to perhaps half and 5G might represent $1.6 trillion in revenue.

It is nothing to dismiss, but is a far cry from the $7.5 trillion some estimate.