Are “happy” customers “more loyal?” It might be hard to say. Satisfied customers--it often is believed--lead to loyal customers, which in turn leads to profits.

Customer satisfaction typically is thought of as a predictor of customer buying intentions and loyalty, propensity to desert one provider in favor of another, account longevity, revenue per relationship and financial performance. That is perhaps one reason so many executives take stock in the net promoter score, a measure of customer satisfaction, in telecom and other industries.

“Customer satisfaction is a leading indicator of company financial performance,” says the American Customer Satisfaction Index. “Stocks of companies with high ACSI scores tend to do better than those of companies with low scores.”

But the relationships are not always so clear.

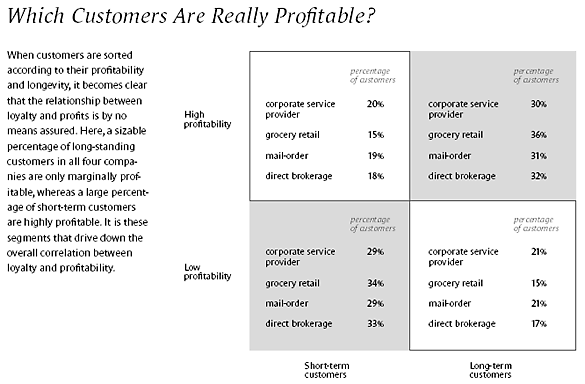

“What we’ve found is that the relationship between loyalty and profitability is much weaker—and subtler—than the proponents of loyalty programs claim,” say Werner Reinartz, Professor of Marketing at the University of Cologne, and V. Kumar, executive director of the Center for Excellence in Brand and Customer Management at Georgia State University’s J. Mack Robinson College of Business.

source: Harvard Business Review

“Specifically, we discovered little or no evidence to suggest that customers who purchase steadily from a company over time are necessarily cheaper to serve, less price sensitive, or particularly effective at bringing in new business,” they argue. The researchers find “no evidence” to support such claims.

In fact, some would argue, some potential buyers should be actively discouraged. In the colloquial, “there are some customers you do not want.”

source: Harvard Business Review

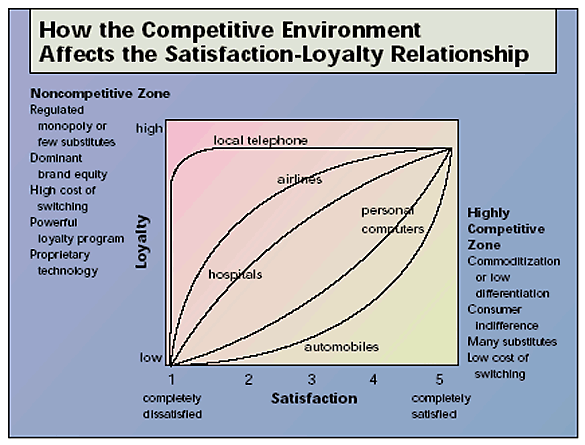

I’ve never been completely convinced that satisfaction and loyalty are related in a linear way, though. For starters, satisfaction and loyalty have different reference points.

“Customer satisfaction is a self-reported measure of how much customers ‘likes' a company and how happy they are with goods purchased or services obtained from the company,” says Mark Klein, Loyalty Builders CEO. “Customer loyalty, on the other hand, is a company-calculated metric of likelihood to purchase again or not defect to a competitor.”

Also, customers can “like” a product and yet buy a competitor’s offering, without having any change in a “satisfaction” score. “Just because they’re happy with their current brand doesn’t mean they won’t switch if a lower price is offered elsewhere,” notes Actionable Research.

Loyalty is what firms want, and satisfaction is seen as a proxy for loyalty. That might not generally be the case.

But some question net promoter score relevance and predictive power, as popular as NPS is in many firms. “Two 2007 studies analyzing thousands of customer interviews said NPS doesn’t correlate with revenue or predict customer behavior any better than other survey-based metric,” two reporters for the Wall Street Journal report. “A 2015 study examining data on 80,000 customers from hundreds of brands said the score doesn’t explain the way people allocate their money.”

Of all the criticisms, lack of predictive capability might be the most significant, since that is what the NPS purports to do: predict repeat buying behavior.

“The science behind NPS is bad,” says Timothy Keiningham, a marketing professor at St. John’s University in New York, and one of the co-authors of the three studies. “When people change their net promoter score, that has almost no relationship to how they divide their spending,” he said.

Others might argue that social media has changed the way consumers “refer” others to companies and products. Some question the methodology.

As valuable as the “loyalty drives profits” argument might be, it is reasonable to question how well the NPS, or any other metric purporting to demonstrate the causal effect of loyalty or satisfaction on repeat buying, actually can predict such behavior.

Some argue that “satisfaction” might not predict very much. What might have predictive value is “totally satisfied” customers. Mere “satisfaction” is not predictive of loyalty, in other words.

Xerox, for example, discovered that Its totally satisfied customers were six times more likely to repurchase Xerox products over the next 18 months than its satisfied customers. Merely satisfying customers is not enough to keep them loyal, in competitive markets.

In other words, “satisfied customers” can, and will, defect. Totally satisfied customers tend not to churn, and tend to buy more from any supplier.

source: Harvard Business Review

It might be hard to find anyone who believes there is no relationship between customer satisfaction and business outcomes. But the relationship might well be more complicated than we suppose.