All other things being equal, people and firms who have a choice are better served choosing to work in growing industries rather than declining ones. They arguably are best served choosing new and potentially fast-growing industries.

Likewise, connectivity providers would prefer to operate as "fast moving" innovators in new developing markets. The problem is that many such markets do not initially represent revenue scale, and for that reason are difficult for big firms to justify chasing.

Small firms have other problems, as they cannot generally compete successfully in any parts of the business that require scale (capital, people, large and extensive networks, lots of customer support). Any large connectivity market that requires scale are the best places for large tier-one providers to succeed.

That is more than a little troubling for firms and people in connectivity industries, and explains the common observation that "telcos cannot innovate."

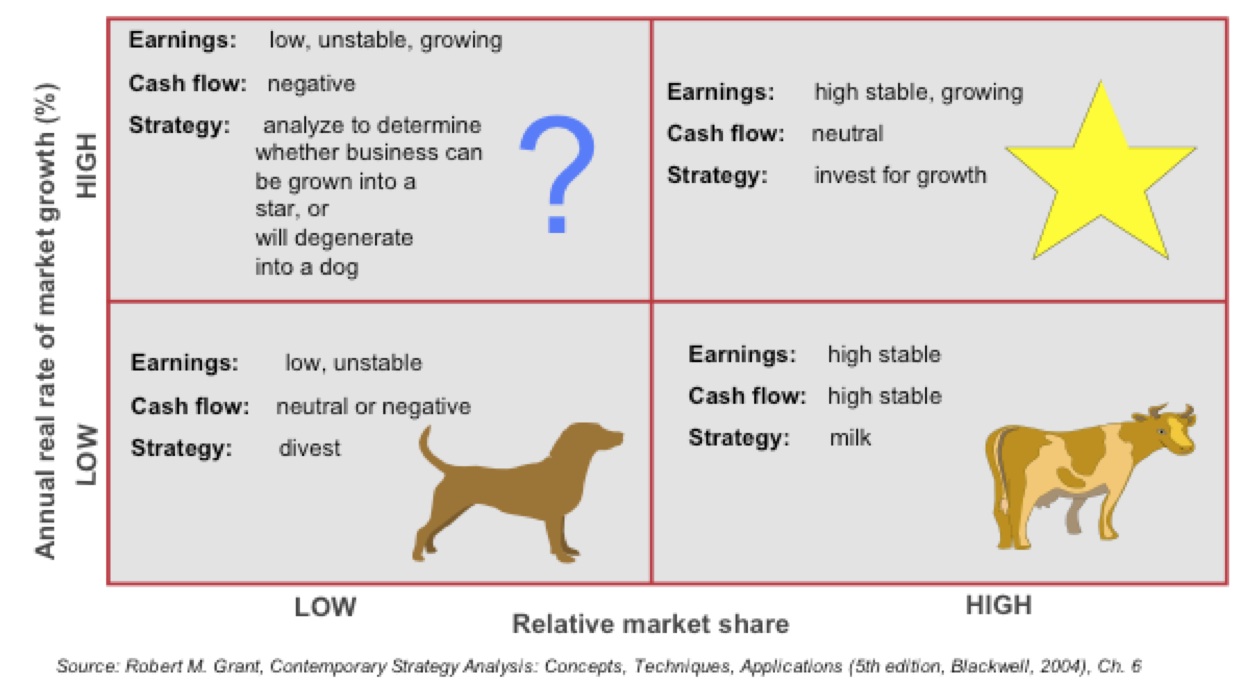

Until recently, mobile phone services have been an industry “star,” driving strong revenue growth. But mobile revenue growth rates are stalling, and overall global industry growth rates have dipped to somewhere between one percent and two percent annually (not adjusted for inflation).

source: GSMA

Other fixed network services have been “cash cows” at best, “dogs” at worst. For most of the 1990s, international long distance calling was a cash cow, whose revenues were to be harvested. In the second decade of the 21st century, voice services generally are products with shrinking demand, slim revenues and marginal--if any--profits.

New high growth markets are believed to exist in the internet of things and edge computing, but remain untested, and are “question marks.”

source: John Wiley, BCC

Over the past two decades, many potential lines of business have been proposed as growth engines, including VoIP, data center operations, app stores, entertainment video services, advertising, content ownership and cloud computing (to a smaller extent)/

Few of those initiatives have proven viable, with the exceptions, in some cases, of entertainment video and content ownership. There is much truth to the notion that “telcos cannot innovate,” but the broader observation might be the difficulty of carving out sustainable new roles in an ecosystem.

In a by-now familiar pattern, CSG notes that 79 percent of telecom executives are concerned about becoming commodity providers of “dumb pipe” services in an ecosystem where value and profit migrate elsewhere in the value chain.

Those beliefs also are clear in an Accenture white paper produced about digital transformation in the telecom industry by the World Economic Forum. To some extent, the industry’s problems are perhaps even deeper. Until recently, mobile subscription growth, and a shift of revenue drivers from voice to texting--then texting to mobile broadband--have been revenue “stars,” offering high rates of growth.

But the mobile market clearly is maturing, with negative to slow rates of growth in developed markets, and slowing growth rates in developing markets. Note that the present growth driver in developed markets--mobile broadband--has been slowing since 2008.

source: Researchgate

Subscriptions still have room to grow in developing markets, but at some point even those markets will saturate. So growth (revenue and accounts) is a key industry challenge.

Connectivity services firms with small market share have to compete differently from firms with large market share. For starters, small firms do not typically have access to huge amounts of capital, or the ability to hire huge numbers of people.

That means they always must find niches of one sort or another, specializing and segmenting their customer opportunities. Where tier-one service providers must “think big” when chasing new revenue sources, smaller firms have to “think small.”

Where a $1 billion opportunity is almost the bottom limit of what a tier-one service provider can try to address, a $1 billion opportunity is too large for many small firms to try and seize. Basically, the small firm strategy is to “go where the big guys will not follow” and will not try and compete.

Historically, that has been clear in segments such as enterprise phone switches, local area networking, Wi-Fi and specialty mobile segments, for example, where connectivity providers have been content to leave those segments to others.

The early broadband access market using digital subscriber line as the platform initially was left to independent retailers, for example. Prior to that, the dial-up internet access market similarly was left to third party providers.

LIkewise, small firms typically lack the resources to diversify into new parts of a value chain, innovate technologically or compete by offering superior credit policies or other financial inducements. They typically cannot be leaders in high-growth, low-share new markets with high investment costs and low sales volumes.

source: Robert Grant

Where small firms often can try and add value is by providing more intensive or customized support, especially for any market segments or products that are relatively low volume and routinely customized.

{kind=link}