How much will the new business-to-business environment post-Covid “normal” resemble either the “old” normal or the temporary pandemic normal? And to what degree will the new normal create new trends that affect business models?

The safest answer--based on history--is that the new normal will accentuate underlying trends in place before Covid, with incremental changes to business models for many businesses and industries. Most of us likely assume that the consumer and business shift to online behaviors--already underway before Covid--will be reinforced at a higher level.

That includes a shift to remote work and more collaboration at a distance. But that arguably will affect many industries and firms in an incremental way.

The bigger issue is whether some industries--such as airlines, cruise lines and hotels--might see big and permanent drops in demand, which will force big business model changes, including industry exit if markets shrink.

Some believe business travel, for example, will never return to pre-pandemic levels. That will have negative repercussions for hotels, airlines, trade shows, restaurants and associated industries.

If demand shrinks, so must operating costs and investment. Some business models might break altogether. Most trade shows will suffer; some will disappear.

Beyond all that, the question is whether any important new trends with business model implications--unseen before Covid--could be created. “Contact-less” procedures and business processes could be one example of a big new trend affecting many, if not all, place-based businesses.

Big financial and technology disruptions tend to have a big short term impact on business models--revenue and cost; customers and sales; products and services; production and distribution--and operating procedures.

The long-term impact is harder to gauge. Do disruptions such as recessions (economic cycles or deliberate result of government policies) cause new trends or only accelerate underlying trends.

Will some industries find demand permanently reduced or enhanced? Which industries might see permanent shrinkage? How will they cope? Beyond big demand changes, what are the more prosaic operational changes?

Will a shift to more “contact-less” retail commerce emerge as a permanent shift? And how much in-person retail shifts permanently to online ordering and fulfillment? How much will remote work and work from home persist? Will business travel be permanently reduced? If so, how do sales and marketing practices change?

The easy “answer” is that big recessions or pandemics accelerate trends already in place. You would have to search very hard to find a recession that actually reverses a key underlying trend.

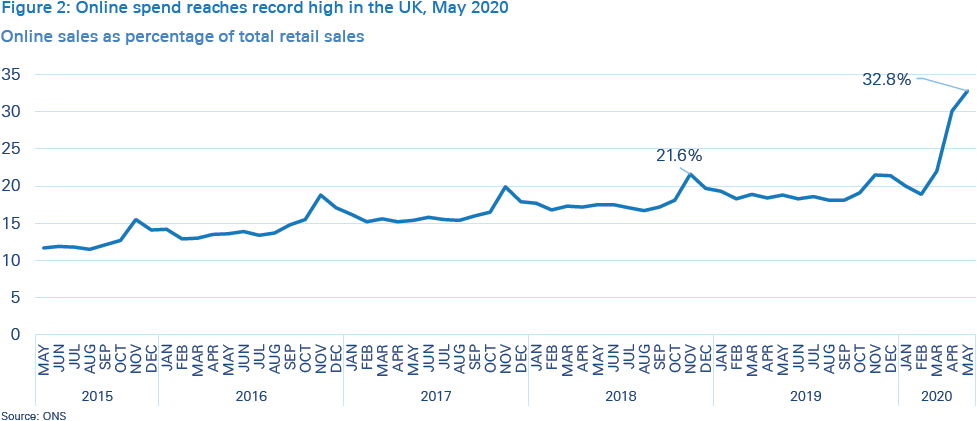

The obvious example is online retail spending, which in the United Kingdom, for example, sharply accelerated during the pandemic. The issue, of course, is how much reversion to the mean will occur once the pandemic is over.

The conventional wisdom seems to be that a permanent shift could occur. The magnitude of the shift is the issue, as is the timing of the shifts.

It is easier to show that recessions accelerate technology substitution than to illustrate new trend causation or at least correlation.

The short term effect is obvious: technology investment drops in the wake of a recession, even if firm professionals tend to believe the opposite.

In line with that expectation, there is some evidence that the Covid pandemic has caused firms hit by massive drops in demand to decrease digital technology investment, while firms able to continue operating have increased investment.

Retailers, for example, have remained open while cruise lines and theaters have been completely shut down, while other travel-related entities such as hotels and airlines have seen drops in demand above 70 percent. It obviously is easier to maintain investment when revenue has not been devastated.

Disparate investment in technology might easily be explained by relative differences in firm and industry revenue during the pandemic. Streaming services gained customers and revenue. Cloud computing sales increased, as did purchasing of broadband internet access services.

In contrast, it is hard to increase technology spending when a firm’s revenue has been reduced to zero or close to zero. As firms cut operating costs, their investments in technology also tend to be reduced.

source: A.D. Little