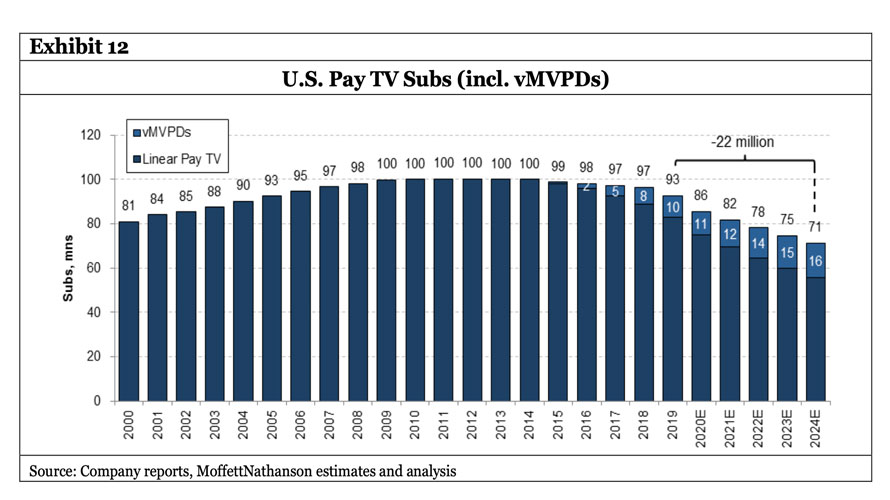

Subscription TV revenue appears poised to begin a faster and non-linear rate of decline, after relatively muted rates of change since revenue in the U.S. business peaked about 2011.

And that decline might hit both the subscription revenue stream as well as advertising, the twin drivers of revenue in the linear TV subscription business. To about 2025, forecasters believe the rate of decline of linear TV will accelerate.

Some believe the rate of decline--while accelerating--will only amount to about a 20 percent in the four years between 2020 and 2024, for example. That would be a relatively mild decline of about five percent a year. But that is significantly less than others believe will be the case.

source: MoffettNathanson

Linear TV ad spend, for example, is likely to drop more than 50 percent in the next five years, from $70 billion to roughly $34 billion, according to Ark Invest. Since ad buys are based on viewership, that suggests a drop in subscribers and viewing by half, as well, or a rate of decline between 13 percent and 16 percent per year.

source: Ark Invest

For most connectivity-based services, usage is correlated with perceptions of value, and ultimately is a sign of future consumer behavior, whether that be messaging, voice communications, data consumption or use of video services.

In that regard, a huge drop in linear video viewing has recently occurred, on the order of 50 percent in 2019 alone, ThinkNow Media says.

Convergence Research estimates 2020 U.S. linear video revenue declined six percent to $94.7 billion. The group forecasts a decline of 6.5 percent to $88.5 billion in 2021 and a decline of 10 percent in 2023 to $73.4 billion.

That rate of decline matters because any quantity that declines 6.5 percent a year is cut in half in 10 years. If the higher 10 percent attrition rate continues, linear video revenue is cut in half in less than seven years.

But the rate of change is accelerating, the group says. By about 2023, the rate of abandonment of linear video will reach 13 percent, Convergence Research estimates.

“At current run-rate OTT access revenue will exceed TV access revenue in 2024,” the group says.

Convergence Research estimates that US OTT revenue grew by 35 percent to $29.6 billion in 2020, and forecasts 35 percent growth to $39.9 billion for 2021, and $59.4 billion for 2023 (double 2020).

Convergence Research forecasts average OTT subscriptions will increase to five per OTT household in 2023, up from an average of three subscriptions in 2020.

All of that explains the high interest in growing video streaming services, the importance of broadband access in retail connectivity supplier business plans, the move by cable operators into the mobile business and the hopes many have for edge computing and internet of things as drivers of new revenue.

{kind=link}