The debate about the productivity of remote work will likely never be fully settled, in large part because it is so difficult, perhaps impossible, to measure knowledge worker or office worker productivity.

Whether knowledge worker productivity is up, down or flat is almost impossible to say, despite claims one way or the other. Much of the debate rests on subjective reports by remote workers themselves, not “more-objective” measures, assuming one could devise such measures.

Measuring intangible output is inherently more challenging than measuring output of physical goods. And some “test effect” occurs, at least temporarily. The output of workers who know they are being tested tends to rise during the period of the test.

There will always be room to contest managerial effectiveness at managing remote workers; the ability of workers to perform as well remotely as “in the office” and differences between workers (motivation and actual output).

There also will be room to contest the impact of heavy remote work on company culture; collaboration and other “soft” outcomes at levels beyond individual effort and output. Do work groups actually perform as well, or better, in remote work settings? Do companies benefit in other ways that are measurable and offset any potential costs?

And beyond all that, productivity arguably is an issue affecting broad swaths of the U.S economy, no matter what the form of work setting.

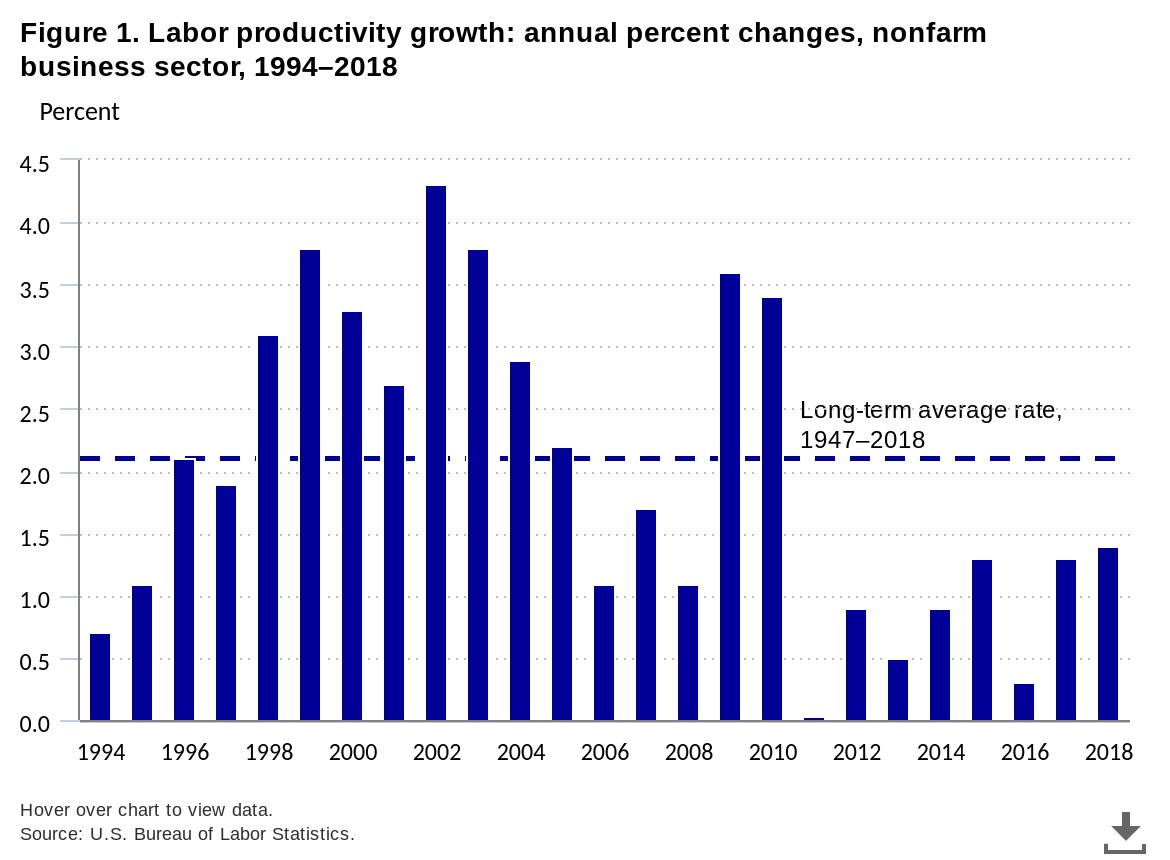

Productivity—defined as output per labor hour—has grown at a below-average rate since 2005, representing a dramatic reversal of the above-average growth of the late 1990s and early 2000s, according to the U.S. Bureau of Labor Statistics.

source: Bureau of Labor Statistics

Assume you believe the measurements are correct, and that non-farm productivity actually can be measured. Labor productivity compares the amount of goods and services produced (output) with the number of labor hours (inputs) used to produce those goods and services. Productivity is defined mathematically as output per hour of work, and growth occurs when output increases faster than labor hours.

As always, there are caveats. Such measures are not good at capturing hedonic improvements.

Hedonic qualIty adjustment is a method used by economists to adjust prices whenever the characteristics of the products included in the consumer price index change because of innovation. Hedonic quality adjustment also is used when older products are improved and become new products.

Hedonically adjusted price indices for broadband internet access in the U.S. market--adjusted for quality improvements such as speed--then looks like this:

source: Bureau of Labor Statistics

Also, the productivity of knowledge or office workers is very hard--perhaps impossible--to measure. Virtually any quantitative way of measuring “input” is only a supposed proxy for productivity itself.

Perhaps of notable significance are changes in “multi factor” inputs beyond capital investment and labor cost. That is where information technology, managerial skill, changes in goods produced or cultural changes apply.

The point is that the debate over “remote versus in-office work” is more about politics and emotion than economic facts. Firms can do it or not do it, but we should stop claiming we are motivated by clear economic facts.