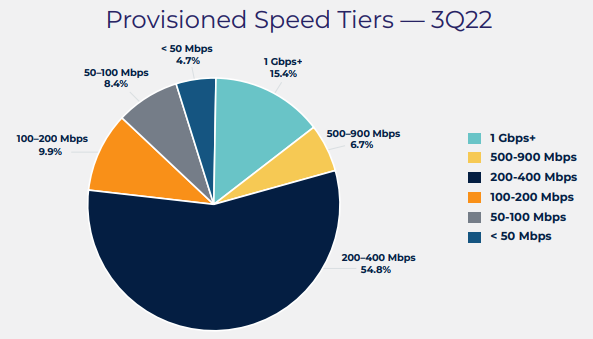

It is hard to answer the question “have home broadband prices risen since 2009?” with using hedonic adjustment and also adjusting for inflation. The Bureau of Labor Statistics uses hedonic adjustment to track producer prices for home broadband, for example, since speed and other attributes change over time.

The rationale is that a dial-up internet connection is not a comparable service to home broadband at various speeds (10 Mbps, 100 Mbps, 1 Gbps, for example). Since prices tend to stay about the same over time while speeds have increased for the “most bought” tiers of service, BLS adjusts prices to account for quality improvements.

source: Bureau of Labor Statistics

Trends for voice services are harder to track, as that feature is included in the recurring cost of both mobile and fixed network services. Over a few decades, the cost of fixed network voice services has tended to rise (as actual costs cannot be easily subsidized by higher-profit services, as once was the case).

The cost of mobile service has tended to drop over time. In October 2022, for example, the U.S. Bureau of Labor Statistics said the cost of mobile service dropped 1.4 percent, hedonically adjusted.

Home broadband also appears to have gotten cheaper by a bit in the September 2022 CPI report. That figure has to be interpreted, however, as the internet services category includes both internet access and other “electronic information providers.”

That includes subscriber fees for residential internet access, but also other online services such as web hosting, domain names, and file hosting for non-business use.

Also, this category includes service bundles that might include telephone and TV services bundled with residential internet service and mobile internet access. Obviously, each of those separate services has a distinct retail cost profile that can skew the figure for what we assume “home broadband” actually costs.

Other monthly subscriber fees are also included in the but are not limited to internet rental equipment, Wi-Fi service fees, installation and activation fees, and other associated taxes and fees.

That noted, we might note that service bundles mean lower prices per product, even when some components such as home telephone service might have rising cost profiles.

Determining what most customers actually pay does require some analysis of the service plans people actually buy, not simply the posted retail prices. If most customers buy bundles, their costs per service are lower than if they purchased each component separately.

Still, using the BLS data, we can see a dramatic fall in U.S. internet access prices since about 2017, when hedonically adjusted.