The Federal Communications Commission appears to be ready to license some spectrum, as part of its proposed national broadband plan, for free or very-low-cost access. It is not clear whether the agency envisions giving a single national operator the entire frequency block, whether it will license the spectrum for free or for fee, or whether the plan mirrors other proposals that have been advanced.

FCC statement

The FCC has provided no additional details, but the thought is not new. Outgoing Federal Communications Commission Chairman Kevin Martin in 2008 had pushed for action on a plan to offer free, pornography-free wireless Internet service to about 95 percent of the country, using about 6 MHz of spectrum in a block of about 25 MHz. The licensee would have been free to create a revenue-generating plan using about 19 MHz.

The FCC's proposal mirrored a plan offered by M2Z Networks, which has been proposing

providing free, wireless, family-friendly service at speeds of 512 kbps, providing a basic and relatively slow 384 kbps for downloads and 128 kbps for uploads.

M2Z Networks had proposed using AWS-3 spectrum in the 2155-2180 MHz band.

Advertising revenue would support the free service, while M2Z also proposed offering faster "for fee" services at speeds up to 3 Mbps.

M2Z also has said it would pay the government about five percent of revenues from such a service.

Showing posts with label broadband plan. Show all posts

Showing posts with label broadband plan. Show all posts

Tuesday, March 9, 2010

FCC to Propose Spectrum for "Free or Low Cost" Broadband Access

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, March 5, 2010

What Does 100 Mbps for 100 Million Homes Imply About Monthly Prices?

There are only two major problems with the Federal Communication Commission's upcoming National Broadband Plan, says Dan Hays, PRTM director. The aspirational goal of 100 Mbps service provided to 100 milliion U.S. homes by 2020 is a fine aspirational goal, but it isn't clear how it can be implemented, he says.

The other big initiative is in the wireless area, specificially the effort to get TV broadcasters to give up 500 megahertz worth of spectrum so that wireless service providers can use it.

And there are just two problems there: buyers and sellers. Are there willing buyers? Are there willing sellers? Hays says the broadcasters already have said they are unwilling to sell. Even if they do agree to sell, the cost to acquire that much spectrum would be quite expensive, coming at a time when service providers are straining to justify further investments in their fixed plant.

The 100-Mbps access plan likewise has just two problems: who will pay for the investments, and whether end users are willing to pay substantially more than they now do for the upgraded speeds.

Estimates of how much that might cost range from a wildly-low $25 billion up to $350 billion, says Hays.

Commercial organizations aren't terribly interested in investing now to provide speeds that high, as there is little consumer willingness to pay much more than what people pay today, Hays says.

The percentage of household income spent on communications in the United States is in line with the rest of the world today, he says. So it does not make sense to assume a step level change in spending even if much-higher speeds are made available.

Beyond that, there is a generational and cultural issue at work. A good percentage of broadband non-adopters are older than 65. But as younger users who "cannot live without broadband" move up the age cohort, that particular non-adoption issue fixes itself, says Hays.

Once upon a time one could hear many doubters about why people would buy cable TV when they could get off-air video for no incremental cost. Over time, people decided they really did need it. The same thing has been at work with mobility services and will be true of broadband as well.

None of this is to argue that, over time, access speeds will increase. But investment capital cannot be raised unless there is a plausible business case. So the catch is that investors will want to see some plausible evidence that $300 billion worth of investment will lead to a return on investment.

Assume there are 65 million U.S. households spending $40 a month, on average, for broadband. That works out to about $2.6 billion a month, or $31 billion a year.

Assume a base of about 115 million U.S. households. Assume 90 percent broadband penetration, or 104 million connected homes. That would represent about $4.2 billion in monthly spending, or about $50 billion in consumer revenue.

How much incremental revenue would an investor want to see to justify investing $300 billion? Assume a 15 percent return as a hurdle rate and 104 million customer households.

The debt service implied is $45 billion a year. Assume borrowers also want to repay the principal over a 10-year period. That would very roughly imply a need to earn an incremental $75 billion a year.

Assume 40-percent margins. That implies gross incremental revenue has to be about $187.5 billion a year, or $1630 per customer, or an additional $136 per customer, per month. That implies a monthly price of at least $175 a month.

Do you really think every broadband customer in America, at 90 percent penetration of homes, is willing to pay $175 a month for broadband access?

Of course, maybe I have blown the math here. If not, I think 100 Mbps access, using networks built with private capital, are unlikely to happen. It would require consumers to do something history and logic suggests they will not do.

The other big initiative is in the wireless area, specificially the effort to get TV broadcasters to give up 500 megahertz worth of spectrum so that wireless service providers can use it.

And there are just two problems there: buyers and sellers. Are there willing buyers? Are there willing sellers? Hays says the broadcasters already have said they are unwilling to sell. Even if they do agree to sell, the cost to acquire that much spectrum would be quite expensive, coming at a time when service providers are straining to justify further investments in their fixed plant.

The 100-Mbps access plan likewise has just two problems: who will pay for the investments, and whether end users are willing to pay substantially more than they now do for the upgraded speeds.

Estimates of how much that might cost range from a wildly-low $25 billion up to $350 billion, says Hays.

Commercial organizations aren't terribly interested in investing now to provide speeds that high, as there is little consumer willingness to pay much more than what people pay today, Hays says.

The percentage of household income spent on communications in the United States is in line with the rest of the world today, he says. So it does not make sense to assume a step level change in spending even if much-higher speeds are made available.

Beyond that, there is a generational and cultural issue at work. A good percentage of broadband non-adopters are older than 65. But as younger users who "cannot live without broadband" move up the age cohort, that particular non-adoption issue fixes itself, says Hays.

Once upon a time one could hear many doubters about why people would buy cable TV when they could get off-air video for no incremental cost. Over time, people decided they really did need it. The same thing has been at work with mobility services and will be true of broadband as well.

None of this is to argue that, over time, access speeds will increase. But investment capital cannot be raised unless there is a plausible business case. So the catch is that investors will want to see some plausible evidence that $300 billion worth of investment will lead to a return on investment.

Assume there are 65 million U.S. households spending $40 a month, on average, for broadband. That works out to about $2.6 billion a month, or $31 billion a year.

Assume a base of about 115 million U.S. households. Assume 90 percent broadband penetration, or 104 million connected homes. That would represent about $4.2 billion in monthly spending, or about $50 billion in consumer revenue.

How much incremental revenue would an investor want to see to justify investing $300 billion? Assume a 15 percent return as a hurdle rate and 104 million customer households.

The debt service implied is $45 billion a year. Assume borrowers also want to repay the principal over a 10-year period. That would very roughly imply a need to earn an incremental $75 billion a year.

Assume 40-percent margins. That implies gross incremental revenue has to be about $187.5 billion a year, or $1630 per customer, or an additional $136 per customer, per month. That implies a monthly price of at least $175 a month.

Do you really think every broadband customer in America, at 90 percent penetration of homes, is willing to pay $175 a month for broadband access?

Of course, maybe I have blown the math here. If not, I think 100 Mbps access, using networks built with private capital, are unlikely to happen. It would require consumers to do something history and logic suggests they will not do.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, March 3, 2010

Telecom Return on Investment: Implications for Broadband Policy

In business terms, that means the largest, best-financed U.S. communications providers face a worsening situation, not a rosy and growing market.

Unless a person believes the U.S. government has access to enough capital to reinvent 90 percent to 95 percent of the nation's infrastructure, something that might cost $300 billion or more, policymakers are going to have to rely on the private sector to do the heavy lifting.

Though we are yet weeks away from knowing what the Federal Communications Commission actually will attempt to achieve as a "national broadband policy," we are years away from knowing how it all will work out.

The reason is that sweeping changes of this sort always result in years of litigation, even once rules are set.

It seems fairly safe to argue that, whatever emerges, the rules will not be as bad as service providers fear, nor as good as some policy proponents would like. So long as the nation requires private firms and private capital to do the vast proportion of the work, policies that negatively affect investment will doom the effort.

Nobody will be completely happy when the rules are announced, or modified and litigated. But rational policymakers will not kill the golden goose. And service providers likely will face some changes they would rather not have to confront. That's just the way these things work.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sunday, February 28, 2010

Regulatory Pendulum Swings: But Which Way?

It has been apparent for a couple of years that the regulatory pendulum in the the U.S. telecom arena was swinging towards more regulation.

What now is unclear, though, is whether such new rules will largely revolve around consumer protection and copyright or might extend further into fundamental business practices.

Current Federal Communications Commission inquiries into wireless handset subsidies and contract bundling, application of wireline Internet policies to service wireless providers, as well as the creation of new "network neutrality" rules are examples.

But so will the settting of a national broadband policy likely result in more regulation. And there are some voices calling for regulating broadband access, which always has been viewed as a non-regulated data service, as a common carrier service.

One example is a recent speech given by Lawrence Strickling, National Telecommunications and Information Administration assistant secretary, to the Media Institute.

He said the United States faces "an increasingly urgent set of questions regarding the roles of the commercial sector, civil society, governments, and multi-stakeholder institutions in the very dynamic evolution of the Internet."

Strickling notes that “leaving the Internet alone” has been the nation’s Internet policy since the Internet was first commercialized in the mid-1990s. The primary government imperative then was just to get out of the way to encourage its growth.

"This was the right policy for the United States in the early stages of the Internet," Strickling said. "But that was then and this is now."

Policy isues have ben growing since 2001, he argued, namely privacy, security and copyright infringement. For that reason, "I don’t think any of you in this room really believe that we should leave the Internet alone," he said.

In a clear shift away from market-based operation, Strickling said the Internet has "no natural laws to guide it."

And Strickling pointed to security, copyright, peering and packet discrimination. So government has to get involved, he said, for NTIA particilarly on issues relating to "trust" for users on the Internet.

Those issues represent relatively minor new regulatory moves. But they are illustrative of the wider shift of government thinking. Of course, the question must be asked: how stable is the climate?

Generally speaking, changes of political party at the presidential level have directly affected the climate for telecom policy frameworks. And while a year ago it might have seemed likely that telecom policy was clearly headed for a much more intrusive policy regime, all that now is unclear.

A reasonable and informed person might have argued in November 2008 that "more regulation" was going to be a trend lasting a period of at least eight years, and probably longer, possibly decades.

None of that is certain any longer. All of which means the trend towards more regulation, though on the current agenda, is itself an unstable development. One might wonder whether it is going to last much longer.

That is not to say some issues, such as copyright protection or consumer protection from identity theft. for example, might not continue to get attention in any case. But the re-regulatory drift on much-larger questions, such as whether broadband is a data or common carrier service, or whether wireless and cable operators should be common carriers, might not continue along the same path.

You can make your own decision about whether those are good or bad things. The point is that presidential elections matter, and the outcome of the 2012 election no longer is certain.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, February 17, 2010

100 Mbps for 100 Million Homes by 2020?

If Federal Communications Commission Chairman Julius Genachowski gets his way, the FCC will set a goal of 100-Mbps service delivered to 100 milliion American homes by 2020.

Genachowski says his preferred approach to a national broadband policy would require ISPs to offer minimum home connection speeds by 2020. The “100 Squared” initiative might in fact be too modest a goal, he suggests.

"We should stretch beyond 100 megabits," he adds.

The proposal is part of the FCC's national broadband plan, due for initial public comment in March 2010.

The goal is sure to come under some scrutiny by service providers, in part because there is not currently any way to provide bandwidth of that magnitude on a national basis while pricing service at rates most consumers would pay.

There is not enough usable wireless spectrum to provide that kind of coverage and usage, and fixed access networks are not completely or primarily subject to Moore's Law. While chipsets and processors do get faster, the cost of digging trenches does not get less expensive over time. In fact, construction cost is the dominant cost element for any optical network providing service directly to end users.

"One hundred meg is just a dream," says Qwest Communications International Inc Chief Executive Edward Mueller. "We couldn't afford it."

Few customers now buy 50-Mbps services where such speeds are available, in large part because the cost is in the triple-digits range. Proponents might argue that the goal is 100 Mbps for not much more money than people now pay for 4 Mbps or 7 Mbps service, but it is hard to envision how even "free" opto-electronices could support such a value-price combination.

In other words, even if all the active elements actually were provided for free, could service providers actually build ubiquitous networks offering 100 Mbps or faster speeds, and price in middle-double digits? So far, the answer appears to be negative.

About 60 percent of the cost of building an FTTH network is construction work, ducts and cables, not to mention cabinets, power supplies and other network elements. Still, in some dense areas, it might be possible to do so, since the construction and cable might amount to about $1200 per home passed. Again, keep in mind we assume totally free opto-electronics.

In suburban areas the business case is marginal, at best, since about $2400 might have to be spent on construction and passive elements.

Since the FCC goal only calls for connecting 100 million homes out of possibly 113 million, we can safely assume the cost of most rural networks of such capacity need not be considered.

Of course, opto-electronics are not "free." But the point is that construction costs, were nothing else an issue, would still be a tough proposition, if the goal is very high speed access at prices most consumers would pay.

American consumers will be paying more for broadband in the future, if for no other reason than that most mobile plans will require it, and those charges will be paid for on a "per-device" basis, not "per home."

What seems improbable is that U.S. consumers are willing to increase overall broadband spending by an order of magnitude (10 times) to have 100 Mbps or faster service on a fixed basis.

One can of course argue from history. Prices for lower-speed broadband services have declined over time, while the prices for the faster tiers have remained stable, but speeds have increased. The issue is how much price compression is possible.

"In order to earn a return for investors, you have to be conscious of what consumers will pay. I don't know this is something consumers will pay for," Piper Jaffray analyst Christopher Larsen says. "It's a nice goal, but it's a little on the over ambitious side."

Having a "stretch goal" is fine. Firm mandates, though, might run smack up against stubborn consumer willingness to pay and the fixed costs of building access infrastructure.

Genachowski says his preferred approach to a national broadband policy would require ISPs to offer minimum home connection speeds by 2020. The “100 Squared” initiative might in fact be too modest a goal, he suggests.

"We should stretch beyond 100 megabits," he adds.

The proposal is part of the FCC's national broadband plan, due for initial public comment in March 2010.

The goal is sure to come under some scrutiny by service providers, in part because there is not currently any way to provide bandwidth of that magnitude on a national basis while pricing service at rates most consumers would pay.

There is not enough usable wireless spectrum to provide that kind of coverage and usage, and fixed access networks are not completely or primarily subject to Moore's Law. While chipsets and processors do get faster, the cost of digging trenches does not get less expensive over time. In fact, construction cost is the dominant cost element for any optical network providing service directly to end users.

"One hundred meg is just a dream," says Qwest Communications International Inc Chief Executive Edward Mueller. "We couldn't afford it."

Few customers now buy 50-Mbps services where such speeds are available, in large part because the cost is in the triple-digits range. Proponents might argue that the goal is 100 Mbps for not much more money than people now pay for 4 Mbps or 7 Mbps service, but it is hard to envision how even "free" opto-electronices could support such a value-price combination.

In other words, even if all the active elements actually were provided for free, could service providers actually build ubiquitous networks offering 100 Mbps or faster speeds, and price in middle-double digits? So far, the answer appears to be negative.

About 60 percent of the cost of building an FTTH network is construction work, ducts and cables, not to mention cabinets, power supplies and other network elements. Still, in some dense areas, it might be possible to do so, since the construction and cable might amount to about $1200 per home passed. Again, keep in mind we assume totally free opto-electronics.

In suburban areas the business case is marginal, at best, since about $2400 might have to be spent on construction and passive elements.

Since the FCC goal only calls for connecting 100 million homes out of possibly 113 million, we can safely assume the cost of most rural networks of such capacity need not be considered.

Of course, opto-electronics are not "free." But the point is that construction costs, were nothing else an issue, would still be a tough proposition, if the goal is very high speed access at prices most consumers would pay.

American consumers will be paying more for broadband in the future, if for no other reason than that most mobile plans will require it, and those charges will be paid for on a "per-device" basis, not "per home."

What seems improbable is that U.S. consumers are willing to increase overall broadband spending by an order of magnitude (10 times) to have 100 Mbps or faster service on a fixed basis.

One can of course argue from history. Prices for lower-speed broadband services have declined over time, while the prices for the faster tiers have remained stable, but speeds have increased. The issue is how much price compression is possible.

"In order to earn a return for investors, you have to be conscious of what consumers will pay. I don't know this is something consumers will pay for," Piper Jaffray analyst Christopher Larsen says. "It's a nice goal, but it's a little on the over ambitious side."

Having a "stretch goal" is fine. Firm mandates, though, might run smack up against stubborn consumer willingness to pay and the fixed costs of building access infrastructure.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, December 22, 2009

64% of U.S. Broadband Connections Now are Mobile

There are more mobile broadband subscriptions in service in the U.S. market than fixed line.

The CTIA notes that there are now 103 million mobile broadband customers in the United States, according to Informa Telecom and Media. There are more than 58 million fixed line subscribers, according to Insight Research Corp.

By that measure, there are 161 million U.S. broadband subscriptions. So mobile connections represent 64 percent of broadband connections now in use. And mobile broadband has exploded over the last 18 months.

In June 2008, mobile broadband accounted for more than 59 million high speed subscribers, about 45 percent of all broadband connection in the United States, according to the Federal Communications Commission.

Clearly, any effort to create a national U.S. broadband policy would have to recognize the leading role wireless now plays.

The CTIA notes that there are now 103 million mobile broadband customers in the United States, according to Informa Telecom and Media. There are more than 58 million fixed line subscribers, according to Insight Research Corp.

By that measure, there are 161 million U.S. broadband subscriptions. So mobile connections represent 64 percent of broadband connections now in use. And mobile broadband has exploded over the last 18 months.

In June 2008, mobile broadband accounted for more than 59 million high speed subscribers, about 45 percent of all broadband connection in the United States, according to the Federal Communications Commission.

Clearly, any effort to create a national U.S. broadband policy would have to recognize the leading role wireless now plays.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, November 24, 2009

Do Usage Caps for Wireless and Mobile Broadband Make Sense?

Consumers say 60 percent of the wireless broadband decision is based on two factors: monthly recurring charge and existence or size of a usage cap. For that reason, "data caps" are a particularly unfriendly way to manage overall traffic, says Yankee Group analyst Philip Marshall.

A better approach, from a service provider perspective, is to offer unlimited usage and then manage traffic usingreal-time, network intelligence-based solutions like deep packet inspection and policy enforcement, Marshall argues.

Some would argue that fair use policies that throttle maximum speeds when policies are violated is no picnic, either. But temporary limits on consumption, only at peak hours of usage, arguably is more consumer friendly than absolute caps with overage charges.

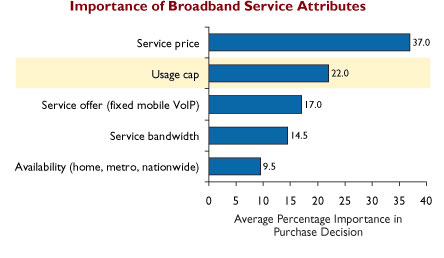

To test consumer preferences, Yankee Group conducted a custom survey that included a "choice-based conjoint analysis," which allowed Yankee Group analysts to estimate the relative importance to consumers of key wireless broadband service attributes. The survey was taken by 1,000 mobile consumers who also use broadband access services.

From the conjoint analysis, "we found that, on average, 59 percent of a wireless broadband purchase decision depends on two factors: service price, and the presence or absence of a 2 GByte per month usage cap," Marshall says.

The results also indicate that 14.5 percent of a typical purchase decision is affected by service bandwidth, and that the implied average revenue per user lift when increasing bandwidth from 768 Kbps to 2 Mbps ranges between $5 and $10 per month.

The results also indicate, however, that there are diminishing returns for service plans that offer speeds above 3 Mbps, though speed increases might be useful for other reasons, such as competitive positioning.

"Our price elasticity analysis implies that consumers are willing to pay $25 to $30 more per month for plans that offer unlimited usage, compared to plans that have a 2 GBytes a month usage cap," says Marshall.

"In a competitive operating environment, consumers will tend to migrate toward higher bandwidth services, all else being equal, but they are not necessarily willing to pay a significant premium for the added performance capability," says Marshall.

Our most recent survey results indicate that consumers require 2 Mbps to 3 Mbps bandwidth for their broadband service. This is likely to increase dramatically over the next two to three years, but the consumer survey suggests dramatically-higher bandwidth does not affect decisions as much as recurring price and existence of bandwidth caps.

For example, when offered a choice between one package featuring a 2 GByte per month usage cap with 6 Mbps bandwidth, and another package with unlimited monthly usage but just 2 Mbps service speed, 63 percent of consumers opted for the 2 Mbps service with no cap.

Even when the choice is between an unlimited package offering only 768 Kbps bandwidth, compared to an alternative plan with 6 Mbps bandwidth and a 2 GByte per month usage cap, 57 percent preferred the 768 kbps package.

Service providers still must manage bandwidth demand though, with or without usage caps

Usage caps work to regulate demand, but users do not like them.

The other approach is not to impose the usage caps, but instead to use policy managment and deep packet inspection to manage traffic flows.

If such solutions are implemented in a non-discriminatory manner, so that all like services are treated equally, they can be implemented irrespective of network neutrality regimes currently under consideration, Marshall believes.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, April 10, 2009

Investment Incentives Key for National Broadband Plan, McDowell Says

As part of the recently passed American Recovery and Reinvestment Act of 2009 ("stimulus package"), the Federal Communications Commission must create a national broadband plan.

Commissioner Robert McDowell says “it is essential that our plan give current and prospective broadband network and service providers the proper incentives to deploy new technologies."

"We must also provide entrepreneurs with the flexibility to make full use of all available spectrum, including the television white spaces, to backhaul broadband traffic," McDowell says. "In order to attract investors to fund the build-out of new networks, we must not engage in rulemakings that produce whimsical regulatory arbitrage."

"Rather, we must allow market players to succeed or fail on their own merits and not due to the government picking winners and losers," McDowell says. "In short, our rules must allow network operators to have a reasonable opportunity to pay back their investors. That’s the only way to improve existing networks and build new ones.”

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Broadband is Partly an Availability Problem; Partly a Demand Problem

"Predominantly, even in contexts with reliable supply of broadband, it is consumer demand for broadband that is the tallest barrier to adoption and represents America’s competitive vulnerability," says Connected Nation.

It might be worth keeping that in mind as plans for the broadband stimulus program operated by the National Telecommunications & Administration and Agriculture Department's "broadband stimulus" rules are finalized.

There clearly is a physical access problem in rural areas (at least in terms of wired access: though some locations may not have clear line of sight, multiple providers of satellite access are available, and it is possible to supply speeds up to perhaps 5 Mbps using satellite), but broadband availability is not the same problem as lack of adoption. In fact, people have lots of reasons not to buy services they already have access to.

The largest barrier to broadband adoption is a lack of awareness about broadband’s benefits, Connected Nation says. Nearly one-half (44 percent) of those with no home broadband connection say “I don’t need broadband.”

Likewise, the top barrier to computer ownership is also a perceived lack of need. Nearly two-thirds

(62 percent) of those who do not own a computer say “I don’t need a computer,” Connected Nation says.

In other cases, perceived cost is an issue. Nearly one fourth (24 percent) of those who do not own a computer cite the up-front cost as a barrier. Similarly, nearly one-fourth of those without a home broadband connection say broadband is too expensive.

Four out of ten parents with children who are without a home computer see no need for having a computer in the home. And nearly one-third (30 percent) of parents with children who do not have a home broadband connection see no need for a broadband connection.

More than one half (56 percent) of people with disabilities who do not own a computer see no need for having a computer in the home. Four out of ten people with disabilities who do not have a home broadband connection see no need for a broadband connection, Connected Nation says.

Close to one half (42 percent) of rural residents without a home broadband connection say it is because they do not need broadband. This compares with 19 percent of these rural residents who say they do not subscribe because broadband service is not available in their area.

Additionally, 22 percent of these rural residents say broadband is too expensive.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, April 8, 2009

More Qualms About Broadband Stimulus: This Time From Small Rural Telcos

Large U.S. telcos have their doubts about whether it will make any sense at all to apply for any funds under the National Telecommunications & Information Administration's portion of "broadband stimulus" funds, and generally are barred from applying under the Rural Utilities Service rules.

It appears small, independent, rural telcos have similar qualms. Attendees at a MetaSwitch Forum workshop on the broadband stimulus plan were shaking their heads in disbelief about "strings" attached to receipt of funds under the RUS plan, in particular the nebulous language about investments in access that allow multiple providers to compete.

Depending on how the final rules shape up, it is conceivable that most telcos and cable companies will decide not to participate directly.

It appears small, independent, rural telcos have similar qualms. Attendees at a MetaSwitch Forum workshop on the broadband stimulus plan were shaking their heads in disbelief about "strings" attached to receipt of funds under the RUS plan, in particular the nebulous language about investments in access that allow multiple providers to compete.

Depending on how the final rules shape up, it is conceivable that most telcos and cable companies will decide not to participate directly.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Titanic Battle Shaping Up over Broadband

As busy as people are trying to prepare for the imminent opening of the first of three proposal submission windows for funds authorized by the American Reinvestment and Recovery Act ("broadband stimulus"), a bigger food fight will begin to break out next year as the Federal Communications Commission opens a new rule-making on a national broadband strategy. As much attention as the broadband stimulus program is getting, it is going to be dwarfed by any new framework that emerges from the FCC effort.

The stimulus money is a temporary "shot in the arm." In fact, some question whether there will be much of any long-term impact from the majority of the money that ultimately is allocated, in jobs, an identifiable uptick in broadband use or economic growth.

Any new national broadband policy will reshape the broadband marketplace, creating new winners and losers on the supplier and reshaping the financial terrain for existing and would-be contestants, in ways that contribute "in a material way," to use the financial term, to the health of virtually all service providers, software and hardware suppliers.

Specifically, the FCC now is charged, by statute, to determine how tax dollars will be spent on deploying and upgrading Internet access across the United States. Telcos large and small--and their suppliers--have huge stakes in how those rules are recast. And make no mistake: current business models, revenue streams and company valuations are at stake.

The FCC's responsibility is also to update policies and regulations that have conspicuously failed to keep pace with changes in communications technologies and the different ways in which the US public actually get their phone, cable TV and Internet services.

It would not be overstating the case to say we will witness the biggest single change to U.S. communications regulation since either the 1934 Communications Act, or the Telecom Act of 1996, each of which has been foundational for shaping the U.S. communications environment.

As some of us have been arguing for a half decade or more, it is likely that regulators will be looking at greater structural change involving a form of structural or functional separation, developments which already have occurred in Europe and now are happening in Southeast Asia, and which has happened on a small scale in the United States as well, principally in Rochester, N.Y., where Rochester Telephone agreed to form a new wholesale access company providing local loop services to all licensed providers.

That move will be fiercely resisted by most telcos, you can be sure, as it formally breaks up the vertically-integrated model historically the mainstay in the U.S. market. Cable operators have to worry that they will, for the first time, also be forced to provide widespread wholesale access to competitors as well, something the cable industry always has opposed but which will be hard to avoid if other key providers are required to do so.

Small telcos face equally-large challenges, as a shift to broadband concerns might necessarily reshape rural investment rules in ways that directly harm the existing voice revenue support many hundreds of companies now rely on to support their firms. For hundreds of independent and rural companies, that government support is the single largest income category, vastly outstripping actual direct end user revenues.

The other potential changes are new requirements for minimum bandwidth, control of network management practices and a wide variety of business-model-shaping changes.

If you have any familiarity with the on-going disputes about universal service funds, or the intense pressure created by the debates leading up to the Telecom Act, you have some idea of what is about to happen.

Oddly enough, you will find widespread sentiment that the Telecom Act failed. But you will not find many human beings that believe their own choices, value or communications richness now are worse than they were before the Act was passed. What is clear is the foundational impact any rules changes will have on competitor fortunes. Still, an early prediction: no matter what ultimately happens, no matter which sectors claim they have "won or lost," end users will have richer options than before, with or without rules changes. But rules changes are inevitable.

The stimulus money is a temporary "shot in the arm." In fact, some question whether there will be much of any long-term impact from the majority of the money that ultimately is allocated, in jobs, an identifiable uptick in broadband use or economic growth.

Any new national broadband policy will reshape the broadband marketplace, creating new winners and losers on the supplier and reshaping the financial terrain for existing and would-be contestants, in ways that contribute "in a material way," to use the financial term, to the health of virtually all service providers, software and hardware suppliers.

Specifically, the FCC now is charged, by statute, to determine how tax dollars will be spent on deploying and upgrading Internet access across the United States. Telcos large and small--and their suppliers--have huge stakes in how those rules are recast. And make no mistake: current business models, revenue streams and company valuations are at stake.

The FCC's responsibility is also to update policies and regulations that have conspicuously failed to keep pace with changes in communications technologies and the different ways in which the US public actually get their phone, cable TV and Internet services.

It would not be overstating the case to say we will witness the biggest single change to U.S. communications regulation since either the 1934 Communications Act, or the Telecom Act of 1996, each of which has been foundational for shaping the U.S. communications environment.

As some of us have been arguing for a half decade or more, it is likely that regulators will be looking at greater structural change involving a form of structural or functional separation, developments which already have occurred in Europe and now are happening in Southeast Asia, and which has happened on a small scale in the United States as well, principally in Rochester, N.Y., where Rochester Telephone agreed to form a new wholesale access company providing local loop services to all licensed providers.

That move will be fiercely resisted by most telcos, you can be sure, as it formally breaks up the vertically-integrated model historically the mainstay in the U.S. market. Cable operators have to worry that they will, for the first time, also be forced to provide widespread wholesale access to competitors as well, something the cable industry always has opposed but which will be hard to avoid if other key providers are required to do so.

Small telcos face equally-large challenges, as a shift to broadband concerns might necessarily reshape rural investment rules in ways that directly harm the existing voice revenue support many hundreds of companies now rely on to support their firms. For hundreds of independent and rural companies, that government support is the single largest income category, vastly outstripping actual direct end user revenues.

The other potential changes are new requirements for minimum bandwidth, control of network management practices and a wide variety of business-model-shaping changes.

If you have any familiarity with the on-going disputes about universal service funds, or the intense pressure created by the debates leading up to the Telecom Act, you have some idea of what is about to happen.

Oddly enough, you will find widespread sentiment that the Telecom Act failed. But you will not find many human beings that believe their own choices, value or communications richness now are worse than they were before the Act was passed. What is clear is the foundational impact any rules changes will have on competitor fortunes. Still, an early prediction: no matter what ultimately happens, no matter which sectors claim they have "won or lost," end users will have richer options than before, with or without rules changes. But rules changes are inevitable.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

Are GPUs Essentially a Subscription?

Are graphics processing units more akin to a subscription than “capital investment?” Think about your own smartphone purchases. Yes, it is ...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Financial analysts typically express concern when any firm’s customer base is too concentrated. Consider that, In 2024, CoreWeave’s top two ...