Sometimes the truth emerges even when not intended; at times even when the opposite argument is being made. Consider the argument for gradual introduction of more optical fiber into hybrid fiber coax networks, which is sound thinking.

Though making that case, one optical supplier executive has said that “connectivity is increasingly transforming from static wireline to mobile or wireless delivery,” said Cate McNaught, Corning Optical Communications emerging applications market development manager.

That is not to say fixed network access is going away, or will not underpin wireless or mobile network backhaul (fronthaul, anyhaul). It is to acknowledge that content and video consumption on mobile and untethered devices seems to be the main trend right now, with mobile over the top video services proliferating, and more content supplied by all OTT services being consumed on mobile devices.

The issue then is not the need for more optical fiber in access networks, but the business models and rationale for doing so. The problem is stranded assets Today, fiber to the home networks in the U.S. market strands as much as 60 percent of the deployed FTTH capital. That creates a bigger return on investment problem.

Consumer spending on communications and entertainment services has not changed all that much, in most countries, although the specific products purchased have changed.

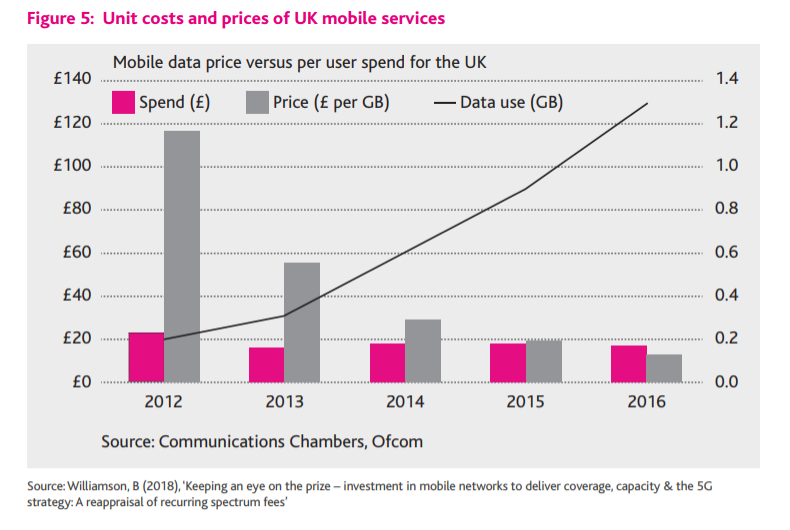

At the same time, the profit margin from many services also has compressed. Prices per gigabyte for consumers using internet access services have declined by about an order of magnitude since 2012, in the U.K. market, for example.

The stranded assets problem simply is that when a ubiquitous network is built, not every single home or business buys every service. Not every consumer buys fixed network voice, entertainment video or internet access. Not every business buys the same mix of voice and data services, or mobility.

The problem really is compounded, however, as multiple suppliers compete. If the demand for any single product is 95 percent, and there are three competent suppliers, on average, any supplier can only expect to get revenue from 32 percent of locations passed by the network.

In other words, 68 percent of locations passed earn no revenue.

Such problems can intensify when the demand curve changes, as when consumers abandon use of fixed network voice in favor of mobile voice. The remedy, up to this point, has been product bundles.

One set of numbers from the Comcast third quarter 2017 results is instructive: Comcast details the number of customers taking single, dual-product and three-product or four-product packages.

About 30 percent of consumer customers buy just one product, a third buy two products, while 37 percent buy three or four products as a bundle. Looking at each buy as a “unit sold,” those figures help service providers deal with stranded assets.

If 37 percent of Comcast customers buy an average 3.5 products, that equates to an average of 1.3 products per home passed. If 33 percent buy two products, that equates to one unit sold across 66 percent of the homes passed. The 30 percent of homes that buy only a single product, when added to the dual-product homes, equate to one product sold to 96 percent of homes passed. Altogether, those figures mean Comcast sells an average of two products per home passed.

And that is how the economics work, even when stranded assets range from 40 percent to 60 percent.

The business model will come under more stress if and when mobile alternatives emerge more strongly. So two apparently contradictory claims can be made: there will be a growing need for more access optical fiber, and there also will be less need for some of it.

The remaining customers will need optical fiber advantages more; but fewer customers will buy.