To be sure, those figures represent a "best guess" made by Stanford professor Jonathan Koomey.

Thursday, August 4, 2011

Google runs 900,000 servers, uses 0.01% of world's electricity

Google runs 900,000 servers that possibly consume u0.01 percent of worldwide electricity, compared to data centers as a whole, which account for up to 1.5 percent of worldwide electricity use, and as much as 2.2 percent of U.S. electricity.

To be sure, those figures represent a "best guess" made by Stanford professor Jonathan Koomey.

To be sure, those figures represent a "best guess" made by Stanford professor Jonathan Koomey.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, August 3, 2011

Windstream Purchase of PAETEC Has Broader Lessons

Windstream Corp.'s acquisition of PAETEC Holding Corp. illustrates one key element of business strategy for most service providers of any size in the U.S. and other global markets. The $2.3 billion deal gives Windstream a bigger profile in business customer services, arguably a more-important revenue source for any fixed-line service provider, given the cable industry's growing success in the consumer services market.

The acquisition also illustrates the generally paltry returns available to most service providers in their legacy geographic footprints. Generally speaking, the largest tier-one telcos, mobile service providers, small rural telcos and competitive local exchange carriers have been able to get significant growth in subscribers and revenue over the last decade largely by growing outside their original service territories. Read more here.

The need to go "out of region" is not just a strategic imperative for tier-one global providers. It applies to small telcos, competitive local exchange carriers and mobile service providers as well.

Few remember it, but Rochester Telephone, an independent telco operating in Rochester, N.Y., once wanted to get into the competitive long distance business badly enough to trade away its local access monopoly, breaking itself up into a "wholesale" infrastructure company and a separate retail entity that bought network service from the wholesale company just like any other competitor in the market.

More recently, SingTel decided to give up its local monopoly in the same way Rochester Tel did, in exchange for freedom to deploy its capital in other international markets. But note the business driver: SingTel cannot achieve the growth it expects and wants if it stays a provider of services in Singapore. Perhaps 90 percent of current revenue already comes from "out of region" operations.

Windstream says the deal provides more opportunity in strategic growth areas for Windstream, including IP-based services, data centers, cloud computing and managed services. A stronger presence in the important business market is key. But the acquisition also gets Windstream into new geographic markets as well.

The acquisition also illustrates the generally paltry returns available to most service providers in their legacy geographic footprints. Generally speaking, the largest tier-one telcos, mobile service providers, small rural telcos and competitive local exchange carriers have been able to get significant growth in subscribers and revenue over the last decade largely by growing outside their original service territories. Read more here.

The need to go "out of region" is not just a strategic imperative for tier-one global providers. It applies to small telcos, competitive local exchange carriers and mobile service providers as well.

Few remember it, but Rochester Telephone, an independent telco operating in Rochester, N.Y., once wanted to get into the competitive long distance business badly enough to trade away its local access monopoly, breaking itself up into a "wholesale" infrastructure company and a separate retail entity that bought network service from the wholesale company just like any other competitor in the market.

More recently, SingTel decided to give up its local monopoly in the same way Rochester Tel did, in exchange for freedom to deploy its capital in other international markets. But note the business driver: SingTel cannot achieve the growth it expects and wants if it stays a provider of services in Singapore. Perhaps 90 percent of current revenue already comes from "out of region" operations.

Windstream says the deal provides more opportunity in strategic growth areas for Windstream, including IP-based services, data centers, cloud computing and managed services. A stronger presence in the important business market is key. But the acquisition also gets Windstream into new geographic markets as well.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Mobile Operator Radio Costs to Grow 7 Times to 2016

According to Juniper Research, even after adding more-efficient Long Term Evolution networks, global mobile operator costs to deliver user data could surpass $370 billion annually by 2016, a seven-fold increase on their 2010 level of $53 billion.

That might be a generalized problem for fixed networks as well, on both capital and operating cost fronts.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

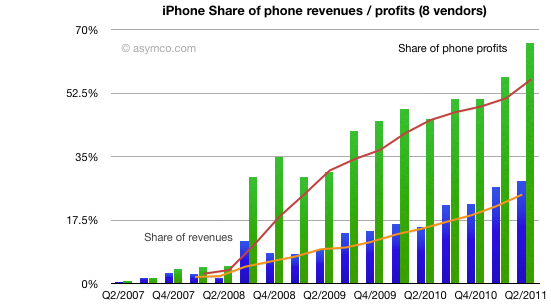

Apple Gets 66% of Handset Profits

Apple gets two thirds of total industry profit share in the handset arena, despite getting only about 28 percent share of device sales. Apple share of phone revenues increased to 28%

Apple gets two thirds of total industry profit share in the handset arena, despite getting only about 28 percent share of device sales. Apple share of phone revenues increased to 28%

Read more here as well.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Low ROI Blunts Mobile Marketing Adoption

A new study conducted by The Relevancy Group in June 2011 and commissioned by Pontiflex, finds that lack of return on investment from mobile advertising is the biggest deterrent for marketers when it comes to increasing mobile ad spending in 2011.

Some 43 percent of marketers who aren't planning to increase their mobile ad spending this year say low ROI from mobile advertising is the top reason that they won't increase spending. The survey also found that 93 percent of marketers said they would increase mobile ad spending if they realized a higher return on their investment.

Some 43 percent of marketers who aren't planning to increase their mobile ad spending this year say low ROI from mobile advertising is the top reason that they won't increase spending. The survey also found that 93 percent of marketers said they would increase mobile ad spending if they realized a higher return on their investment.

Other survey results indicate that marketers are dissatisfied with click-based mobile advertising. The Relevancy Group survey found that 56 percent of Fortune 500 marketers are dissatisfied with or don't use click-based mobile advertising.

Some 43 percent of marketers who aren't planning to increase their mobile ad spending this year say low ROI from mobile advertising is the top reason that they won't increase spending. The survey also found that 93 percent of marketers said they would increase mobile ad spending if they realized a higher return on their investment.

Some 43 percent of marketers who aren't planning to increase their mobile ad spending this year say low ROI from mobile advertising is the top reason that they won't increase spending. The survey also found that 93 percent of marketers said they would increase mobile ad spending if they realized a higher return on their investment. Other survey results indicate that marketers are dissatisfied with click-based mobile advertising. The Relevancy Group survey found that 56 percent of Fortune 500 marketers are dissatisfied with or don't use click-based mobile advertising.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Comcast Won't Compete for Over the Top Video Customers Outside its Franchise Areas

Comcast Corp. says it will not offer streaming video services that can be purchased by customers outside its own franchise areas.

The economic hurdle is too great for the operator to consider going over the top with subscription streaming video services that would compete not only with Netflix, but with other cable TV operators, according to As Comcast Chairman and CEO Brian Roberts.

The economic hurdle is too great for the operator to consider going over the top with subscription streaming video services that would compete not only with Netflix, but with other cable TV operators, according to As Comcast Chairman and CEO Brian Roberts.

If you know the cable industry, you knew he would say that. Cable companies simply do not compete with each other.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, August 2, 2011

U.S. ISPs Deliver 82% to 114% of Advertised Speeds

In its new report on broadband access performance of 13 Internet service providers representing 86 percent of U.S. subscribers, the Federal Communicartions Commission found that actual download speeds are substantially closer to advertised speeds than was found in data from early 2009.

On average, during peak periods, digital subscriber line services delivered download speeds that were 82 percent of advertised speeds, cable-based services delivered 93 percent of advertised speeds, and fiber-to-the-home services delivered 114 percent of advertised speeds. Verizon's FiOS average real-world speeds were actually higher than advertised speeds, both over a 24-hour period and during peak surfing hours. Other high-ranking ISPs include Comcast and Cox.

During peak periods, speeds decreased from 24-hour average speeds by 0.4 percent for fiber-to-the-home services, 5.5 percent for DSL-based services, and 7.3 percent for cable-based services.

Peak period download speeds varied from a high of 114 percent of advertised speed to a low of 54 percent of advertised speed.

Peak period performance results for upload speeds were similar to or better than those for download speeds. Upload speeds were not significantly affected during peak periods, showing an average decrease of only 0.7 percent from the 24-hour average speed.

On average, DSL-based services delivered 95 percent of advertised upload speeds, cable-based services delivered 108 percent, and fiber-to-the-home services delivered 112 percent.

Upload speeds among ISPs ranged from a low of 85 percent of advertised speed to a high of 125 percent of advertised speed.

On average, during peak periods, digital subscriber line services delivered download speeds that were 82 percent of advertised speeds, cable-based services delivered 93 percent of advertised speeds, and fiber-to-the-home services delivered 114 percent of advertised speeds. Verizon's FiOS average real-world speeds were actually higher than advertised speeds, both over a 24-hour period and during peak surfing hours. Other high-ranking ISPs include Comcast and Cox.

During peak periods, speeds decreased from 24-hour average speeds by 0.4 percent for fiber-to-the-home services, 5.5 percent for DSL-based services, and 7.3 percent for cable-based services.

Peak period download speeds varied from a high of 114 percent of advertised speed to a low of 54 percent of advertised speed.

Peak period performance results for upload speeds were similar to or better than those for download speeds. Upload speeds were not significantly affected during peak periods, showing an average decrease of only 0.7 percent from the 24-hour average speed.

On average, DSL-based services delivered 95 percent of advertised upload speeds, cable-based services delivered 108 percent, and fiber-to-the-home services delivered 112 percent.

Upload speeds among ISPs ranged from a low of 85 percent of advertised speed to a high of 125 percent of advertised speed.

The Free Press predictably chose to focus on the gaps. "While the study indicates some providers are consistently delivering their customers the promised network speeds, it reveals that many providers are falling well short of their advertised claims." ISPs Fail to Deliver Advertised Broadband Speeds

On average, during peak periods, digital subscriber line services delivered download speeds that were 82 percent of advertised speeds, cable-based services delivered 93 percent of advertised speeds, and fiber-to-the-home services delivered 114 percent of advertised speeds.

During peak periods, speeds decreased from 24-hour average speeds by 0.4 percent for fiber-to-the-home services, 5.5 percent for DSL-based services, and 7.3 percent for cable-based services. Read the report here.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Are Smart Phones, 4G Bad for Smaller Wireless Providers?

It is no secret that the costs of marketing smart phones are higher than was the case for feature phones, and that is true for carriers large and small.

MetroPCS has also seen its costs rise much more steeply than its profits, for example. Its cost per gross addition reached $177.88 in the second quarter, up about eight percent, and its average revenue per user rose to $40.49, up just over 1.6 percent. Read more.

The growing dominance of AT&T and Verizon Wireless in the U.S. market has been said to threaten Sprint, but does nothing to help either MetroPCS or Leap, argues 24/7wallstreet.

A merger of MetroPCS and Leap is likely only to delay their inevitable demise. Both AT&T and Verizon Wireless offer pre-paid phones, and though the pre-paid service is not their preferred business, the two giants could pretty easily eliminate MetroPCS and Leap.

MetroPCS has also seen its costs rise much more steeply than its profits, for example. Its cost per gross addition reached $177.88 in the second quarter, up about eight percent, and its average revenue per user rose to $40.49, up just over 1.6 percent. Read more.

The growing dominance of AT&T and Verizon Wireless in the U.S. market has been said to threaten Sprint, but does nothing to help either MetroPCS or Leap, argues 24/7wallstreet.

A merger of MetroPCS and Leap is likely only to delay their inevitable demise. Both AT&T and Verizon Wireless offer pre-paid phones, and though the pre-paid service is not their preferred business, the two giants could pretty easily eliminate MetroPCS and Leap.

One is reminded of what the advent of broadband did to independent Internet service providers in the dial-up era. Once the broadband shift began, dial-up ISPs found they no longer could compete, as the costs of providing broadband access were higher than dial-up, destroying profit margins.

It might be the case that smart phones and fourth-generation services might have similar impact on many smaller mobile providers, resellers and channel partners.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Trans-Pacific Circuit Prices Plunge

Trans-Pacific capacity prices have plummeted over the past two years, says TeleGeography.

Trans-Pacific capacity prices have plummeted over the past two years, says TeleGeography.Between the second quarter of 2009 and second quarter of 2011, the median monthly lease price for a 10 Gbps wavelength from Los Angeles to Tokyo fell 63 percent, from $98,500 to $36,000.

Prices are tumbling on other trans-Pacific routes as well. Over the past 12 months, median 10 Gbps wavelength prices from Los Angeles to Singapore fell 33 percent, while Hong Kong-Los Angeles 10 Gbps prices declined 39 percent.

Three new cable systems are probably the reason for the sharp price declines. The Asia-America Gateway (2008), Trans-Pacific Express (2009), and Unity (2010) cable systems have increased supply, with the predictable effects on pricing.

Industry executives have been relatively optimistic in public about "rational" pricing behavior in the capacity markets. Some will argue faster price declines are to be expected when new capacity comes online. Generally speaking, price-per-megabit prices drop 20 percent or so each year, so a decline, on a per-megabit basis, is not unusual. The sharper declines on trans-Pacific routes, though, suggest pricing pressure will be more significant than usual, for a while.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Data Center Electricity Consumption Grows More Slowly Than Expected

Data center power consumption has grown significantly less than predicted over the past few years, largely due to the 2008 economic crisis, according to a new study.

The study, carried out by Jonathan Koomey, a consulting professor in the civil and environmental engineering department at Stanford University, found that electricity used by data centers worldwide increased by about 56 percent from 2005 to 2010.

Data center electricity use doubled from 2000 to 2005 and a study by the U.S. Environmental Protection Agency predicted power consumption would double again from 2005 to 2010.

The study, carried out by Jonathan Koomey, a consulting professor in the civil and environmental engineering department at Stanford University, found that electricity used by data centers worldwide increased by about 56 percent from 2005 to 2010.

Data center electricity use doubled from 2000 to 2005 and a study by the U.S. Environmental Protection Agency predicted power consumption would double again from 2005 to 2010.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Visa launches mobile payments in Indonesia

"Visa has launched "m-saku," a mobile payment application for Visa card users who also have Blackberry and Nexian phones in Indonesia.

The application also provides offers such as discounts for m-saku users from certain merchants, as well as a mobile payment function available at participating merchant locations.

M-saku allows users to top up their cellular credit, pay bills, buy tickets and shop online using their smart phones.

The application also provides offers such as discounts for m-saku users from certain merchants, as well as a mobile payment function available at participating merchant locations.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

QFPay Readies Chinese "Square"

QFPay, a Beijing-based company providing a payments solution similar to Square, is coming out of stealth mode. QFPay enables users to pay with bank cards swiped on mobile devices.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Verizon Partners with American Express for "Serve" Mobile Payments

Verizon Wireless will be supporting the American Express "Serve" system for mobile phone payments, in addition to its support of Isis, the wallet joint venture with AT&T and T-Mobile USA.

Serve enables users to send and receive money from mobile devices, using accounts provided by Amex, and is different from other systems designed for use at retail locations only.

The partnership means Verizon mobile uers will be able to use the "Serve" payment system on mobile phones and tablet computers. Sprint also is working with American Express to support Serve for its users.

Serve enables users to send and receive money from mobile devices, using accounts provided by Amex, and is different from other systems designed for use at retail locations only.

Verizon, American Express Partner on Mobile Payments (subscription required)

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Mobile Payments Won't Save Consumers Money, Says Consumer Reports

In many cases, consumers using their mobile devices to pay for purchases will not find they are saving money, Consumer Reports argues. In most cases, retailers won't be saving money, either.

Most of the new electronic payment options are tied to credit and debit cards, so whatever costs consumers or retailers normally incur when using their plastic will find the same charges are incurred in a "pay by mobile phone" context as well.

Google Wallet merchant transaction fees are the same as those charged on plastic payments, and the same is expected to be true for Visa's digital wallet. Square and PayPal Mobile charge merchants even more than the average big bank fee, 2.75 and 2.9 percent of the transaction amount, respectively.

Among payment processors Consumer Reports looked at, only Obopay charges consumers (not merchants) an explicit flat 50-cent fee for payments over $10. You can transfer funds to your Obopay account from a bank account at no cost, but if you link a transaction to a debit or credit card, you'll pay a 1.5 percent fee. So on a $100 payment, fees can run from 50 cents to $2.

Among payment processors Consumer Reports looked at, only Obopay charges consumers (not merchants) an explicit flat 50-cent fee for payments over $10. You can transfer funds to your Obopay account from a bank account at no cost, but if you link a transaction to a debit or credit card, you'll pay a 1.5 percent fee. So on a $100 payment, fees can run from 50 cents to $2.

That should raise an immediate question: what's the value to end users of paying by mobile phone instead of credit or debit card? The answer will be obvious in a few cases, but more obscure in most cases. Paying for public transportation is one of the scenarios where the ability to simply waive a phone near a terminal will provide value by saving consumers the time spent waiting in line to buy tickets or recharge current fare cards.

In other cases one might argue consumers can save a bit of time checking out by "swiping a phone" instead of a card. But many will find that a minor value, if a value at all. That's one reason interest in "wallet" approaches that use the mobile to store credentials and target offers of value to users seems to be growing. Getting a discount or other incentive provides the "value."

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Amazon Getting into Social Shopping

Social shopping sites (mobile coupons, group offers or deal of the day services) have proliferated since Groupon started getting traction. Now Amazon.com has launched its own deal-of-the-day service in Chicago, the Wall Street Journal reports. Amazon Getting into Social Shopping (subscription required).

Google has started slowly rolling out its own Groupon-like offerings see Google Offers.

Social couponing, or social shopping, sometimes called "deal of the day," is becoming a serious business, but it also is easy to dismiss. It's just coupons, right? Maybe not. The coupon is the tactic used to aggregate buyers. It is a rival channel to alternative coupon channels and other forms of local advertising and promotion.

The group-buying industry is expected to grow 138 percent to $2.66 billion in 2011. The business is highly fragmented at the moment, with some estimating there are about 439 daily deal email programs serving the U.S. market in the first quarter of 2011.

Nor is social shopping just a nice or interesting stand-alone business. Many believe it will increasingly be integrated with mobile payments, mobile loyalty mechanisms and other targeted forms of advertising and promotion. Read more here.

Google has started slowly rolling out its own Groupon-like offerings see Google Offers.

Social couponing, or social shopping, sometimes called "deal of the day," is becoming a serious business, but it also is easy to dismiss. It's just coupons, right? Maybe not. The coupon is the tactic used to aggregate buyers. It is a rival channel to alternative coupon channels and other forms of local advertising and promotion.

The group-buying industry is expected to grow 138 percent to $2.66 billion in 2011. The business is highly fragmented at the moment, with some estimating there are about 439 daily deal email programs serving the U.S. market in the first quarter of 2011.

Nor is social shopping just a nice or interesting stand-alone business. Many believe it will increasingly be integrated with mobile payments, mobile loyalty mechanisms and other targeted forms of advertising and promotion. Read more here.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

U.S. Productivity is Rising, but AI Doesn't Seem the Reason

U.S. productivity has been rising for several years, but artificial intelligence is probably not the reason, at least, not yet. According t...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Financial analysts typically express concern when any firm’s customer base is too concentrated. Consider that, In 2024, CoreWeave’s top two ...