For most of its 150-year history, the telecom business has had to sell an intangible product, with few proxies for value and few ways to create a "hot" emotional connection with customers. As value as "dial tone" might be, what consumer is emotionally involved with the product?

That changed with the introduction of the Apple iPhone. For the first time in its history, telcos have a physical embodiment of service with which consumers do have emotional connection. The problem, some executives will note, is that the bond is with the third party device, not the service provider or service. That's correct.

Still, for those who have been waiting for some way to create high emotional engagement with an intangible communications service, iPhone is the closest proxy in 150 years. And that matters.

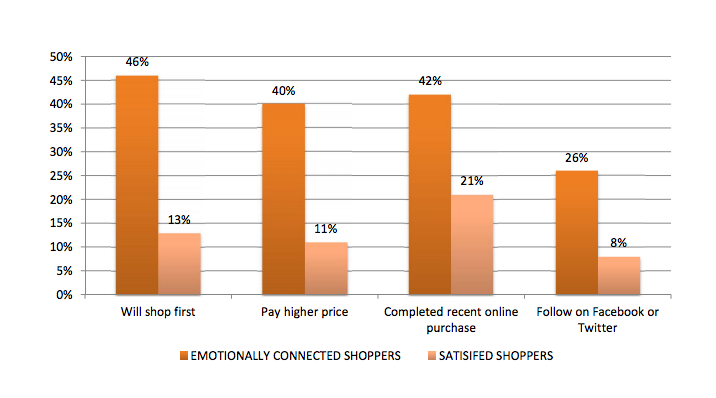

Recent data from Motista illustrated the top emotional drivers behind retail purchases in the fourth quarter of 2011 were more motivated by “fun” and “comfort in life,” reflecting an emotional need they want from their retailers.

The data also compared satisfied consumers to emotionally connected consumers, and forty-six percent of emotionally connected shoppers indicated they always shop a particular retailer first compared to only 13 percent of “satisfied” shoppers. In other words, emotionally connected shoppers are four times more likely to shop a particular retailer first.

Emotional involvement makes a huge difference.