One rule of thumb used by venture capital investors when assessing technology firms is to look for an order of magnitude better user experience. That rule sometimes is expressed as an order of magnitude better technology performance.

Using that measuring stick, one might argue that, whatever the initial expectations, magazine and newspaper experiences with mobile apps for smart phones and tablets have delivered “end user experience” that is problematic, compared to Amazon’s experience with books.

At the same time, from a provider perspective, mobile apps that were expected to recast newspaper and magazine readership and revenue have proven more complicated than offline publishing, have cost more than expected and provide less profit than expected.

Amazon, on the other hand, arguably has focused on selling digital content with characteristics that are more congruent with the offline end user experience, at costs more controllable and predictable.

While one might argue that tablet and smart phone content availability is not an order of magnitude more valuable to end users than offline versions of those products, one might well argue that the digital versions of songs, videos and books that Amazon sells provide more value than the digital subscriptions magazines and newspapers have tried to sell.

Also, in terms of the “native app versus Web” delivery formats, some content products are better suited, or equally well suited, to Web distribution, compared to app distribution.

Some of the same fundamental questions must be asked of other new mobile businesses that take offline processes, such as shopping, paying and banking, and attempt to create new mobile versions of those products.

Mass adoption will hinge on whether end users perceive dramatically-better experiences, whether we can quantify how much better those experiences are. The notion of “dramatically better” is akin to “order of magnitude” change that can induce massive end user behavior change, while the “incrementally better” notion, with incremental new hassle, is not likely to lead to behavior change.

Looking only at magazine and newspaper apps, there are issues that illustrate the hurdles. Apple’s 30-percent slice of gross revenue is a problem for suppliers, since that is higher than the typical profit margin for a newspaper or magazine publisher. Irrespective of end user experience, it arguably is a “profitless” exercise to sell a digital magazine or newspaper subscription when the revenue split gives a distributor 30 percent of gross revenue.

Among other complications, though, were how publishers could comply with their normal auditing standards used for offline publications, Technology Review notes.

Nor, oddly enough, did mobile apps represent a particularly easy publishing format. Tablets, and some smart phones, support both a "portrait" (vertical) and "landscape" (horizontal) view, depending on how the user held the device.

Then, too, the screens of smart phones were much smaller than those of tablets.

So many publishers ended up producing six different versions of their editorial product: a print publication, a conventional digital replica for Web browsers and proprietary software, a digital replica for landscape viewing on tablets, something that was not quite a digital replica for portrait viewing on tablets, a kind of hack for smart phones, and ordinary HTML pages for their websites.

Not surprisingly, app development costs were unexpected.

But the real problem, some might argue, is that end users expect an online “link rich” experience when using an app for content consumption, much as they expect with Web-based content consumption.

That conflicts with the walled garden that a newspaper or magazine represents. In one sense, a magazine or newspaper is like a compact disc, a collection of items, whereas people increasingly expect to consume items one at a time, in random fashion.

Fundamentally, people consuming in an online channel are looking for songs, not albums. They are looking for stories, not collections.

The point is that transitioning from offline products to mobile products sometimes is not just a matter of authoring, design and software development. Sometimes the product has to be different when it is a mobile-consumed product, not an offline product.

There are many analogies. A mobile payment capability, for example, has to offer an experience that is qualitatively and significantly better than paying with cash or a credit card. It can’t be a little better. It has to be a lot better. And that means it cannot be new experience that is just seconds faster.

There has to be something about the experience that is much better. Maybe a user won’t be able to quantify the changes so easily. But they have to sense that the “new thing” is really lots better than the “old thing.” Slight little improvements won’t motivate change.

You might argue that Square, and other merchant point of sale services offered by Intuit and PayPal have gotten such big traction because they were those sorts of “vastly better” experiences, allowing small retailers to take credit card and debit card payments where they never could do so before.

Something like that will happen for every successful mobile app and use case, period. But most apps and experiences do not represent that sort of clear advantage for end users. Tablets and smart phones, on the other hand, clearly have succeeded in offering user experience and value much better than users had before.

Without such value, new revenue models and businesses will not succeed in the mobile realm.

Wednesday, May 9, 2012

Is Your Mobile Product Providing 10x Better User Experience? If Not, Odds of Failure are High

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, May 8, 2012

Why "Mobile First" Makes Sense for So Many App, Content, Device, Service Providers

According to some projections, mobile Internet usage will overtake desktop usage before 2015. That's why a "mobile first" strategy makes so much sense.

Microsoft Tag recently attempted to sum up this constantly changing space with a single infographic.

Microsoft Tag recently attempted to sum up this constantly changing space with a single infographic.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Amobee: the Biggest Mobile Ad Platform in the Mobile Service Provider Business

The typical professional working in the telecom business can be forgiven for not knowing mobile advertising platform Amobee, any more than the typical professional knows all that much about the details of all the other myriad of activities routinely conducted by tier-one mobile service providers globally.

So here are a couple of quick reasons tier-one service providers need to know about Amobee. First, Amobee is a mobile advertising platform designed from the ground up to enable mobile service provider advertising operations, functioning intentionally as a digital ad agency, not just an ad network.

Second, Amobee is owned by Singtel, which operates in some 20 countries throughout Asia and serves 434 million mobile customers and has investments in Bharti Airtel (India), Telkomsel (Indonesia), Globe Telecom (the Philippines), Advanced Info Service (Thailand), Warid Telecom (Pakistan) and PBTL (Bangladesh).

Third, Amobee’s client roster includes Nokia, BMW, AOL, eBay, Zynga, Skype, Google and Barnes & Noble.

In other words, Amobee is carrier friendly, built to scale and already has shown traction with some of the biggest names in advertising.

In mobile advertising, as in everything else a tier-one service provider does, scale matters. To really be financially interesting, a tier-one service provider needs revenue opportunities of some size.

In mobile advertising, that means the biggest brands, with the biggest budgets, which is why Amobee has been built essentially as a digital version of a Madison Avenue agency.

Amobee, owned by parent Singtel, was intentionally created as the digital and mobile equivalent of a Madison Avenue agency, not an “advertising network.” Amobee also was created with a global clientele in mind, the sort of advertiser that might very well need to support its products in countries on many continents.

That is quite a daunting task. Ignore for the moment the need for “creative” approaches for different cultures, in many languages. The simple act of placing ads (“insertions”) on a number of mobile networks in each separate country, plus many different mobile advertising networks, and you get some idea of the sheer complexity.

The whole idea is to make the task of reaching huge mobile audiences efficiently, working with one contact point, not dozens to scores of different mobile companies and similar numbers of ad networks to get the required coverage.

Consider that between the Singtel audience of 434 million, and screens served by other customers Vodafone and Telefonica, the Amobee reach is about a billion people. That’s serious scale.

In the latest news, Amobee has acquired a 3D specialist operation known as Adjitsu, a feature Admobee CEO Trevor Healy believes will provide an edge in a young mobile ad business that nevertheless, from a creative point of view, “can be quite static and pedestrian.”

The other very-practical angle is that one thing a brand does not want is a viewer immersed in a 3D program to suddenly find themselves watching either a high-definition or standard-definition video ad, if video is the ad format the advertiser prefers.

So here are a couple of quick reasons tier-one service providers need to know about Amobee. First, Amobee is a mobile advertising platform designed from the ground up to enable mobile service provider advertising operations, functioning intentionally as a digital ad agency, not just an ad network.

Second, Amobee is owned by Singtel, which operates in some 20 countries throughout Asia and serves 434 million mobile customers and has investments in Bharti Airtel (India), Telkomsel (Indonesia), Globe Telecom (the Philippines), Advanced Info Service (Thailand), Warid Telecom (Pakistan) and PBTL (Bangladesh).

Third, Amobee’s client roster includes Nokia, BMW, AOL, eBay, Zynga, Skype, Google and Barnes & Noble.

In other words, Amobee is carrier friendly, built to scale and already has shown traction with some of the biggest names in advertising.

In mobile advertising, as in everything else a tier-one service provider does, scale matters. To really be financially interesting, a tier-one service provider needs revenue opportunities of some size.

In mobile advertising, that means the biggest brands, with the biggest budgets, which is why Amobee has been built essentially as a digital version of a Madison Avenue agency.

Amobee, owned by parent Singtel, was intentionally created as the digital and mobile equivalent of a Madison Avenue agency, not an “advertising network.” Amobee also was created with a global clientele in mind, the sort of advertiser that might very well need to support its products in countries on many continents.

That is quite a daunting task. Ignore for the moment the need for “creative” approaches for different cultures, in many languages. The simple act of placing ads (“insertions”) on a number of mobile networks in each separate country, plus many different mobile advertising networks, and you get some idea of the sheer complexity.

The whole idea is to make the task of reaching huge mobile audiences efficiently, working with one contact point, not dozens to scores of different mobile companies and similar numbers of ad networks to get the required coverage.

Consider that between the Singtel audience of 434 million, and screens served by other customers Vodafone and Telefonica, the Amobee reach is about a billion people. That’s serious scale.

In the latest news, Amobee has acquired a 3D specialist operation known as Adjitsu, a feature Admobee CEO Trevor Healy believes will provide an edge in a young mobile ad business that nevertheless, from a creative point of view, “can be quite static and pedestrian.”

The other very-practical angle is that one thing a brand does not want is a viewer immersed in a 3D program to suddenly find themselves watching either a high-definition or standard-definition video ad, if video is the ad format the advertiser prefers.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tablets Win Because 75% of All PC Use is Content Consumption, Sharing

Tablets, at least in developed markets, are not direct substitutes for personal computers, though they are substitutes for many of the key activities people also can do on PCs.

Tablets, at least in developed markets, are not direct substitutes for personal computers, though they are substitutes for many of the key activities people also can do on PCs. Most early surveys suggest that people owning tablets also own PCs, making the tablet a new device in the consumer electronics environment, not generally a replacement for a PC.

Content consumption is the reason tablets potentially can displace most of the functions of a PC.

Some surveys also suggest that 75 percent of activities conducted on PCs consist of content consumption or content sharing.

Still, the ability of a tablet to support email, social networking and Internet apps does show how much traditional PC application value has shifted to content consumption and "light" text communications.

“Consumers will now look at a task that they have to perform, and they will determine which device will allow them to perform such a task in the most effective, fun and convenient way," says Atwal. "The device has to meet the user needs not the other way round.”

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

For "Real Time" Help, People Use Smart Phones

Some 70 percent of all mobile phone owners and 86 percent of smart phone owners have used their phones in the previous 30 days to perform at least one form of real-time activity, according to Pew Internet & American Life Project.

Some 65 percent of smart phone owners say they have used their devices to get turn-by-turn navigation or directions while driving. About 15 percent report doing so on a typical day.

Some 41 percent of mobile phone owners have used their devices to coordinate a meeting or get-together.

About 35 percent they have used their phones to solve an unexpected problem that they or someone else had encountered.

As you might expect, 30 percent used their devices to decide whether to visit a business, such as a restaurant. Some 27 percent have used their phone to find information to help settle an argument.

About 23 percent have used their phone to look up a score of a sporting event, while 20 percent looked for traffic or public transit information.

In addition, 19 percent used their mobiles to get help in an emergency situation.

Overall, these “just-in-time” mobile users amount to 62 percent of the entire U.S. adult population.

Some 65 percent of smart phone owners say they have used their devices to get turn-by-turn navigation or directions while driving. About 15 percent report doing so on a typical day.

Some 41 percent of mobile phone owners have used their devices to coordinate a meeting or get-together.

About 35 percent they have used their phones to solve an unexpected problem that they or someone else had encountered.

As you might expect, 30 percent used their devices to decide whether to visit a business, such as a restaurant. Some 27 percent have used their phone to find information to help settle an argument.

About 23 percent have used their phone to look up a score of a sporting event, while 20 percent looked for traffic or public transit information.

In addition, 19 percent used their mobiles to get help in an emergency situation.

Overall, these “just-in-time” mobile users amount to 62 percent of the entire U.S. adult population.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Despite "Showrooming," Retailers Move to Support Tablet, Smart Phone Apps

Despite the danger of showrooming, where shoppers investigate merchandise in a store, then check prices and buy online, major retailers seem to be embracing mobile shopping as shoppers show growing mobile shopping behavior.

The most popular shopping activity, performed by 57 percent of shoppers, is looking up store information, another study suggests. Half of shoppers compare prices on their mobile

devices, while 39 percent read product descriptions and 38 percent made a purchase, according to a study by Kantar Media and Compete.

Other popular shopping activities include searching for coupons, checking to see if a product is available in store, and checking the status of an existing order, Compete and Kantar Media say.

Up to this point, mobile shopping has been largely a matter of content purchases, though more respondents say they have bought “electronics” than “books.”

Among those who have made a purchase on a mobile device, 40 percent have bought movies, music, and videos, 31 percent have purchased electronics and 26 percent have bought books. Home items, such as furniture, kitchenware, and garden supplies are the least popular items to buy.

Some 68 percent of the retailers have developed smartphone apps and 59 percent

have smart phone-specific sites.

But retailers have their own reasons for embracing mobile inside their stores. From a retailer perspective, mobile point of sale is of high interest in the retailer, hospitality and field service verticals. Some 66 percent of retail, hospitality and field service managers surveyed on behalf of Motorola Solutions are interested in mobile point of sale solutions, while 42 percent of retail respondents are currently piloting or starting trials within the next 36 months.

A majority of respondents are focused on using mobile POS for sales associates on the store floor or to speed buyer check out, the study found.

Retailers also are embracing mobile POS pilots and trials to eliminate the high cost of traditional cash registers and accept customer payments wherever and whenever needed. Some 55 percent of those surveyed even plan to incorporate the ability to take cash as part of their mobile POS operations.

In retail settings, there is more emphasis on “coverage on the showroom floor,” check out and loyalty programs. And despite the emphasis on use of mobile devices as payment terminals, support for cash, checks and credit cards and debit cards are far more important modes of payment. Just nine percent plan to support contactless payment.

Fully 82 percent plan to support credit card payment, while 55 percent plan to take debit cards. Some 45 percent plan to support cash payments, while 36 percent plan to support payment by check. About 16 percent say they plan to support PayPal or some other online payment service.

Respondents suggest that 48 percent of cashiers and point-of-sale staff will be using mobile POS. In 53 percent of cases, the intention is to use fixed POS or self-checkout terminals for actual payment. In about 40 percent of instances, payments are expected to be processed by associates using mobile POS. In about 23 percent of cases, the shopper’s smart phone will be the payment terminal.

Some 47 percent of other sales associates will be outfitted with mobile POS. About 37 percent of customer service personnel will have mobile POS capabilities.

Also, a third of “store clerks” and 31 percent of field sales professionals will be using mobile POS. For retailers, 71 percent see “better customer service” as a tactical goal.

HawkPartners, a Boston-based marketing consulting and research firm, reviewed the mobile and tablet offerings of the top 100 US retailers and found that less than one-third of retailers have optimized, or even adjusted, their sites for tablets.

Rather than investing in separate iPad sites (or iPad apps), most simply use their existing websites, which translates into a clunky and often frustrating shopping experience for

consumers.

While over two-thirds of the retailers have iPhone apps, only half offer the ability to purchase using the app, the study suggests.

The most popular shopping activity, performed by 57 percent of shoppers, is looking up store information, another study suggests. Half of shoppers compare prices on their mobile

devices, while 39 percent read product descriptions and 38 percent made a purchase, according to a study by Kantar Media and Compete.

Other popular shopping activities include searching for coupons, checking to see if a product is available in store, and checking the status of an existing order, Compete and Kantar Media say.

Up to this point, mobile shopping has been largely a matter of content purchases, though more respondents say they have bought “electronics” than “books.”

Among those who have made a purchase on a mobile device, 40 percent have bought movies, music, and videos, 31 percent have purchased electronics and 26 percent have bought books. Home items, such as furniture, kitchenware, and garden supplies are the least popular items to buy.

Some 68 percent of the retailers have developed smartphone apps and 59 percent

have smart phone-specific sites.

But retailers have their own reasons for embracing mobile inside their stores. From a retailer perspective, mobile point of sale is of high interest in the retailer, hospitality and field service verticals. Some 66 percent of retail, hospitality and field service managers surveyed on behalf of Motorola Solutions are interested in mobile point of sale solutions, while 42 percent of retail respondents are currently piloting or starting trials within the next 36 months.

A majority of respondents are focused on using mobile POS for sales associates on the store floor or to speed buyer check out, the study found.

Retailers also are embracing mobile POS pilots and trials to eliminate the high cost of traditional cash registers and accept customer payments wherever and whenever needed. Some 55 percent of those surveyed even plan to incorporate the ability to take cash as part of their mobile POS operations.

Fully 71 percent of respondents that indicated interest in mobile POS are using or planning to use it to improve customer service and also intend to provide access to inventory management (51 percent), pricing (48 percent) and merchandise returns (42 percent) applications.

In December 2011, Motorola's holiday shopper survey also found that a third of store visits ended with an average of $125 unspent due to missed opportunities to purchase. The survey also found that inefficient payment processes were one of the leading contributors to those lost sales. In that survey, more than 43 percent of shoppers agreed that their shopping experience improved when store associates used mobile POS devices.

About 16 percent of surveyed retailers currently have a mobile POS solution deployed, while less than nine percent have completely mobile or portable checkout systems.

On average, retail respondents anticipated replacing more than 36 percent of their fixed POS as a result of migrating to an mobile POS.

About 41 percent of field service respondents intend to use mobile POS for taking orders and selling in the field. About 39 percent plan to support banking transactions. But a third also see “management of the business” applications and 24 percent will automate work orders.

In retail settings, there is more emphasis on “coverage on the showroom floor,” check out and loyalty programs. And despite the emphasis on use of mobile devices as payment terminals, support for cash, checks and credit cards and debit cards are far more important modes of payment. Just nine percent plan to support contactless payment.

Fully 82 percent plan to support credit card payment, while 55 percent plan to take debit cards. Some 45 percent plan to support cash payments, while 36 percent plan to support payment by check. About 16 percent say they plan to support PayPal or some other online payment service.

Respondents suggest that 48 percent of cashiers and point-of-sale staff will be using mobile POS. In 53 percent of cases, the intention is to use fixed POS or self-checkout terminals for actual payment. In about 40 percent of instances, payments are expected to be processed by associates using mobile POS. In about 23 percent of cases, the shopper’s smart phone will be the payment terminal.

Some 47 percent of other sales associates will be outfitted with mobile POS. About 37 percent of customer service personnel will have mobile POS capabilities.

Also, a third of “store clerks” and 31 percent of field sales professionals will be using mobile POS. For retailers, 71 percent see “better customer service” as a tactical goal.

HawkPartners, a Boston-based marketing consulting and research firm, reviewed the mobile and tablet offerings of the top 100 US retailers and found that less than one-third of retailers have optimized, or even adjusted, their sites for tablets.

Rather than investing in separate iPad sites (or iPad apps), most simply use their existing websites, which translates into a clunky and often frustrating shopping experience for

consumers.

While over two-thirds of the retailers have iPhone apps, only half offer the ability to purchase using the app, the study suggests.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, May 7, 2012

MasterCard Launches Own Mobile Wallet

MasterCard is launching its own digital wallet service, initially focusing on services for online shopping on websites, but ultimately as a mobile wallet as well. It would be tempting to say either that MasterCard has lost confidence in its partnership with Google Wallet, or that MasterCard needs to ensure it can match the rival V.e mobile wallet effort.

The latter is more likely correct than the former. At the moment, both Visa and MasterCard are pursuing multiple parallel efforts, in large part because nobody can be entirely sure which approaches will win in the market. Neither MasterCard nor Visa want to be caught unawares, so it just makes sense to invest in a number of rival approaches.

In addition to V.me and "PayPass" by MasterCard, Isis and other consortia of European mobile service providers also are launching their own mobile wallets. Google Wallet and PayPal also are committed to their own branded wallets as well.

PayPass Wallet Services, a suite of software products for use by merchants, card-issuing banks and their customers will be used initially by AMR Corp.'s American Airlines and Barnes & Noble on their respective websites. American Airlines will also integrate the technology into its mobile application.

The latter is more likely correct than the former. At the moment, both Visa and MasterCard are pursuing multiple parallel efforts, in large part because nobody can be entirely sure which approaches will win in the market. Neither MasterCard nor Visa want to be caught unawares, so it just makes sense to invest in a number of rival approaches.

In addition to V.me and "PayPass" by MasterCard, Isis and other consortia of European mobile service providers also are launching their own mobile wallets. Google Wallet and PayPal also are committed to their own branded wallets as well.

PayPass Wallet Services, a suite of software products for use by merchants, card-issuing banks and their customers will be used initially by AMR Corp.'s American Airlines and Barnes & Noble on their respective websites. American Airlines will also integrate the technology into its mobile application.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Evolution of the "Screen"

The functions embedded into "screens" have changed dramatically over the last three decades. In the past, the TV was a moderately dumb device, while the component TV monitor intentionally was a dumb device.

The functions embedded into "screens" have changed dramatically over the last three decades. In the past, the TV was a moderately dumb device, while the component TV monitor intentionally was a dumb device. With the introduction of smart phones, iPods, game players, tablets and notebooks, most screens are part of "intellligent" devices that make quite a few specific assumptions about the networks and types of software those devices will be interworking with and supporting.

With the exception of the desktop PC monitor, virtually all other screens intentionally assume roles as "intelligent" devices, with specific networks and application environments in mind.

These days most TVs remain moderately intelligent screens that still require some third party devices to add more functionality. For cable, satellite and telco TV, that device is the set-top decoder. In other cases it is the game console or an "Apple TV" box that provides the additional functionality.

The big issue now is how fast, and how far, the third party functionality can be built into the standard TV. Up to this point, it has proven quite difficult to do so, and that likely will not change, even as rumored Apple TVs and Google TVs are created for the mass market.

The point is that many of the advanced features still require highly network-specific software loads that cannot all be supported in a basic TV display.

That is important because advanced features that can be "built in" to a smart phone or tablet will be more difficult in a TV monitor.

Each smart phone is built with detailed knowledge of the networks it must interoperate with.

Many third party devices, such as game consoles, simply cannot make those assumptions and must be insulated from network details, with the exception of simple network interfaces, such as Wi-Fi and Internet.

The big question for any new suppliers that want to change the experience of TV viewing is to determine which important new features can be embedded, at what cost. In most cases, a relatively "dumb" approach still will make sense for general purpose screens that are expected to work with "all" game consoles, service provider decoders, VCRs, DVD players and video recorder devices.

Though service providers long have wanted an ability to offload the decoder functions to the TV, that has proven impractical. In most cases, especially when software continues to evolve rapidly, it will make sense to provide standard network interfaces to popular third party devices, Internet and Wi-Fi connections, while restricting on-board applications and features that typically are provided by a third party device.

Many would argue TVs always will have to be relatively dumb displays, compared to other screens, because those other screens are designed to be used primarily within one platform, or on one network. But nobody wants to get a new TV every time they change video service providers, game consoles or other devices that normally get attached to TVs.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Smart Phones A Majority of Phones in Use for First Time

It's an important milestone: In March 2012, a majority (50.4 percent) of U.S. mobile subscribers owned smart phones, up from 47.8 percent in December 2011. Smart phones have been outselling feature phones for some time, but this appears to be the first time the installed base has featured a majority of smart phone users.

In the first quarter of 2012, for example, smart phones represented 66 percent of all handset sales, according to NPD.

Consumers purchasing new phones picked smart phones more often, and among smart phone owners Apple was the top manufacturer of smart phone handsets, while Android was the top smart phone OS, says Nielsen.

In an interesting note, the Nielsen data also shows the importance of smart phones for minority populations, all of whom use smart phones at higher rates than "white" Americans. The reason that is significant is that it is possible mobile broadband is a "more important" method of access for some groups, compared to others. Discussions of "broadband gaps" have to take that into account.

The point is that "differences" in consumer choice are not necessarily indicative of "supply gaps."

In the first quarter of 2012, for example, smart phones represented 66 percent of all handset sales, according to NPD.

Consumers purchasing new phones picked smart phones more often, and among smart phone owners Apple was the top manufacturer of smart phone handsets, while Android was the top smart phone OS, says Nielsen.

In an interesting note, the Nielsen data also shows the importance of smart phones for minority populations, all of whom use smart phones at higher rates than "white" Americans. The reason that is significant is that it is possible mobile broadband is a "more important" method of access for some groups, compared to others. Discussions of "broadband gaps" have to take that into account.

The point is that "differences" in consumer choice are not necessarily indicative of "supply gaps."

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Why Most Mobile Innovations Fail, and Will Fail

Amazon probably has quite-different reasons for embracing tablets than many magazine and newspaper publishers do, and the reasons illustrate the difficulty of adapting offline business models to mobile modes.

One rule of thumb used by venture capital investors when assessing technology firms is to look for an order of magnitude better user experience. That rule sometimes is expressed as an order of magnitude better technology performance.

Using that measuring stick, one might argue that, whatever the initial expectations, magazine and newspaper experiences with mobile apps for smart phones and tablets have delivered “end user experience” that is problematic, compared to Amazon’s experience with books.

At the same time, from a provider perspective, mobile apps that were expected to recast newspaper and magazine readership and revenue have proven more complicated than offline publishing, have cost more than expected and provide less profit than expected.

Amazon, on the other hand, arguably has focused on selling digital content with characteristics that are more congruent with the offline end user experience, at costs more controllable and predictable.

While one might argue that tablet and smart phone content availability is not an order of magnitude more valuable to end users than offline versions of those products, one might well argue that the digital versions of songs, videos and books that Amazon sells provide more value than the digital subscriptions magazines and newspapers have tried to sell.

Also, in terms of the “native app versus Web” delivery formats, some content products are better suited, or equally well suited, to Web distribution, compared to app distribution.

Some of the same fundamental questions must be asked of other new mobile businesses that take offline processes, such as shopping, paying and banking, and attempt to create new mobile versions of those products.

Mass adoption will hinge on whether end users perceive dramatically-better experiences, whether we can quantify how much better those experiences are. The notion of “dramatically better” is akin to “order of magnitude” change that can induce massive end user behavior change, while the “incrementally better” notion, with incremental new hassle, is not likely to lead to behavior change.

Looking only at magazine and newspaper apps, there are issues that illustrate the hurdles. Apple’s 30-percent slice of gross revenue is a problem for suppliers, since that is higher than the typical profit margin for a newspaper or magazine publisher. Irrespective of end user experience, it arguably is a “profitless” exercise to sell a digital magazine or newspaper subscription when the revenue split gives a distributor 30 percent of gross revenue.

Among other complications, though, were how publishers could comply with their normal auditing standards used for offline publications, Technology Review notes.

Nor, oddly enough, did mobile apps represent a particularly easy publishing format. Tablets, and some smart phones, support both a "portrait" (vertical) and "landscape" (horizontal) view, depending on how the user held the device.

Then, too, the screens of smart phones were much smaller than those of tablets.

So many publishers ended up producing six different versions of their editorial product: a print publication, a conventional digital replica for Web browsers and proprietary software, a digital replica for landscape viewing on tablets, something that was not quite a digital replica for portrait viewing on tablets, a kind of hack for smart phones, and ordinary HTML pages for their websites.

Not surprisingly, app development costs were unexpected.

But the real problem, some might argue, is that end users expect an online “link rich” experience when using an app for content consumption, much as they expect with Web-based content consumption.

That conflicts with the walled garden that a newspaper or magazine represents. In one sense, a magazine or newspaper is like a compact disc, a collection of items, whereas people increasingly expect to consume items one at a time, in random fashion.

Fundamentally, people consuming in an online channel are looking for songs, not albums. They are looking for stories, not collections.

The point is that transitioning from offline products to mobile products sometimes is not just a matter of authoring, design and software development. Sometimes the product has to be different when it is a mobile-consumed product, not an offline product.

There are many analogies. A mobile payment capability, for example, has to offer an experience that is qualitatively and significantly better than paying with cash or a credit card. It can’t be a little better. It has to be a lot better. And that means it cannot be new experience that is just seconds faster.

There has to be something about the experience that is much better. Maybe a user won’t be able to quantify the changes so easily. But they have to sense that the “new thing” is really lots better than the “old thing.” Slight little improvements won’t motivate change.

You might argue that Square, and other merchant point of sale services offered by Intuit and PayPal have gotten such big traction because they were those sorts of “vastly better” experiences, allowing small retailers to take credit card and debit card payments where they never could do so before.

Something like that will happen for every successful mobile app and use case, period. But most apps and experiences do not represent that sort of clear advantage for end users. Tablets and smart phones, on the other hand, clearly have succeeded in offering user experience and value much better than users had before.

Without such value, new revenue models and businesses will not succeed in the mobile realm.

One rule of thumb used by venture capital investors when assessing technology firms is to look for an order of magnitude better user experience. That rule sometimes is expressed as an order of magnitude better technology performance.

Using that measuring stick, one might argue that, whatever the initial expectations, magazine and newspaper experiences with mobile apps for smart phones and tablets have delivered “end user experience” that is problematic, compared to Amazon’s experience with books.

At the same time, from a provider perspective, mobile apps that were expected to recast newspaper and magazine readership and revenue have proven more complicated than offline publishing, have cost more than expected and provide less profit than expected.

Amazon, on the other hand, arguably has focused on selling digital content with characteristics that are more congruent with the offline end user experience, at costs more controllable and predictable.

While one might argue that tablet and smart phone content availability is not an order of magnitude more valuable to end users than offline versions of those products, one might well argue that the digital versions of songs, videos and books that Amazon sells provide more value than the digital subscriptions magazines and newspapers have tried to sell.

Also, in terms of the “native app versus Web” delivery formats, some content products are better suited, or equally well suited, to Web distribution, compared to app distribution.

Some of the same fundamental questions must be asked of other new mobile businesses that take offline processes, such as shopping, paying and banking, and attempt to create new mobile versions of those products.

Mass adoption will hinge on whether end users perceive dramatically-better experiences, whether we can quantify how much better those experiences are. The notion of “dramatically better” is akin to “order of magnitude” change that can induce massive end user behavior change, while the “incrementally better” notion, with incremental new hassle, is not likely to lead to behavior change.

Looking only at magazine and newspaper apps, there are issues that illustrate the hurdles. Apple’s 30-percent slice of gross revenue is a problem for suppliers, since that is higher than the typical profit margin for a newspaper or magazine publisher. Irrespective of end user experience, it arguably is a “profitless” exercise to sell a digital magazine or newspaper subscription when the revenue split gives a distributor 30 percent of gross revenue.

Among other complications, though, were how publishers could comply with their normal auditing standards used for offline publications, Technology Review notes.

Nor, oddly enough, did mobile apps represent a particularly easy publishing format. Tablets, and some smart phones, support both a "portrait" (vertical) and "landscape" (horizontal) view, depending on how the user held the device.

Then, too, the screens of smart phones were much smaller than those of tablets.

So many publishers ended up producing six different versions of their editorial product: a print publication, a conventional digital replica for Web browsers and proprietary software, a digital replica for landscape viewing on tablets, something that was not quite a digital replica for portrait viewing on tablets, a kind of hack for smart phones, and ordinary HTML pages for their websites.

Not surprisingly, app development costs were unexpected.

But the real problem, some might argue, is that end users expect an online “link rich” experience when using an app for content consumption, much as they expect with Web-based content consumption.

That conflicts with the walled garden that a newspaper or magazine represents. In one sense, a magazine or newspaper is like a compact disc, a collection of items, whereas people increasingly expect to consume items one at a time, in random fashion.

Fundamentally, people consuming in an online channel are looking for songs, not albums. They are looking for stories, not collections.

The point is that transitioning from offline products to mobile products sometimes is not just a matter of authoring, design and software development. Sometimes the product has to be different when it is a mobile-consumed product, not an offline product.

There are many analogies. A mobile payment capability, for example, has to offer an experience that is qualitatively and significantly better than paying with cash or a credit card. It can’t be a little better. It has to be a lot better. And that means it cannot be new experience that is just seconds faster.

There has to be something about the experience that is much better. Maybe a user won’t be able to quantify the changes so easily. But they have to sense that the “new thing” is really lots better than the “old thing.” Slight little improvements won’t motivate change.

You might argue that Square, and other merchant point of sale services offered by Intuit and PayPal have gotten such big traction because they were those sorts of “vastly better” experiences, allowing small retailers to take credit card and debit card payments where they never could do so before.

Something like that will happen for every successful mobile app and use case, period. But most apps and experiences do not represent that sort of clear advantage for end users. Tablets and smart phones, on the other hand, clearly have succeeded in offering user experience and value much better than users had before.

Without such value, new revenue models and businesses will not succeed in the mobile realm.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tablets are "Entertainment" Devices With a High "Status" Value

Tablets primarily are used for entertainment and are a status symbol, not devices used for "work" and productivity, Alcatel-Lucent says.

Tablets primarily are used for entertainment and are a status symbol, not devices used for "work" and productivity, Alcatel-Lucent says. Though becoming a standard feature of "work" environments, tablets are used primarily for game play, content activities such as reading and viewing streaming and stored videos, Alcatel-Lucent says.

Key benefits are screen quality, flexible connectivity, battery life and slim form factor, all of which contribute to the device’s ease of use and portability. The study also suggests that use of various computing devices varies with screen size. The smart phone is the universal screen, while tablets are used in lean back environments.

Smart phones are the primary mobility devices, and tablets substitute for laptops when the primary goal is relaxation or entertainment.

Tablets are "rarely" used for productive work because they lack keyboards and mice for efficient and effective data input and control of the device, the study suggests.

Also, respondents in Spain and the United States own tablets as a badge of social status. Some might not think such rationales are key drivers of behavior, but one only has to look back a decade or so, when use of a BlackBerry device similarly was seen as a sign of status or importance in enterprise settings.

The "pain of adoption" (cost) in this case is overwhelmed to a great extent by the value of the status. As equity analyst Pip Coburn has noted, all technology products achieve adoption only when the pain of the status quo is greater than that pain of adoption. And "pain" can be a matter of social status or inclusion.

Mass adoption of any new technology becomes irresistible when "all my friends have an X."

Arguments about tablet productivity are to be expected in business settings. Users will not be able to justify buying them, otherwise.

But it is safe to say many of those arguments are spurious.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

U.S. Mobile Providers Face Spectrum Uncertainty

U.S. wireless operators and equity analysts have argued for well over a decade that there is "too much competition" in the U.S. mobile market. The notion is that a stable national market would have no more than three providers.

Also, with the emergence of the smart phone business, all mobile service providers need lots more spectrum, though some would contest the notion in a near-term sense.

But some also note that, at least for the moment, contestants are stymied, in large part because recent deals that would have changed spectrum allocations, and some deals still pending, signal to most contestants the likely regulatory resistance.

Recent regulatory action includes the successful regulator resistance to the AT&T purchase of T-Mobile USA, and scrutiny of the spectrum sales by Comcast, Time Warner Telecom, Cox Communications and Bright House Networks to Verizon.

The denial of LightSquared to use satellite spectrum for a terrestrial Long Term Evolution network is a separate case, many would argue, as the issue there was not market structure (indeed, one might have argued LightSquared would increase the level of competition in the U.S. market), but signal interference with other licensed users.

Is the share of market now characteristic of the U.S. market sustainable? Most would say "no." Among the common observations is that two of the top four national providers have market share two to three times greater than two of the others.

Also, with the emergence of the smart phone business, all mobile service providers need lots more spectrum, though some would contest the notion in a near-term sense.

But some also note that, at least for the moment, contestants are stymied, in large part because recent deals that would have changed spectrum allocations, and some deals still pending, signal to most contestants the likely regulatory resistance.

Recent regulatory action includes the successful regulator resistance to the AT&T purchase of T-Mobile USA, and scrutiny of the spectrum sales by Comcast, Time Warner Telecom, Cox Communications and Bright House Networks to Verizon.

The denial of LightSquared to use satellite spectrum for a terrestrial Long Term Evolution network is a separate case, many would argue, as the issue there was not market structure (indeed, one might have argued LightSquared would increase the level of competition in the U.S. market), but signal interference with other licensed users.

Is the share of market now characteristic of the U.S. market sustainable? Most would say "no." Among the common observations is that two of the top four national providers have market share two to three times greater than two of the others.

Many observers would say a market with four national providers is about one too many for a sustainable and stable market. Significantly, that view is held by the Federal Communications Commission and Department of Justice, both of which use a standard test of market concentration in deeming the U.S. mobile market already

One of the ways to measure market concentration is the Heffindahl-Hirshman Index or HHI, often used as a measure of market concentration. The HHI is the square of the percentage market share of each firm summed over the largest 50 firms in a market.

The HHI which already suggests that the market is uncompetitive. HHI is the problem where it comes to further mergers among the four largest national mobile providers, even a merger of Sprint and T-Mobile USA, which despite its complexity would create three national providers with roughly equivalent market share.

Market share concerns also will permeate any spectrum acquisitions, as well, since spectrum is a key "raw material" from which any mobile service provider can build a business.

Over the long term, there is perhaps general agreement that more spectrum will be required. At issue is the way such spectrum is allocated. In the past, many regulators, in many countries, have restricted availability of new spectrum by incumbents, hoping thereby to create more competition.

Over the long term, one has to question whether this actually ever works, as all markets, over time, consolidate, even when the initial implications would appear to be positive, from an "enabling of competition" perspective.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Cloud Winners and Losers Will Cross Ecosystems

Who wins, and who loses, as mobile apps and services, especially cloud-based apps and services, gain more traction? The “obvious” answer is that device and app providers are “winning,” while service providers “lose.” Though obviously true in the case of over-the-top voice, messaging, videoconferencing and entertainment video realms, the larger reality is more complicated.

In many cases substantial and real competition now is occurring between firms in different ecosystems, not only within single ecosystems. And, as has been the case for a couple of decades, contestants have to balance effort between protecting existing businesses and growing new lines of business.

The difference now is that many of the new revenue streams and businesses actually cross ecosystems and redefine them.

For example, mobile payment systems offered by Square, Intuit and PayPal arguably represent incremental revenue within the credit card and debit card transaction business, rather than primarily a shift of transaction volume within the business. The reason is that such services are used primarily by businesses that would not have used merchant point of sale systems in the past.

Likewise, to some extent, services that turn smart phones and tablets into merchant point of sale systems will compete with supplier of traditional merchant terminals, as well.

Enterprise cloud services might compete with packaged software suppliers, data centers or server manufacturers, for example. That would mean some amount of competition between segments of one industry.

Small business cloud services might reduce the amount of revenue earned by value-added resellers or system integrators, for example. That also is a form of intra-ecosystem competition.

Consumer cloud services, especially those related to storage, will displace some of the need for local storage, and could reduce demand for external hard drive storage and some amount of PC sales. That might be more an example of competition between ecosystems

Cloud storage might reduce need for PCs and storage devices, for example, reducing some amount of device spending and shifting that spending into software and services. So some device manufacturers might lose, while others might gain (PCs, external storage lose; mobile devices win).

By the end of 2013, consumer cloud services for accessing content will be integrated into 90 percent of all connected consumer devices, according to Gartner.

The other dynamic is that, in the case of brand-new services, such as cloud storage, there could also be winners within and between ecosystems. App providers could win, as well as hosting facilities.

Traditional entertainment video suppliers such as cable companies hope to win, even as some amount of entertainment video shifts to cloud mechanisms, even as rivals think cloud delivery will eventually displace traditional distribution mechanisms.

Likewise, cloud services could help device manufacturers as much as app providers. Certain handsets and environments, such as iOS iTunes and Apple tablets and phones, or Google Drive and Android-based devices, provide early examples. That might be an example of value and revenue shifts within the mobile ecosystem.

In other cases, such as many parts of the mobile commerce business, competition might entail substantial amounts of competition between ecosystems. Services offered by the likes of Square, Intuit and PayPal that turn a smart phone into a merchant point of service terminal represent competition between those firms and other existing payment systems, merchant POS terminal providers and emerging application provider or mobile communications service provider payment systems.

“Inside the spending envelope, market dynamics will collapse some markets while creating others that expand the captured revenue,” says Gartner managing vice president Andrew Johnson.

Providers of consumer devices, services and content must anticipate the risk of sweeping changes to their business models,” said Johnson. “The personal cloud will force technology providers not only to rethink how they approach markets, but also, more importantly, how they define markets.”

Emerging and mature markets are no longer useful form of market segmentation, Johnson argues.

In many cases substantial and real competition now is occurring between firms in different ecosystems, not only within single ecosystems. And, as has been the case for a couple of decades, contestants have to balance effort between protecting existing businesses and growing new lines of business.

The difference now is that many of the new revenue streams and businesses actually cross ecosystems and redefine them.

For example, mobile payment systems offered by Square, Intuit and PayPal arguably represent incremental revenue within the credit card and debit card transaction business, rather than primarily a shift of transaction volume within the business. The reason is that such services are used primarily by businesses that would not have used merchant point of sale systems in the past.

Likewise, to some extent, services that turn smart phones and tablets into merchant point of sale systems will compete with supplier of traditional merchant terminals, as well.

Enterprise cloud services might compete with packaged software suppliers, data centers or server manufacturers, for example. That would mean some amount of competition between segments of one industry.

Small business cloud services might reduce the amount of revenue earned by value-added resellers or system integrators, for example. That also is a form of intra-ecosystem competition.

Consumer cloud services, especially those related to storage, will displace some of the need for local storage, and could reduce demand for external hard drive storage and some amount of PC sales. That might be more an example of competition between ecosystems

Cloud storage might reduce need for PCs and storage devices, for example, reducing some amount of device spending and shifting that spending into software and services. So some device manufacturers might lose, while others might gain (PCs, external storage lose; mobile devices win).

By the end of 2013, consumer cloud services for accessing content will be integrated into 90 percent of all connected consumer devices, according to Gartner.

The other dynamic is that, in the case of brand-new services, such as cloud storage, there could also be winners within and between ecosystems. App providers could win, as well as hosting facilities.

Traditional entertainment video suppliers such as cable companies hope to win, even as some amount of entertainment video shifts to cloud mechanisms, even as rivals think cloud delivery will eventually displace traditional distribution mechanisms.

Likewise, cloud services could help device manufacturers as much as app providers. Certain handsets and environments, such as iOS iTunes and Apple tablets and phones, or Google Drive and Android-based devices, provide early examples. That might be an example of value and revenue shifts within the mobile ecosystem.

In other cases, such as many parts of the mobile commerce business, competition might entail substantial amounts of competition between ecosystems. Services offered by the likes of Square, Intuit and PayPal that turn a smart phone into a merchant point of service terminal represent competition between those firms and other existing payment systems, merchant POS terminal providers and emerging application provider or mobile communications service provider payment systems.

“Inside the spending envelope, market dynamics will collapse some markets while creating others that expand the captured revenue,” says Gartner managing vice president Andrew Johnson.

Providers of consumer devices, services and content must anticipate the risk of sweeping changes to their business models,” said Johnson. “The personal cloud will force technology providers not only to rethink how they approach markets, but also, more importantly, how they define markets.”

Emerging and mature markets are no longer useful form of market segmentation, Johnson argues.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sunday, May 6, 2012

Online Video Still Needs Scale to Attract More Advertising

The online-video market represented about $1.8 billion worth of ad spending in 2011, with half of that going to just two players: Hulu (about $300 million) and YouTube (about $600 million), according to Brian Wieser, an analyst at Pivotal Research Group, and reported by Ad Age.

The online-video market represented about $1.8 billion worth of ad spending in 2011, with half of that going to just two players: Hulu (about $300 million) and YouTube (about $600 million), according to Brian Wieser, an analyst at Pivotal Research Group, and reported by Ad Age. Most of the advertising growth in online video could happen because it shifts spending from the $70 billion spent annually on TV ads in the U.S. market.

High-quality video lots of people want to watch might be necessary. But it is not sufficient for success, simply because video advertisers want large audiences.

And the simple fact is that not many providers have both attractive programming and large audiences. Subscription revenue is dominated by Netflix.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, May 4, 2012

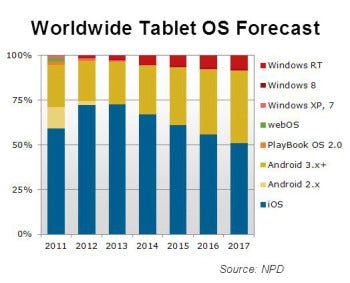

Apple Tablet Share 51% in 2017

Apple, after reaching a market share high of nearly 75 percent in 2013, will see its share decline steadily to 50.9 percent in 2017, according to forecasts by the NPD Group.

Apple, after reaching a market share high of nearly 75 percent in 2013, will see its share decline steadily to 50.9 percent in 2017, according to forecasts by the NPD Group.Shipments of tablet PCs are expected to grow from 81.6 million units in 2011 to 424.9 million units by 2017, according to NPD Group.

That forecast suggests that in 2016 more tablet PCs will be shipped than notebook PCs.

The iOS operating system has been dominant in tablet PCs, but it is expected to lose share, from 72.1 percent in 2012 to 50.9 percent in 2017, as Android increases from 22.5 percent in 2012 to 40.5 percent over the same period.

Meanwhile, share for Windows RT is also expected to grow, but from a very small base of 1.5 percent in 2012 to 7.5 percent in 2017.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

AI Model Pricing Eventually Moves to a Cloud Model

So far, language model pricing based on usage closely mirrors the early patterns of cloud computing , . Which matured into a massive, lower-...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Financial analysts typically express concern when any firm’s customer base is too concentrated. Consider that, In 2024, CoreWeave’s top two ...