The European Union wants its leading fixed network service providers to connect 50 percent of region households to high-speed broadband by 2020, using fiber to the home technology.

By "high speed," the EU means internet speeds of 30 Mbps or above for European citizens, with half European households subscribing to connections of 100Mbps or higher.

As always, the issue is how to get from here to there. Europe also features high reliance on wholesale access to existing copper access infrastructure, at prices competitors naturally want to keep low, and if possible, decrease.

Service providers who will be borrowing the money to invest obviously think that is detrimental to the business case for new fiber.

France Telecom expects a payback payback time of 30 years to 40 years, far exceeding the three-year to five-year payback expected of application investments.

A business plan with a payback of five years or less has to assume retail penetration of at least 30 percent, and ih many cases also with triple-play service offerings. Any payback analysis is of course highly dependent on the assumptions, ranging from capital cost per location passed, as well as service revenue per location, among other things

That indicates the risk France Telecom and other providers are facing. Those time frames are so long they typically only can be considered by very capital intensive utility firms that operate in monopoly style markets, as fixed network providers used to assume was the case.

These days, the fixed network business faces competition from other facilities-based suppliers, mobile and satellite networks.

Tuesday, June 12, 2012

Fiber to the Home Still is About Difficult Investment Conditions

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

"Share Everything" Plan Should You Buy?

As always is the case when mobile retail service plans are revamped in major ways, each account owner, and customers of other service providers, will have to do a bit of work to figure out whether the new plans are better than the existing plans any user is buying.

As always, the answer is that whether the new plans are better, roughly the same, or worse, for any given customer depends on how users on any account want to use mobile services.

For some Verizon customers who don’t use all their voice minutes and text allowance, the new plans, featuring unlimited domestic calling and texting, might not actually offer any new value, except theoretically. Such users might even pay slightly more.

Heavy voice or texting users might like the plans, and might save a bit of money.

Heavy data users might pay measurably more, but also can buy plans that match their usage.

If shared data plans have similar market impact to family voice and texting plans, the decision context will change. The big decisions will not be "choosing a new plan" for the same services and devices, but "adding new devices to the account" and "upgrading feature phones to smart phones." Those decisions, it is true, will increase recurring bills, but mainly because adding incremental new devices costs less than it would have in the past.

In all likelihood, that was part of Verizon Wireless thinking all along. To the extent possible, the new plans would aim to be revenue neutral for customers who do not plan to change the number of devices on any single account, or upgrade devices from feature phones to smart phones.

For accounts where the incremental costs now are more attractive, the decisions will more likely hinge on whether it now makes sense to spend a little more, to get more.

As always, the answer is that whether the new plans are better, roughly the same, or worse, for any given customer depends on how users on any account want to use mobile services.

For some Verizon customers who don’t use all their voice minutes and text allowance, the new plans, featuring unlimited domestic calling and texting, might not actually offer any new value, except theoretically. Such users might even pay slightly more.

Heavy voice or texting users might like the plans, and might save a bit of money.

Heavy data users might pay measurably more, but also can buy plans that match their usage.

If shared data plans have similar market impact to family voice and texting plans, the decision context will change. The big decisions will not be "choosing a new plan" for the same services and devices, but "adding new devices to the account" and "upgrading feature phones to smart phones." Those decisions, it is true, will increase recurring bills, but mainly because adding incremental new devices costs less than it would have in the past.

In all likelihood, that was part of Verizon Wireless thinking all along. To the extent possible, the new plans would aim to be revenue neutral for customers who do not plan to change the number of devices on any single account, or upgrade devices from feature phones to smart phones.

For accounts where the incremental costs now are more attractive, the decisions will more likely hinge on whether it now makes sense to spend a little more, to get more.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

DirecTV Might Deploy Ad-Skipping Technology

DirecTV says it could deploy technology that would enable its millions of subscribers to automatically skip television advertising, Reuters reports. DirecTV probably wouldn't do anything until lawsuits pitting Dish Network against TV broadcasters, over the legality of such practices, are settled in court.

Fox, CBS and NBCUniversal separately have sued Dish Network over its new AutoHop service, which allows consumers to skip television ads. At the same time, Dish has filed its own lawsuit against all four broadcast networks seeking a declaration as to the legality of its new service.

Dish’s "Hopper" is a digital video recorder that allows Dish customers to automatically skip past all the commercials on some prime-time network TV shows. Understandably, the TV networks aren't too happy about that, even if Dish customers might like the feature, and they have sued Dish Network to stop the practice.

TiVo also had earlier proposed allowing its customers to skip over all commercials, but TiVo disabled the feature after intense opposition from programming networks.

In a sense, Dish is gambling that the "surgical" approach, allowing users to skip virtually all commercials on broadcast network prime-time programs, will please customers more than it irritates the few affected networks.

Hopper would have faced across the board opposition had it proposed eliminating all commercials from all programming, automatically.

Fox, CBS and NBCUniversal separately have sued Dish Network over its new AutoHop service, which allows consumers to skip television ads. At the same time, Dish has filed its own lawsuit against all four broadcast networks seeking a declaration as to the legality of its new service.

Dish’s "Hopper" is a digital video recorder that allows Dish customers to automatically skip past all the commercials on some prime-time network TV shows. Understandably, the TV networks aren't too happy about that, even if Dish customers might like the feature, and they have sued Dish Network to stop the practice.

TiVo also had earlier proposed allowing its customers to skip over all commercials, but TiVo disabled the feature after intense opposition from programming networks.

In a sense, Dish is gambling that the "surgical" approach, allowing users to skip virtually all commercials on broadcast network prime-time programs, will please customers more than it irritates the few affected networks.

Hopper would have faced across the board opposition had it proposed eliminating all commercials from all programming, automatically.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Mobile and Mobile Payment A Top Issue for Parking Industry

Technology-related innovations account for half of the top ten trends in the $30 billion parking industry. The single most important trend in parking today is the technological revolution

that is driving the industry, according to the International Parking Institute.

In fact, three of the top five trends identified in a study focus on technology, including cashless or electronic payment, technologies to improve access control and payment automation, or increased real-time communication of pricing and availability by mobile phone or similar devices.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

NCR Enables ATMs that use Mobile Devices and Barcodes

New software from NCR Corporation will allow consumers to initiate cash withdrawals from their banking accounts on mobile devices and then complete those transactions at an ATM by scanning a 2D barcode.

New software from NCR Corporation will allow consumers to initiate cash withdrawals from their banking accounts on mobile devices and then complete those transactions at an ATM by scanning a 2D barcode.NCR Mobile Cash Withdrawal will make ATM transactions faster and more secure by removing cards and PINs from the process at the ATM. The entire transaction, while the consumer is in front of the ATM, can take less than 10 seconds, according to NCR.

The point is that there are lots of ways to handle the communications function between a mobile device and a transaction terminal. Near field communications is one way, but only one way.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Apple's Passbook Isn't a Wallet, Yet

But Passbook sure looks like a wallet app. Passbook formally aims only to store loyalty, reward or other account information, from retailers that support barcode apps for boarding passes, store cards, and movie tickets, for example.

Of course, you might note that Apple has about 400 million iTunes accounts linked to user credit cards. So everybody recognizes that Apple could become a wallet of its own, with a mobile-enabled payment mechanism, if it chose to do so. For the moment, it seems content to operate a closed loop service for content purchases from its own "stores."

Of course, you might note that Apple has about 400 million iTunes accounts linked to user credit cards. So everybody recognizes that Apple could become a wallet of its own, with a mobile-enabled payment mechanism, if it chose to do so. For the moment, it seems content to operate a closed loop service for content purchases from its own "stores."

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Verizon’s Shared Data Plan is Revenue Neutral for a Single-User Account

New Verizon Wireless shared data plans are designed to encourage uptake of connected tablets and smart phones. The impact on a single-user smart phone account probably will be "revenue neutral" for both Verizon Wireless and any single smart phone account.

New Verizon Wireless shared data plans are designed to encourage uptake of connected tablets and smart phones. The impact on a single-user smart phone account probably will be "revenue neutral" for both Verizon Wireless and any single smart phone account.And that was intentional, obviously. Ideally, Verizon Wireless would find the new plans provide incentives for group accounts to add smart phone and tablet devices, while not cannibalizing the single-user accounts.

Verizon Wireless seems to have done so. If one compares the existing cost of a single smart phone, with a $40 a month plan including 450 anytime minutes, $20 for unlimited texts, and $30 for 2GB of data, plus $30 for 2GB of data on a connected tablet, the person who owns both devices is currently paying $120 per month for the two devices.

With a shared plan that bumps them to unlimited minutes and shares the whole 4GB of data between devices, their monthly total also costs $120 a month.

But the more telling analysis is the cost for a user who does not connect his or her tablet to the Verizon network. Using the same plan as above, that "phone only" user spends $90 a month just for the phone account.

Adding the tablet represents an incremental cost of $10 for the access. Assuming that user upgrades the data plan to about $70 a month (4 Gbytes), Verizon gains an incremental $40 in mobile data spending, for an incremental increase of $50 a month for a single-device smart phone account adding one connected tablet. That's a significant increase in recurring revenue.

If the single smart phone user only wants to upgrade the data bucket to use the personal hotspot feature, the incremental revenue is $40 a month. That is serious money if enough users upgrade.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Verizon Wireless: Biggest Change in Consumer Mobile Pricing in 10 Years

In 2011, about 57 percent of all U.S. mobile subscribers were enrolled in family plans for voice and texting. In a big move, Verizon Wireless has announced "Share Everything Plans" that Verizon Wireless says "will forever change the way customers purchase wireless services." That probably is not hyperbole, even if some U.S. mobile service providers do not yet agree.

Share Everything Plans include unlimited voice minutes, unlimited text, video and picture messaging and a single data allowance for up to 10 Verizon Wireless devices.

In addition, the Mobile Hotspot service on all the devices is included in the Share Everything Plans at no additional charge, Verizon Wireless says.

The Share Everything Plans debut on June 28 and will be available to new, as well as existing, customers who may wish to move to the new plans.

Share Everything Plans include unlimited voice minutes, unlimited text, video and picture messaging and a single data allowance for up to 10 Verizon Wireless devices.

In addition, the Mobile Hotspot service on all the devices is included in the Share Everything Plans at no additional charge, Verizon Wireless says.

The Share Everything Plans debut on June 28 and will be available to new, as well as existing, customers who may wish to move to the new plans.

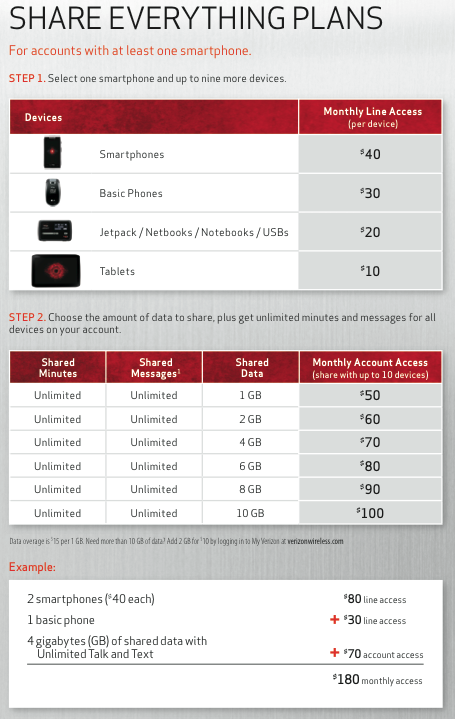

To get started on a Share Everything Plan, customers first select the devices they want on their accounts. That requires a $40 monthly access fee for smart phones.

The next step is to choose a plan that includes unlimited minutes, unlimited messages and a shared data allowance that begins at 1 GB for $50.

Customers adding a tablet on their Share Everything Plans can do so for an additional $10, with no long-term contract requirement. The following matrix shows pricing for an account with several different devices, such as a smartphone, a tablet and a basic phone, billed to the same individual.

The next step is to choose a plan that includes unlimited minutes, unlimited messages and a shared data allowance that begins at 1 GB for $50.

Customers adding a tablet on their Share Everything Plans can do so for an additional $10, with no long-term contract requirement. The following matrix shows pricing for an account with several different devices, such as a smartphone, a tablet and a basic phone, billed to the same individual.

| Step 1 | Step 2 | |||

Monthly Line Access

(per device) | Shared Minutes | Shared Messages | Shared Data | Monthly Account Access (shared with up to 10 devices) |

Smart phones - $40

Basic Phones - $30 Jetpacks/USBs/ Notebooks/Netbooks - $20 Tablets - $10 | Unlimited | Unlimited | 1 GB | $50 |

| Unlimited | Unlimited | 2 GB | $60 | |

| Unlimited | Unlimited | 4 GB | $70 | |

| Unlimited | Unlimited | 6 GB | $80 | |

| Unlimited | Unlimited | 8 GB | $90 | |

| Unlimited | Unlimited | 10 GB | $100 | |

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

67% of Small Businesses Use Tablets

Nearly all small businesses (96 percent) surveyed on behalf of AT&T report they use wireless technologies in their operations, with almost two-thirds (63 percent) indicating that they could not survive — or it would be a major challenge to survive — without wireless technologies.

Nearly all small businesses (96 percent) surveyed on behalf of AT&T report they use wireless technologies in their operations, with almost two-thirds (63 percent) indicating that they could not survive — or it would be a major challenge to survive — without wireless technologies.Some 43 percent of small businesses surveyed report all of their employees use wireless devices or technologies to work away from the office, a nearly 80 percent jump from three years ago.

Perhaps more surprisingly, 67 percent of small businesses surveyed indicate that they use tablet computers, up from 57 percent a year ago. AT&T says.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Video Charging is the Big Issue to be Solved

It is hard to escape the notion that video applications are the key issue for access providers, especially mobile access and service providers. As has been true on the global backbone networks for some time, video is the predominant traffic type.

And since video bandwidth is between one and two orders of magnitude more intense than any other application (voice, for example), the transition to a largely video-driven usage mode has serious implications for access providers.

You don't have to agree with any particular method for cost recovery to note that video really is the preeminent bandwidth problem, going forward. Up to this point, end users have paid the charges. But there are other obvious models. No subscriber to a video entertainment service pays for "bandwidth" in a direct sense.

Consumers pay for access to content, and the bandwidth costs are simply part of the overall cost of creating and delivering the experience. Someday, that principle might have wider application.

And since video bandwidth is between one and two orders of magnitude more intense than any other application (voice, for example), the transition to a largely video-driven usage mode has serious implications for access providers.

You don't have to agree with any particular method for cost recovery to note that video really is the preeminent bandwidth problem, going forward. Up to this point, end users have paid the charges. But there are other obvious models. No subscriber to a video entertainment service pays for "bandwidth" in a direct sense.

Consumers pay for access to content, and the bandwidth costs are simply part of the overall cost of creating and delivering the experience. Someday, that principle might have wider application.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Top European Regulator Calls for Telco Mergers

It isn't every day that one hears a major telecom regulator call for significant consolidation of providers in a market. But that is precisely what Europe's top technology regulator, Neelie Kroes,European Community commissioner for the "Digital Agenda," says is necessary in Europe.

Further mergers would create a handful of strong cross-border telecom leaders, which can invest more in mobile and broadband networks to close the gap with the United States and Asia, Reuters reports.

To be sure, Europe's market is more fragmented than that of the United States, China, Canada or Australia, larger countries where a relative handful of leading firms already is the pattern. To the extent that communications is a scale business, larger size makes a difference.

What might not be so clear is the extent to which a wave of mergers and consolidation necessarily would provide a better climate for investments in fiber to home facilities the EC wants to see built.

At a tactical level, current calls for even-lower wholesale rates for leasing copper access facilities to competitors will create a worse climate for fiber investments.

Further mergers would create a handful of strong cross-border telecom leaders, which can invest more in mobile and broadband networks to close the gap with the United States and Asia, Reuters reports.

To be sure, Europe's market is more fragmented than that of the United States, China, Canada or Australia, larger countries where a relative handful of leading firms already is the pattern. To the extent that communications is a scale business, larger size makes a difference.

What might not be so clear is the extent to which a wave of mergers and consolidation necessarily would provide a better climate for investments in fiber to home facilities the EC wants to see built.

At a tactical level, current calls for even-lower wholesale rates for leasing copper access facilities to competitors will create a worse climate for fiber investments.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Entertainment Spending Grows, Digital Grows Faster

The communications and major media businesses are alike in some ways. The economics of the businesses favor firms that can operate at scale.

Both have a business-to-consumer as well as a business-to-business component. Among the differences is the advertising revenue models that are more important for much of media.

Communications still is dominated by subscription sales.

But the "media" business is fundamentally unlike the communications business in one sense. It is based on "scarcity" to a much greater extent than the communications business.

Media also is about "audiences," not "subscribers" or "users." That is not to say subscribers and users are unimportant.

It is to say that media succeeds only when it creates engagement and attention. And that turns out to be a matter of "art," not science.

There is plenty of "media" produced and consumed, but precious little of it attracts any significant amount of advertising support.

That scarcity accounts for the different pricing mechanisms in media and communications.

Where retail prices can, and do, rise every year in media, prices tend to decline in communications, even as both types of industries shift to a digital format.

Digital's share of total spend will grow from 28 percent in 2011 to 37.5 percent in 2016, and digital spending will account for 67 percent of total entertainment and media spending growth to 2016.

That includes both consumer spending on content as well as advertising.

Global spending on digital recorded music formats will overtake physical distribution in 2015, reaching 55 percent of total revenues in 2016.

And global spending on online and wireless video games will overtake console and PC games revenues in 2013.

By contrast, the digital component of consumer magazines will account for only 10.4 percent of spending by 2016, up from 3.1 percent in 2011.

Both have a business-to-consumer as well as a business-to-business component. Among the differences is the advertising revenue models that are more important for much of media.

Communications still is dominated by subscription sales.

But the "media" business is fundamentally unlike the communications business in one sense. It is based on "scarcity" to a much greater extent than the communications business.

Media also is about "audiences," not "subscribers" or "users." That is not to say subscribers and users are unimportant.

It is to say that media succeeds only when it creates engagement and attention. And that turns out to be a matter of "art," not science.

There is plenty of "media" produced and consumed, but precious little of it attracts any significant amount of advertising support.

That scarcity accounts for the different pricing mechanisms in media and communications.

Where retail prices can, and do, rise every year in media, prices tend to decline in communications, even as both types of industries shift to a digital format.

Global entertainment and media spending on digital advertising and consumer formats increased by 17.6 percent in 2011, for example, according to PwC.

Digital's share of total spend will grow from 28 percent in 2011 to 37.5 percent in 2016, and digital spending will account for 67 percent of total entertainment and media spending growth to 2016.

That includes both consumer spending on content as well as advertising.

Global spending on digital recorded music formats will overtake physical distribution in 2015, reaching 55 percent of total revenues in 2016.

And global spending on online and wireless video games will overtake console and PC games revenues in 2013.

By contrast, the digital component of consumer magazines will account for only 10.4 percent of spending by 2016, up from 3.1 percent in 2011.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, June 11, 2012

Wi-Fi Overhead Becoming an Issue?

Wi-Fi, the well-known standard for wireless internet, is reaching its technical limits in areas of high usage, a study suggests. Wi-Fi efficiency, measured as a percentage of theoretical ability to handle "bearer" traffic, compared to signaling overhead, drops significantly in busy surroundings where many different networks and numerous wireless internet enabled devices are operating, the study suggests.

In some cases, the amount of bearer traffic that can be carried can drop to less than 20 percent.

In some cases, the amount of bearer traffic that can be carried can drop to less than 20 percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Handheld Gaming Devices in Downward Spiral Because of Smart Phones, Tablets

Over 38 million handheld gaming devices from Sony and Nintendo are expected to ship in 2013, a maximum that is significantly lower than the previous peak of 47 million units in 2008, according to ABI Research.

That is one sign that casual gaming has shifted to smart phones and now tablets, and away from dedicated mobile game consoles.

Unit shipments following 2013 are expected to decline slightly, but dedicated handheld gaming devices are a sustainable niche, ABI Research argues, with forecasts relatively flat through 2017.

That is one sign that casual gaming has shifted to smart phones and now tablets, and away from dedicated mobile game consoles.

Unit shipments following 2013 are expected to decline slightly, but dedicated handheld gaming devices are a sustainable niche, ABI Research argues, with forecasts relatively flat through 2017.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Do Mobile Data Plans Reflect or Shape Usage?

What is the relationship between the structure of a data plan and usage? Do people adapt behavior to the plans, or does the choice of a data plan reflect existing behavior? It’s a harder question than might first appear, as several processes likely are at work.

Over time, people tend to consume more data. Use of video-based applications is growing. But virtually all studies show that, even in instances where bandwidth usage actually is “unlimited,” or so generous that no typical user ever approaches a limit, only a small percentage of users actually push the limits.

It is an unquestioned fact that a small percentage of broadband users, on virtually any network, use vastly more data than typical users do. The top one percent of data consumers account for 20 percent of the overall consumption, for example, a fact the study by Benoît Felten, Yankee Group analyst, confirms.

But users also seem to be able to adjust their behavior and expectations. When bandwidth usage carries direct financial implications, people adjust by changing their behavior, switching their smart phones to Wi-Fi access when at home, for example.

Also, data from Ericsson suggests a bit of both processes might be at work. It appears that, over time, virtually all users consume more bandwidth.

But “typical usage” remains a far different issue from “average” usage. Even as overall usage grows, a small percentage of very-heavy users represents a disproportionate amount of usage. In that sense, choice of data plans follows behavior. Heavier users will seek the biggest plans. Lighter users will choose plans with less capacity, when available.

On the other hand, usage patterns are also related to the data plan that comes with a device. That is significant because it suggests people actually modify their behavior based on plan policies. In other words, the Ericsson study suggests, people use more when their plan allows it.

If so, service providers have a wide range of options for shaping end user demand, using price and other packaging mechanisms. Generally speaking, people use more data when they buy bigger buckets of usage.

But it is a nuanced matter. It can’t be precisely determined whether people use more data because they have bigger plans, or have bigger plans because they use more data over time.

Also, since new devices aside from phones tend to get used over time (notebooks and tablets), and since usage profiles for those other devices are different from phones, consumer usage and shaping of retail plans also will tend to change over time.

On the other hand, one might argue, given any set range of plans, users will virtually always fall into a distribution that is stable and predictable.

“Nearly all communications traffic, including Internet traffic, can be approximated with high accuracy by the log-normal distribution,” says Phoenix Center Chief Economist Dr. George S. Ford. That’s important, as it means we generally can predict overall end user behavior when we actually know only a couple of key data points.

Among the practical implications are estimates of what is likely to happen when a broadband service provider imposes a monthly usage cap of 250 gigabytes. The log-normal distribution suggests how many customers would hit the limit.

The log-normal distribution also generally allows some estimation of how consumption will vary across the entire customer base, knowing only the consumption of the top one percent, and the consumption of the top 10 percent of users, an analysis by Dr. Ford suggests.

The point is that “averages” (the arithmetic mean) don’t tell an observer very much when any service has an asymmetric distribution, as always seems to be the case for Internet consumption by consumers.

Cisco’s Visual Networking Index reports that the top one percent of users accounted for more than 20 percent of Internet traffic and that the top 10 percent of users accounted for 60 percent

of traffic.

That means a Pareto distribution, which would ideally show that 20 percent of instances account for 80 percent of the impact would also likely hold.

Ford notes that Comcast’s 250 GByte per month usage cap on its residential broadband

customers, taken with Comcast’s own statements that 99 percent of its residential customers will not approach that cap suggests that only one percent of Comcast’s residential users consume 250 GBytes per month or more.

Comcast also indicated that its median customer consumes about 8 GBytes to 10 GBytes per month.

The log-normal distribution could well inform many other sorts of policies, such as what amount of consumption a “typical” user requires.

“My approach to approximating usage patterns may be useful for variety of policy issues,” says Ford. “ For example, when addressing universal service for broadband, the level of service that qualifies as ‘broadband’ will have to be parameterized.”

Knowledge of the usage distribution may aid in establishing these service level definitions that can be described as “reasonably comparable to those services provided in urban areas, for example.

The relationship between “typical” usage and “heavy” usage seems to be internally consistent, no matter what the “heavy” consumption levels might be.

Over time, people tend to consume more data. Use of video-based applications is growing. But virtually all studies show that, even in instances where bandwidth usage actually is “unlimited,” or so generous that no typical user ever approaches a limit, only a small percentage of users actually push the limits.

It is an unquestioned fact that a small percentage of broadband users, on virtually any network, use vastly more data than typical users do. The top one percent of data consumers account for 20 percent of the overall consumption, for example, a fact the study by Benoît Felten, Yankee Group analyst, confirms.

But users also seem to be able to adjust their behavior and expectations. When bandwidth usage carries direct financial implications, people adjust by changing their behavior, switching their smart phones to Wi-Fi access when at home, for example.

Also, data from Ericsson suggests a bit of both processes might be at work. It appears that, over time, virtually all users consume more bandwidth.

But “typical usage” remains a far different issue from “average” usage. Even as overall usage grows, a small percentage of very-heavy users represents a disproportionate amount of usage. In that sense, choice of data plans follows behavior. Heavier users will seek the biggest plans. Lighter users will choose plans with less capacity, when available.

On the other hand, usage patterns are also related to the data plan that comes with a device. That is significant because it suggests people actually modify their behavior based on plan policies. In other words, the Ericsson study suggests, people use more when their plan allows it.

If so, service providers have a wide range of options for shaping end user demand, using price and other packaging mechanisms. Generally speaking, people use more data when they buy bigger buckets of usage.

But it is a nuanced matter. It can’t be precisely determined whether people use more data because they have bigger plans, or have bigger plans because they use more data over time.

Also, since new devices aside from phones tend to get used over time (notebooks and tablets), and since usage profiles for those other devices are different from phones, consumer usage and shaping of retail plans also will tend to change over time.

On the other hand, one might argue, given any set range of plans, users will virtually always fall into a distribution that is stable and predictable.

“Nearly all communications traffic, including Internet traffic, can be approximated with high accuracy by the log-normal distribution,” says Phoenix Center Chief Economist Dr. George S. Ford. That’s important, as it means we generally can predict overall end user behavior when we actually know only a couple of key data points.

Among the practical implications are estimates of what is likely to happen when a broadband service provider imposes a monthly usage cap of 250 gigabytes. The log-normal distribution suggests how many customers would hit the limit.

The log-normal distribution also generally allows some estimation of how consumption will vary across the entire customer base, knowing only the consumption of the top one percent, and the consumption of the top 10 percent of users, an analysis by Dr. Ford suggests.

The point is that “averages” (the arithmetic mean) don’t tell an observer very much when any service has an asymmetric distribution, as always seems to be the case for Internet consumption by consumers.

Cisco’s Visual Networking Index reports that the top one percent of users accounted for more than 20 percent of Internet traffic and that the top 10 percent of users accounted for 60 percent

of traffic.

That means a Pareto distribution, which would ideally show that 20 percent of instances account for 80 percent of the impact would also likely hold.

Ford notes that Comcast’s 250 GByte per month usage cap on its residential broadband

customers, taken with Comcast’s own statements that 99 percent of its residential customers will not approach that cap suggests that only one percent of Comcast’s residential users consume 250 GBytes per month or more.

Comcast also indicated that its median customer consumes about 8 GBytes to 10 GBytes per month.

The log-normal distribution could well inform many other sorts of policies, such as what amount of consumption a “typical” user requires.

“My approach to approximating usage patterns may be useful for variety of policy issues,” says Ford. “ For example, when addressing universal service for broadband, the level of service that qualifies as ‘broadband’ will have to be parameterized.”

Knowledge of the usage distribution may aid in establishing these service level definitions that can be described as “reasonably comparable to those services provided in urban areas, for example.

The relationship between “typical” usage and “heavy” usage seems to be internally consistent, no matter what the “heavy” consumption levels might be.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Financial analysts typically express concern when any firm’s customer base is too concentrated. Consider that, In 2024, CoreWeave’s top two ...