Mobile service providers have not achieved much market share from content sales globally at least as measured by volume of downloads, Juniper Research estimates.

Mobile operator storefronts and portals now account for about six percent of content downloads worldwide, with Google Play and Apple’s App Store now comprising nearly 70 percent between them.

That has lead many operators to close their own storefronts, Juniper Research says. On the other hand, the value of mobile content that could be sold using direct carrier billing could rise from $2 billion in 2012 to more than $13 billion by 2017, according to Juniper Research.

Direct carrier billing might therefore be said to represent a more lucrative mobile service provider revenue opportunity than selling mobile content.

Analysys Mason forecasts that direct carrier billing will provide service providers with more than US$12 billion in revenue in 2022.

According to mobile applications vendor Ebscer, since BlackBerry introduced carrier billing in August 2010, the percent of sales coming from carrier billing has increased every month for Ebscer.

At the end of April 2011, over 25 percent of total app sales for Ebscer in BlackBerry App World were coming from operator billing.

Wednesday, March 6, 2013

Service Providers Not Making Much Money from Mobile Content, Billing for It Is More Lucrative

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Who Does Google Compete With?

Who does Google compete with, strategically? Over the years, many names have been discussed, including Yahoo, Microsoft or Apple. Google sometimes is said to be unable to compete with some others, such as Facebook. But increasingly, the name that appears is "Amazon."

So it is that Google has begun testing a same-day delivery service with retailers, a move that obviously will be seen as part of a wider head to head competition with Amazon in the e-commerce space, as part of Google Shopping Express.

For a firm historically associated with an advertising revenue base, that might sound odd. But lots of application providers and some service providers now see "mobile commerce" as the next big revenue frontier, with angles ranging from promotion to payments to couponing and payments, as well as a broader "product sales" function.

That shift might see Goolge Shopping Express evolve in the direction of becoming a full marketplace, more like Amazon.

So it is that Google has begun testing a same-day delivery service with retailers, a move that obviously will be seen as part of a wider head to head competition with Amazon in the e-commerce space, as part of Google Shopping Express.

For a firm historically associated with an advertising revenue base, that might sound odd. But lots of application providers and some service providers now see "mobile commerce" as the next big revenue frontier, with angles ranging from promotion to payments to couponing and payments, as well as a broader "product sales" function.

That shift might see Goolge Shopping Express evolve in the direction of becoming a full marketplace, more like Amazon.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Leap Doesn't Find iPhones Too Helpful, Apparently

One has to wonder whether the highest-end devices are such a good match for value segment mobile customers.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Broadband Matters When People Figure Out What to Do with It

"The U.K.’s broadband market is already in rude health," said Ed Vaizy, U.K. Parliamentary Under Secretary of State for Culture, Communications and Creative Industries. What the heck does that mean?

Basically, that the United Kingdom has done a good job of bringing low cost broadband access to its people, offering access at low prices, caused by high degrees of market competition. Challenges remain, particularly in rural areas.

"The U.K. currently benefits from low prices and a high degree of competition in the broadband market," said Vaizy. "The U.K. has the best deals available for consumers across a selection of pricing bundles in the major European economies."

But the role of "demand stimulation" also was cited as key. In other words, beyond making access possible, as much hinges on people figuring out ways to use broadband to grow the economy.

"But we cannot create a world class connected Britain just by laying more fiber in the ground or building new base stations," Vaizy said. " It is also crucial that we get as many people as possible online enjoying the benefits presented by better connectivity, and also encourage British companies to expand and develop their internet-based operations."

"Ultimately it is users that will turn infrastructure investment into growth," he said.

In other words, a fixation on "raw speed" is misplaced. What ultimately matters more is what people figure out they can do with broadband, in ways that benefit the economy.

Basically, that the United Kingdom has done a good job of bringing low cost broadband access to its people, offering access at low prices, caused by high degrees of market competition. Challenges remain, particularly in rural areas.

"The U.K. currently benefits from low prices and a high degree of competition in the broadband market," said Vaizy. "The U.K. has the best deals available for consumers across a selection of pricing bundles in the major European economies."

But the role of "demand stimulation" also was cited as key. In other words, beyond making access possible, as much hinges on people figuring out ways to use broadband to grow the economy.

"But we cannot create a world class connected Britain just by laying more fiber in the ground or building new base stations," Vaizy said. " It is also crucial that we get as many people as possible online enjoying the benefits presented by better connectivity, and also encourage British companies to expand and develop their internet-based operations."

"Ultimately it is users that will turn infrastructure investment into growth," he said.

In other words, a fixation on "raw speed" is misplaced. What ultimately matters more is what people figure out they can do with broadband, in ways that benefit the economy.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

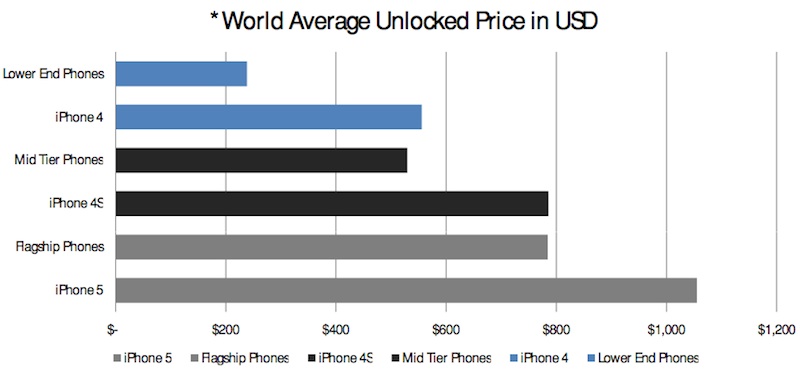

How Much Difference Will Unlocked Phones Make?

It’s hard to ascertain the real prospects for actual movement by the U.S. federal government to mandate mobile phone unlocking in the U.S. market. But it would be fair to say that is the sort of issue politicians like. It makes them sound very “pro-consumer,” at little “cost.”

That’s a dangerous combination for any industry. But it might also be fair to note that the actual benefits to consumers might be relatively modest, even if such new rules were to become part of the framework of mobile “consumer protection and choice,” as it is certain the matter would be sold.

Presumably, the value of unlocked devices will becomes a bigger actual value to consumers only when Long Term Evolution fourth generation networks are fully established in the U.S. market, for some simple reasons.

Unlike many other countries, subscribers and networks are at the moment split into GSM (AT&T and T-Mobile USA) and CDMA (Verizon Wireless and Sprint) air interface camps. An unlocked CDMA device cannot be used on the AT&T and T-Mobile USA neteworks, while a GSM unlocked device cannot be used on the Verizon or Sprint networks.

So while the idea “sounds nice,” the actual amount of consumer value is much less than most probably would think. That is not to say there is “no” value, only that the actual value might wind up being rather minor.

And some would say it doesn’t make sense to cause potential major damage to obtain a relatively small amount of benefit.

But the value of unlocking might be more subtle than many expect. If unlocked phones are sold at full retail prices, when consumers have the choice of a subsidized device, it seems likely to expect most consumers still will continue to opt for a subsidized device. That is especially true for the popular higher end devices.

Not many consumers are going to prefer shelling out full retail price for the latest Apple iPhone, even if they can, when the alternative is a lower device acquisition price, even at the cost of higher monthly recurring costs than might be possible if subsidies were not offered and available.

Beyond that, unlocking might help some consumers and provider segments, especially users on the “value” end of the market, and some firms that specialize in refurbishing and selling reconditioned devices.

That might be helpful for some businesses, and some U.S. consumers. ReCellular has been said to be one of the largest U.S.-based mobile phone refurbishers, and a mandatory “unlocked” phone regime might help such firms by boosting the value of used devices, at least marginally.

ReCellular resold or recycled 5.2 million mobile devices in 2010. ReCellular sells about 60 percent of its phones in the U.S. market and the rest mostly to dealers in Asia, Africa, Latin America and Eastern Europe.

But one might note that the market for used phones is relatively small. Global sales of used phones total a few hundred million units a year, estimates Andy Castonguay, an analyst at consulting firm Yankee Group. That compares with the 1.6 billion new phones sold world-wide last year.

That is only a proxy for the degree to which U.S. consumers might actually take their unlocked phones and switch to a different service provider.

For one thing, most consumers do not seem to keep any single device all that long. According to one U.S. study, the typical mobile device is used 18 months before being replaced. Whether that would be different in an unlocked device context is unclear.

The point is that people in the U.S. market mostly do not seem to want to keep their devices that long, whether they use one service provider or had a device that enabled easy switching. Keep in mind that the 18-month figure, like all “averages,” hides the differences between some users who will keep any device longer, and some who will replace devices even faster than 18 months.

That is not to say device unlocking would have zero advantages for end users and some businesses. It is harder to say what such rules might do for device innovation or the fortunes of mobile service providers.

Service provider revenues might be lower in an unlocked phone regime, since device sales count as “revenue,” and since unlocked device service plans would likely be lower than current plans that include the subsidy recovery.

And it is hard to see how competition between service providers would be less robust, in a full unlocked device regime, than under the current situation.

Service providers might sell fewer phones in the first place, as retail distribution shifts to third party retailers. Whether that helps or hurts service providers is tough to say, with precision.

On the other hand, service providers might benefit. The cost of phone subsidies might drop, so lower “revenue” might also be balanced by lower operating costs.

But service providers might have less ability to “control” customers or stabilize expected revenues that are “less lumpy” because the current two-year contracts reduce churn.

The point is that although the conventional wisdom is that mandatory phone unlocking will help consumers and harm service providers, it is not clear how big those changes might be. Every action has unintended consequences beyond the reactions service providers will undertake.

That’s a dangerous combination for any industry. But it might also be fair to note that the actual benefits to consumers might be relatively modest, even if such new rules were to become part of the framework of mobile “consumer protection and choice,” as it is certain the matter would be sold.

Presumably, the value of unlocked devices will becomes a bigger actual value to consumers only when Long Term Evolution fourth generation networks are fully established in the U.S. market, for some simple reasons.

Unlike many other countries, subscribers and networks are at the moment split into GSM (AT&T and T-Mobile USA) and CDMA (Verizon Wireless and Sprint) air interface camps. An unlocked CDMA device cannot be used on the AT&T and T-Mobile USA neteworks, while a GSM unlocked device cannot be used on the Verizon or Sprint networks.

So while the idea “sounds nice,” the actual amount of consumer value is much less than most probably would think. That is not to say there is “no” value, only that the actual value might wind up being rather minor.

And some would say it doesn’t make sense to cause potential major damage to obtain a relatively small amount of benefit.

But the value of unlocking might be more subtle than many expect. If unlocked phones are sold at full retail prices, when consumers have the choice of a subsidized device, it seems likely to expect most consumers still will continue to opt for a subsidized device. That is especially true for the popular higher end devices.

Not many consumers are going to prefer shelling out full retail price for the latest Apple iPhone, even if they can, when the alternative is a lower device acquisition price, even at the cost of higher monthly recurring costs than might be possible if subsidies were not offered and available.

Beyond that, unlocking might help some consumers and provider segments, especially users on the “value” end of the market, and some firms that specialize in refurbishing and selling reconditioned devices.

That might be helpful for some businesses, and some U.S. consumers. ReCellular has been said to be one of the largest U.S.-based mobile phone refurbishers, and a mandatory “unlocked” phone regime might help such firms by boosting the value of used devices, at least marginally.

ReCellular resold or recycled 5.2 million mobile devices in 2010. ReCellular sells about 60 percent of its phones in the U.S. market and the rest mostly to dealers in Asia, Africa, Latin America and Eastern Europe.

But one might note that the market for used phones is relatively small. Global sales of used phones total a few hundred million units a year, estimates Andy Castonguay, an analyst at consulting firm Yankee Group. That compares with the 1.6 billion new phones sold world-wide last year.

That is only a proxy for the degree to which U.S. consumers might actually take their unlocked phones and switch to a different service provider.

For one thing, most consumers do not seem to keep any single device all that long. According to one U.S. study, the typical mobile device is used 18 months before being replaced. Whether that would be different in an unlocked device context is unclear.

The point is that people in the U.S. market mostly do not seem to want to keep their devices that long, whether they use one service provider or had a device that enabled easy switching. Keep in mind that the 18-month figure, like all “averages,” hides the differences between some users who will keep any device longer, and some who will replace devices even faster than 18 months.

That is not to say device unlocking would have zero advantages for end users and some businesses. It is harder to say what such rules might do for device innovation or the fortunes of mobile service providers.

Service provider revenues might be lower in an unlocked phone regime, since device sales count as “revenue,” and since unlocked device service plans would likely be lower than current plans that include the subsidy recovery.

And it is hard to see how competition between service providers would be less robust, in a full unlocked device regime, than under the current situation.

Service providers might sell fewer phones in the first place, as retail distribution shifts to third party retailers. Whether that helps or hurts service providers is tough to say, with precision.

On the other hand, service providers might benefit. The cost of phone subsidies might drop, so lower “revenue” might also be balanced by lower operating costs.

But service providers might have less ability to “control” customers or stabilize expected revenues that are “less lumpy” because the current two-year contracts reduce churn.

The point is that although the conventional wisdom is that mandatory phone unlocking will help consumers and harm service providers, it is not clear how big those changes might be. Every action has unintended consequences beyond the reactions service providers will undertake.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, March 5, 2013

More Rumors about Verizon Buyout of Vodafone Stake in Verizon Wireless

That there are new rumors about Verizon wanting to acquire the rest of Vodafone’s stake in Verizon Wireless is not surprising. Vodafone recently denied any such talks were underway.

Such denials are commonplace in both politics and business. And though the denials are not always a cover for actual talks, Vodafone’s latest quarterly financial report illustrates the reasons why some analysts and executives at Verizon, might be weighing some action to change the current ownership status of Verizon Wireless.

To be sure, Verizon also has said no such talks are underway. In fact, Verizon recently said no talks about a full purchase of the 45 percent Vodafone stake in Verizon were underway.

That would still leave some room for less complicate measures, such as a gradual purchase by Verizon of Vodafone shares. Some also would say a full-blown merger is a possibility. Sure, it might be, but such a huge deal would present at least some significant regulatory issues.

Where the U.S. Federal Communications Commission would allow Verizon to become that much bigger is a valid question, even though either a buyout of the Vodafone stake, or a full merger, would not immediately affect U.S. mobile market share.

Vodafone posted a worse than expected drop in group revenue for the last three months of 2012, and Vodafone might prefer to liquify its Verizon Wireless stake to pay down debt, for example.

Beyond that, low interest rates make acquisitions attractive at the moment, in large part because organic growth opportunities are limited.

Such denials are commonplace in both politics and business. And though the denials are not always a cover for actual talks, Vodafone’s latest quarterly financial report illustrates the reasons why some analysts and executives at Verizon, might be weighing some action to change the current ownership status of Verizon Wireless.

To be sure, Verizon also has said no such talks are underway. In fact, Verizon recently said no talks about a full purchase of the 45 percent Vodafone stake in Verizon were underway.

That would still leave some room for less complicate measures, such as a gradual purchase by Verizon of Vodafone shares. Some also would say a full-blown merger is a possibility. Sure, it might be, but such a huge deal would present at least some significant regulatory issues.

Where the U.S. Federal Communications Commission would allow Verizon to become that much bigger is a valid question, even though either a buyout of the Vodafone stake, or a full merger, would not immediately affect U.S. mobile market share.

Vodafone posted a worse than expected drop in group revenue for the last three months of 2012, and Vodafone might prefer to liquify its Verizon Wireless stake to pay down debt, for example.

Beyond that, low interest rates make acquisitions attractive at the moment, in large part because organic growth opportunities are limited.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, March 4, 2013

U.K. 4G LTE Frequency Allotments

After some trading activity, the actual spectrum allotments for U.K. 4G LTE providers appear to be set.

The middle block is the Time Division Duplex spectrum, the surrounding ones are uplink and downlink pairs

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

There's a Good Reason Why Big Public Companies Rarely Lead Innovation

Big public companies are not often noted for their innovativeness. But there's a good reason. The pressure to perform, every quarter, tends to drive out other longer-term activities for which the immediate return is minimal.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Fon, Deutsche Telekom Do a Deal

Fon, the global Wi-Fi network, is built by consumers who contribute to the network, and is not "carrier owned" or even "carrier class" in the traditional sense.

But that has not stopped Deutsche Telekom from partnering with Fon to build Germany’s largest Wi-Fi network. The "WLAN To Go" network will launch in the summer of 2013, and is inttended to provide greater Wi-Fi offload capabilities for DT and its customers.

The deal illustrates the porosity of "access" methods in a communications environment that increasingly features a mix of "carrier-owned," "carrier grade," "best effort" and "assured quality" networks.

Given the traditional carrier preference for licensed spectrum rather than unlicensed, and wires rather than wireless for backhaul, the new deal signifies a much more flexible approach to access, overall.

But that has not stopped Deutsche Telekom from partnering with Fon to build Germany’s largest Wi-Fi network. The "WLAN To Go" network will launch in the summer of 2013, and is inttended to provide greater Wi-Fi offload capabilities for DT and its customers.

The deal illustrates the porosity of "access" methods in a communications environment that increasingly features a mix of "carrier-owned," "carrier grade," "best effort" and "assured quality" networks.

Given the traditional carrier preference for licensed spectrum rather than unlicensed, and wires rather than wireless for backhaul, the new deal signifies a much more flexible approach to access, overall.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Samsung Galaxy IV is Coming

In the smart phone race, installed base matters. Coolness matters. Advertising and marketing budgets matter. And Samsung is spending.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sunday, March 3, 2013

Will Europe Reach U.S. Scale; Will U.S. Data Prices Reach Europe Levels?

![[image]](http://si.wsj.net/public/resources/images/MK-CB244_DATA_NS_20130228184520.jpg) In Europe, more than 100 mobile service providers, owned by some 40 companies, serve a population of 505 million. In the United States, four national providers, with market share between 93 percent and 96 percent, serve most of a population of 314 million.

In Europe, more than 100 mobile service providers, owned by some 40 companies, serve a population of 505 million. In the United States, four national providers, with market share between 93 percent and 96 percent, serve most of a population of 314 million. Regulatory fragmentation, in the form of 27 separate and sovereign regulatory entities is another problem service providers say has to be addressed. Service providers would prefer a single European regulator and consistent policies across EU nations.

European service providers say their situation is untenable, and are lobbying regulators very hard for permission to rationalize the business by significant merger and acquisition activity.

In a scale business, those differences probably account for the better financial performance of U.S. mobile service providers.

For U.S. service providers, there is a different sort of concern, namely a convergence of prices for mobile data services that might potentially entail EU prices rising a bit, and U.S. prices declining more substantially.

In part, that could come from more severe price competition in the U.S. market, in part from changes in device portability, in part from changes in device subsidy policies and possibly from a shift of end user mobile data demand (offloading to Wi-Fi).

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Potential New Rules, Taxes Illustrate Regulatory Pressures

In most countries, voice communications, Internet communications, broadcast media, cable TV and broadcasting have been governed by distinct sets of regulations. That made more sense in an era when each type of service was provided by a distinct and purpose-built network.

These days, as all media types can be delivered by all or most networks, there will be a bigger discontinuity between the older forms of regulation and the ways services are created and delivered, across networks.

Sweden's new policy of taxing use of PCs and tablets to watch the state-owned TV service, and a German decision on copyright fees, neatly illustrate some of the regulatory challenges that accompany changing communications and entertainment ecosystems.

Traditionally, Swedish households owning televisions have paid a monthly tax of SEK173 ($27) per month to support Sveriges Television, Sveriges Radio and educational broadcasting known as Utbildningsradion.

But Sweden's Radiotjänst collection agency now is collecting the fee even from Internet-connected computers. The logic is that, in some cases, PCs are used as “TV devices.”

German lower house of parliament separately approved a copyright bill that protects Internet search firms from payment of fees to newspapers and other print publishers when snippets of stories are included in search engine results.

The bill's original draft would have allowed newspapers and other print publishers to stop search companies from showing text snippets, unless they paid licensing fees. The bill still has to win approval in the upper house, which is expected to oppose the current version of the legislation.

The other angle is that the bill does not fully settle the issue of whether search engine applications might have to pay publishers if news aggregators publish bigger amounts of content.

The move by Radiotjänst effectively makes a key form of broadcasting regulation applicable to PCs, notebooks and tablets, in a real sense, even when owners of tablets or PCs do not watch TV. The tax is applied to a households that own Internet connected PCs, but not TVs, whether or not people in the household actually watch television or not.

Smart phones have been exempted from the law, at least for the moment, on grounds that the primary function of a smart phone is communications, not “watching TV.” Obviously, that distinction will be virtually impossible to maintain over the long term. But there is an existing principle that the “TV tax” applies to a “household,” not devices.

Presumably, that means Swedish households without TVs, but using Internet-connected PCs or tablets, will pay the fee only once, and will not have to pay for smart phone use, in addition to tablet or PC access.

Households that do not own PCs or tablets (possibly only a small fraction of all households), and do use smart phones, might ultimately be forced to pay the fee as well. The point is not whether it is “fair” or “right” for Sweden, the United Kingdom or Denmark to tax owners of TVs.

The point is that rapid changes in user behavior and device capabilities are changing the actual environment within which regulatory policy is conducted. Any nation that has distinct regulatory regimes for broadcasting, communications, Internet and print media will increasingly have to confront the growing contradictions and irrationality of older forms of regulation.

These days, as all media types can be delivered by all or most networks, there will be a bigger discontinuity between the older forms of regulation and the ways services are created and delivered, across networks.

Sweden's new policy of taxing use of PCs and tablets to watch the state-owned TV service, and a German decision on copyright fees, neatly illustrate some of the regulatory challenges that accompany changing communications and entertainment ecosystems.

Traditionally, Swedish households owning televisions have paid a monthly tax of SEK173 ($27) per month to support Sveriges Television, Sveriges Radio and educational broadcasting known as Utbildningsradion.

But Sweden's Radiotjänst collection agency now is collecting the fee even from Internet-connected computers. The logic is that, in some cases, PCs are used as “TV devices.”

German lower house of parliament separately approved a copyright bill that protects Internet search firms from payment of fees to newspapers and other print publishers when snippets of stories are included in search engine results.

The bill's original draft would have allowed newspapers and other print publishers to stop search companies from showing text snippets, unless they paid licensing fees. The bill still has to win approval in the upper house, which is expected to oppose the current version of the legislation.

The other angle is that the bill does not fully settle the issue of whether search engine applications might have to pay publishers if news aggregators publish bigger amounts of content.

The move by Radiotjänst effectively makes a key form of broadcasting regulation applicable to PCs, notebooks and tablets, in a real sense, even when owners of tablets or PCs do not watch TV. The tax is applied to a households that own Internet connected PCs, but not TVs, whether or not people in the household actually watch television or not.

Smart phones have been exempted from the law, at least for the moment, on grounds that the primary function of a smart phone is communications, not “watching TV.” Obviously, that distinction will be virtually impossible to maintain over the long term. But there is an existing principle that the “TV tax” applies to a “household,” not devices.

Presumably, that means Swedish households without TVs, but using Internet-connected PCs or tablets, will pay the fee only once, and will not have to pay for smart phone use, in addition to tablet or PC access.

Households that do not own PCs or tablets (possibly only a small fraction of all households), and do use smart phones, might ultimately be forced to pay the fee as well. The point is not whether it is “fair” or “right” for Sweden, the United Kingdom or Denmark to tax owners of TVs.

The point is that rapid changes in user behavior and device capabilities are changing the actual environment within which regulatory policy is conducted. Any nation that has distinct regulatory regimes for broadcasting, communications, Internet and print media will increasingly have to confront the growing contradictions and irrationality of older forms of regulation.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Moral Outrage Over "Loosely Coupled Networks" is Misplaced

Lots of start-ups find they actually change revenue models models on the way to building a sustainable business, compared to what they originally were funded to undertake. But there are lots of more-subtle ways businesses wind up providing value in the Internet ecosystem, for end users and other business partners, even when nothing “Internet” is actually directly related to their actual revenue streams.

These days, it is common for Internet service providers, for example, to lament the way value, revenue and equity valuations are created by successful application providers who do not have a formal and direct relationship with access providers.

That leads to ISP efforts to create such business and therefore revenue relationships between some popular application providers. One might say there is almost a sense of moral outrage that in a loosely-coupled ecosystem, companies are able to build big, valuable Internet-based businesses without necessarily having a direct business relationship with any access provider.

One might well argue that a healthy ISP business, broadly defined, is in the consumer interest, the public interest or the national interest. One might well debate various ways to ensure that this outcome is achieved.

But some of us might argue that the sense of moral outrage is misplaced. One might argue that telecom service providers would not have preferred the loosely-coupled “Internet” as a major communications architecture able to rival their own “closed” and tightly-coupled networks.

One might argue about the degree to which telecom organizations and interests, as opposed to “Internet” organizations and interests, “created” the Internet. But it is hard to argue that telecom interests did not help create the protocols and networks, or that global service providers have not selected Internet Protocol as the foundation of their next generation networks.

That is not to say that all IP networks are “the public Internet,” or that all business models using IP are equivalent. They are not.

But the moral outrage about loosely-coupled networks is more than a bit wrong. Everyone now agrees that this is the way software gets written and that this is the way modern networks operate. The actual ownership of applications and services will vary (some tightly coupled, but most only loosely coupled).

But loose coupling (“over the top” apps) is the way we all have decided modern networks will work. That is not to say, as some once did around the turn of the century, that “bandwidth wants to be free.” That is not to argue the importance of maintaining viable access networks, or the legitimate challenges that have to be faced as massive changes occur in ISP revenue sources.

But the moral outrage really is misplaced. The layered model, by definition, presupposes separation of the application and other layers, including physical and transport layers. It therefore is not surprising at all that new revenue models and business categories now exist, and that such businesses exist without the “permission” of participants working at other layers.

The emergence of loosely coupled networks is profoundly disturbing for legacy access providers, to be sure, even if all service providers now accept such models as the foundation of their own next generation networks.

But any sense of moral outrage or entitlement is wrong and misplaced. Without question, we will need viable and profitable ISPs to support the Internet ecosystem. And video applications do pose issues for ISPs that are very complicated and challenging in a loosely coupled framework.

But that’s the nature of the networks we all have chosen to build and use. In that sense, and without diminishing the legitimate need for strong, financially viable ISP businesses, moral outrage probably is not helpful.

This is the communications world we all have chosen to live in, and some would argue it is a good model. The magnitude of transition issues for access providers should not be underestimated. But in a loosely coupled world, application providers create value, they do not steal it.

These days, it is common for Internet service providers, for example, to lament the way value, revenue and equity valuations are created by successful application providers who do not have a formal and direct relationship with access providers.

That leads to ISP efforts to create such business and therefore revenue relationships between some popular application providers. One might say there is almost a sense of moral outrage that in a loosely-coupled ecosystem, companies are able to build big, valuable Internet-based businesses without necessarily having a direct business relationship with any access provider.

One might well argue that a healthy ISP business, broadly defined, is in the consumer interest, the public interest or the national interest. One might well debate various ways to ensure that this outcome is achieved.

But some of us might argue that the sense of moral outrage is misplaced. One might argue that telecom service providers would not have preferred the loosely-coupled “Internet” as a major communications architecture able to rival their own “closed” and tightly-coupled networks.

One might argue about the degree to which telecom organizations and interests, as opposed to “Internet” organizations and interests, “created” the Internet. But it is hard to argue that telecom interests did not help create the protocols and networks, or that global service providers have not selected Internet Protocol as the foundation of their next generation networks.

That is not to say that all IP networks are “the public Internet,” or that all business models using IP are equivalent. They are not.

But the moral outrage about loosely-coupled networks is more than a bit wrong. Everyone now agrees that this is the way software gets written and that this is the way modern networks operate. The actual ownership of applications and services will vary (some tightly coupled, but most only loosely coupled).

But loose coupling (“over the top” apps) is the way we all have decided modern networks will work. That is not to say, as some once did around the turn of the century, that “bandwidth wants to be free.” That is not to argue the importance of maintaining viable access networks, or the legitimate challenges that have to be faced as massive changes occur in ISP revenue sources.

But the moral outrage really is misplaced. The layered model, by definition, presupposes separation of the application and other layers, including physical and transport layers. It therefore is not surprising at all that new revenue models and business categories now exist, and that such businesses exist without the “permission” of participants working at other layers.

The emergence of loosely coupled networks is profoundly disturbing for legacy access providers, to be sure, even if all service providers now accept such models as the foundation of their own next generation networks.

But any sense of moral outrage or entitlement is wrong and misplaced. Without question, we will need viable and profitable ISPs to support the Internet ecosystem. And video applications do pose issues for ISPs that are very complicated and challenging in a loosely coupled framework.

But that’s the nature of the networks we all have chosen to build and use. In that sense, and without diminishing the legitimate need for strong, financially viable ISP businesses, moral outrage probably is not helpful.

This is the communications world we all have chosen to live in, and some would argue it is a good model. The magnitude of transition issues for access providers should not be underestimated. But in a loosely coupled world, application providers create value, they do not steal it.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, March 2, 2013

Is 3rd Place the Best any Smart Phone Provider Now Can Hope For?

Whether aiming for third place in any competition is a good thing, or a bad thing, depends on perspective. For the acknowledged "best" competitor in any endeavor, third place is a defeat. For an up and coming new competitor that never has won at that level, third is a big win.

In the smart phone business, it appears that "third" place in sales volume or market share is about the best any contestant other than Apple or Samsung now can aspire to. That is not to say that state of affairs is permanent.

But it might now be fair to say many observers seriously doubt any of the "other" contenders have a realistic shot at anything other than third place. That might not be such a "bad" thing for lots of entrepreneurs, though.

With a different cost structure, niche markets, specialized products or method of delivery, plus retail price, lots of competitors "too small to matter" can make a living in many businesses. That has been true in the communications business for a few decades, at least.

In other words, if you want to be a whale, only a few can succeed. If being something else works, lots of space exists in most communication markets. The scale will be different. So will the gross revenue and profit margin. But those niches always exist.

Specialists serving small business segments, premises-based products such as business phone systems, repair, refurbishing, language populations, migrants, prepaid and other niches provide examples.

That is not to say the niches are permanently defensible. If the biggest providers decide they need to be in the businesses specialists occupy, and if the "whales" can figure out a way to sell at a profit (one reason whales do not pursue some lines of business or customer segments is that they cannot do so profitably), then other contestants can find themselves squeezed out of the business.

Each business is different, but the "rule of three" process is likely at work in most parts of the communications business. By that rule of thumb, one should expect to see only three leading contestants in any market.

Some might also suggest that in most markets, market share is unevenly shared by those three competitors. It would not be unusual to expect the share of the lead contestant to be twice that of the number two provider, and for the share held by the number two provider to be twice that of the number three provider, as a general rule.

For contestants in the tier one part of the access provider business, and the smart phone business, the rule of three will be an uncomfortable reality for many. but that isn't the game most entities in the communications business are playing, in any case.

In the smart phone business, it appears that "third" place in sales volume or market share is about the best any contestant other than Apple or Samsung now can aspire to. That is not to say that state of affairs is permanent.

But it might now be fair to say many observers seriously doubt any of the "other" contenders have a realistic shot at anything other than third place. That might not be such a "bad" thing for lots of entrepreneurs, though.

With a different cost structure, niche markets, specialized products or method of delivery, plus retail price, lots of competitors "too small to matter" can make a living in many businesses. That has been true in the communications business for a few decades, at least.

In other words, if you want to be a whale, only a few can succeed. If being something else works, lots of space exists in most communication markets. The scale will be different. So will the gross revenue and profit margin. But those niches always exist.

Specialists serving small business segments, premises-based products such as business phone systems, repair, refurbishing, language populations, migrants, prepaid and other niches provide examples.

That is not to say the niches are permanently defensible. If the biggest providers decide they need to be in the businesses specialists occupy, and if the "whales" can figure out a way to sell at a profit (one reason whales do not pursue some lines of business or customer segments is that they cannot do so profitably), then other contestants can find themselves squeezed out of the business.

Each business is different, but the "rule of three" process is likely at work in most parts of the communications business. By that rule of thumb, one should expect to see only three leading contestants in any market.

Some might also suggest that in most markets, market share is unevenly shared by those three competitors. It would not be unusual to expect the share of the lead contestant to be twice that of the number two provider, and for the share held by the number two provider to be twice that of the number three provider, as a general rule.

For contestants in the tier one part of the access provider business, and the smart phone business, the rule of three will be an uncomfortable reality for many. but that isn't the game most entities in the communications business are playing, in any case.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, February 28, 2013

Pandora on Mobile Illustrates Service Provider Bandwidth Paradox

Pandora says it is introducing a 40-hour-per-month limit on free mobile listening for its users, something that Pandora says will "affect less than four percent" of its total monthly active listeners. The average listener spends approximately 20 hours listening to Pandora across all devices in any given month.

The direct issue for Pandora is licensing fees. The key issue for access providers is more complicated. By definition, "interesting and valuable apps" are the reason people want to use the Internet. So apps create the demand for Internet access services, especially broadband access.

But with the advent of video as the dominant media type affecting global Internet transmission requirements, access revenue and profit margin are an obvious key issue for access providers, who argue they are not being compensated properly for the value of their access and transmission facilities.

It might be correct to say that access providers worry they will not be fairly compensated in the future. By most estimates, tier one access providers are making healthy profit margins on access services. Smaller providers have a much-bigger problem.

The bigger issue really seems to be application revenue, particularly the issue of whether application providers, especially those providing lots of video, might in the future also pay some sort of "access fee."

That would be a major switch from the traditional one-sided business model where retail end users paid for the full price for use of the network. In the proposed two-sided model, access providers would be paid both by end users and third party business partners, as is the case in much of the media and content business (cable TV subscriptions, for example, where revenue comes largely from end user "access" with significant "program network carriage fees" and some "advertising" revenue as well).

The paradox for an access provider is that Internet apps both create the business opportunity and represent a major cost driver. That obvious tension might not, by itself, be too big a challenge. The bigger problem really is that legacy revenues that underpin the business are going away.

In that sense, it is not so much that Pandora or YouTube are breaking the business model, but rather than the shrinking voice and messaging businesses are forcing service providers to recover most of their costs from Internet access services.

In that sense, it is not the "Internet apps" that are the problem. It is the declining revenue from other major sources.

To be sure, some might say the additional problem is that the past value chain is being disrupted. In the past, the "access" was embedded in the "application" provided by a service provider. In other words, voice was the app the customer wanted, and the cost of network access was embedded in the retail cost of using voice.

These days, "voice" increasingly is a separate app from "access." But that might just be another way of saying the real problem for access providers is the legacy revenue disappearing, not the mismatch of value and revenue earned by participants in the Internet value chain.

Entertainment video is helpful, but actual profit margins in video entertainment have fallen dramatically, by perhaps 50 percent over the last decade or so.

Pandora says per-track royalty rates have increased more than 25 percent over the last three years, including nine percent in 2013 alone and are scheduled to increase an additional 16 percent over the next two years. So Pandora has to cover the costs.

Pandora notes that users can listen for free for as many hours as desired on desktop and laptop computers; pay $0.99 for unlimited listening on mobiles for any month when usage exceeds the limit; , or subscribe to "Pandora One" for unlimited listening and no advertising.

The direct issue for Pandora is licensing fees. The key issue for access providers is more complicated. By definition, "interesting and valuable apps" are the reason people want to use the Internet. So apps create the demand for Internet access services, especially broadband access.

But with the advent of video as the dominant media type affecting global Internet transmission requirements, access revenue and profit margin are an obvious key issue for access providers, who argue they are not being compensated properly for the value of their access and transmission facilities.

It might be correct to say that access providers worry they will not be fairly compensated in the future. By most estimates, tier one access providers are making healthy profit margins on access services. Smaller providers have a much-bigger problem.

The bigger issue really seems to be application revenue, particularly the issue of whether application providers, especially those providing lots of video, might in the future also pay some sort of "access fee."

That would be a major switch from the traditional one-sided business model where retail end users paid for the full price for use of the network. In the proposed two-sided model, access providers would be paid both by end users and third party business partners, as is the case in much of the media and content business (cable TV subscriptions, for example, where revenue comes largely from end user "access" with significant "program network carriage fees" and some "advertising" revenue as well).

The paradox for an access provider is that Internet apps both create the business opportunity and represent a major cost driver. That obvious tension might not, by itself, be too big a challenge. The bigger problem really is that legacy revenues that underpin the business are going away.

In that sense, it is not so much that Pandora or YouTube are breaking the business model, but rather than the shrinking voice and messaging businesses are forcing service providers to recover most of their costs from Internet access services.

In that sense, it is not the "Internet apps" that are the problem. It is the declining revenue from other major sources.

To be sure, some might say the additional problem is that the past value chain is being disrupted. In the past, the "access" was embedded in the "application" provided by a service provider. In other words, voice was the app the customer wanted, and the cost of network access was embedded in the retail cost of using voice.

These days, "voice" increasingly is a separate app from "access." But that might just be another way of saying the real problem for access providers is the legacy revenue disappearing, not the mismatch of value and revenue earned by participants in the Internet value chain.

Entertainment video is helpful, but actual profit margins in video entertainment have fallen dramatically, by perhaps 50 percent over the last decade or so.

Pandora says per-track royalty rates have increased more than 25 percent over the last three years, including nine percent in 2013 alone and are scheduled to increase an additional 16 percent over the next two years. So Pandora has to cover the costs.

Pandora notes that users can listen for free for as many hours as desired on desktop and laptop computers; pay $0.99 for unlimited listening on mobiles for any month when usage exceeds the limit; , or subscribe to "Pandora One" for unlimited listening and no advertising.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

We Used to "Google Ourselves," but Now We Will Want to Know Whether We are in the Weights

It was inevitable: perhaps we used to "Google ourselves." Now, with language models doing the heavy lifting, we want to know wheth...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Financial analysts typically express concern when any firm’s customer base is too concentrated. Consider that, In 2024, CoreWeave’s top two ...

{kind=link}