Visa Europe surveyed 4,200 people in four different European nations and found that 57 percent of iPhone users among the respondents said they'd "definitely" or "probably" use Visa's mobile payments platform on their iPhone if they could.

Some 41 percent of all respondents reported they would likely use near field communications and mobile payments if possible.

Visa has drawn the logical inference: that European Apple iPhone users should be targeted. How, you might ask, since the iPhone does not yet support NFC? There always are work-around processes in the mobile payment business.

One way is to outfit a standard iPhone with an NFC-supporting dongle, much as Square turns an iPhone into a payment terminal using a dongle.

Visa appears to be readying a test using the Wireless Dynamics iCarte. Retailer point of sale terrminals also will need to be outfitted for NFC, but also can use a dongle approach.

Some of us have mused that Apple could be a huge force in the mobile payments business if it wanted to "transform" payments the way it routinely expects to transform other businesses. The barrier, of course, is that Apple prefers to transform consumer industries that are based on use of devices.

Mobile payments does not appear to offer much upside in that regard, as Apple already leads the smart phone business. That means mobile payments is just a feature, not the foundation for a whole new class of consumer devices.

But Visa already seems eager to test a theory about the value of an app using the iPhone as a hardware platform. Visa does not lack for clarity about what it means for its own business.

Wednesday, February 1, 2012

Visa Europe to Test Dongle-Based iPhone NFC Mobile :Payments

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Mobiles Change Shopping

Mobile devices are changing the shopping experience, according to a new study by the Pew Internet & American Life Project.

Mobile devices are changing the shopping experience, according to a new study by the Pew Internet & American Life Project. About 25 percent of adult cell phone owners used their devices to look up the price of a product online while they were in a store during this past holiday season, the study found.

Also. some 38 percent of mobile phone owners used their phone to call a friend while they were in a store for advice about a purchase they were considering making.

Some 24 percent used their phone to look up reviews of a product online while they were in a store.

Overall, 52 percent of all adult cell phone owners used their phone for at least one of those reasons over the holiday shopping season, and one-third used their phone specifically for online information while inside a physical store.

There does not seem to be any good reason why behavior in other markets, including Europe and Japan, for example, should be different. Globally, it would appear, mobile devices, especially smart phones, are starting to affect in-store shopping, with huge implications for brick-and-mortar retailers and online retailers as well.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Comcast, Verizon Wireless Bundles In Bay Area, Portland, Seattle

We are about to see how well new inducements offered by Comcast and Verizon Wireless will work as a customer acquisition tool.

Consumers in the San Francisco Bay Area, Seattle and Portland, Ore. now will be eligible for a discount for buying new packages of video, fixed line voice, broadband access and wireless service.

Consumers who sign up for a bundled service plan from Comcast and for new service from Verizon Wireless are eligible to receive a prepaid Visa card worth up to $300, depending on the number of services they buy.

To take advantage of the offer, consumers need to sign up for new service from Comcast and either new service or a new contract from Verizon Wireless.

Customers can use the prepaid card on smart phones or tablets offered by Verizon, but they won't receive the card until after they have signed up for service. Comcast offers discount on Verizon Wireless

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, January 31, 2012

Wireless Customer Satisfaction Doesn't Prevent Customer Churn

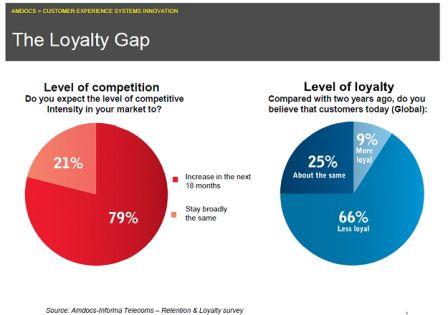

The conventional wisdom for most people, including executives at mobile service provider companies, is that there is a relatively direct relationship between "customer satisfaction" and customer churn. In other words, "happy customers" don't leave.

Two out of three (66 percent) wireless and cable TV consumers switched companies in 2011, even as their satisfaction with the services provided by those companies rose, according to Accenture.

Two out of three (66 percent) wireless and cable TV consumers switched companies in 2011, even as their satisfaction with the services provided by those companies rose, according to Accenture.

The paradox is that “customer satisfaction” does not lead to “loyalty.” Also, there are new precursors to churn, especially the growing pattern of consumers adding a second provider of a service, without dropping the original provider. That of course puts a potential full replacement provider into a relationship with a consumer.

The Accenture Global Consumer Survey asked consumers in 27 countries to evaluate 10 industries on issues ranging from service expectations and purchasing intentions to loyalty, satisfaction and switching.

Among the 10,000 consumers who responded, the proportion of those who switched companies for any reason between 2010 and 2011 rose in eight of the 10 industries included in the survey.

Wireless phone, cable and gas/electric utilities providers each experienced the greatest increase in consumer switching, moving higher by five percentage points.

According to the survey, customer switching also increased by four percent in 2011 in the wireline phone and Internet service sectors.

There is a new and apparently growing indicator of churn potential as well. In a growing percentage of cases, consumers are adding new providers, instead of switching entirely. That can disguise the danger of churn, as the original provider does not realize a new potential replacement provider also has established a relationship with a particular consumer.

“Companies are improving many of the most frustrating parts of the customer service experience, but they are facing a customer who is increasingly willing to engage multiple providers for a service and is apt to switch quickly,” said Robert Wollan, global managing director, Accenture Customer Relationship Management. “

Note the contradiction here: consumers were “more satisfied” and also “not loyal” because of that satisfaction.

Consumers reported increased satisfaction across each of 10 service characteristics evaluated. In fact, satisfaction rates on three customer service characteristics jumped by more than five percentage points from 2010.

However, only one in four consumers feels “very loyal” to his or her providers across industries, and just as many profess no loyalty at all. Furthermore, two-thirds of consumers switched providers in at least one industry in the past year due to poor customer service.

In emerging markets, these contradictions are even more pronounced. While consumers there reported greater customer satisfaction than their mature-market peers, they more often switched providers due to poor service across all industries (in some cases by a two-to-one ratio over mature markets), especially within the retail, ISP, mobile and banking industries.

It doesn't appear that is the case. Perhaps perversely, even happy customers will churn (leave a supplier for another), and at surprisingly high rates.

Two out of three (66 percent) wireless and cable TV consumers switched companies in 2011, even as their satisfaction with the services provided by those companies rose, according to Accenture.

Two out of three (66 percent) wireless and cable TV consumers switched companies in 2011, even as their satisfaction with the services provided by those companies rose, according to Accenture.The paradox is that “customer satisfaction” does not lead to “loyalty.” Also, there are new precursors to churn, especially the growing pattern of consumers adding a second provider of a service, without dropping the original provider. That of course puts a potential full replacement provider into a relationship with a consumer.

The Accenture Global Consumer Survey asked consumers in 27 countries to evaluate 10 industries on issues ranging from service expectations and purchasing intentions to loyalty, satisfaction and switching.

Among the 10,000 consumers who responded, the proportion of those who switched companies for any reason between 2010 and 2011 rose in eight of the 10 industries included in the survey.

Wireless phone, cable and gas/electric utilities providers each experienced the greatest increase in consumer switching, moving higher by five percentage points.

According to the survey, customer switching also increased by four percent in 2011 in the wireline phone and Internet service sectors.

There is a new and apparently growing indicator of churn potential as well. In a growing percentage of cases, consumers are adding new providers, instead of switching entirely. That can disguise the danger of churn, as the original provider does not realize a new potential replacement provider also has established a relationship with a particular consumer.

“Companies are improving many of the most frustrating parts of the customer service experience, but they are facing a customer who is increasingly willing to engage multiple providers for a service and is apt to switch quickly,” said Robert Wollan, global managing director, Accenture Customer Relationship Management. “

Note the contradiction here: consumers were “more satisfied” and also “not loyal” because of that satisfaction.

Consumers reported increased satisfaction across each of 10 service characteristics evaluated. In fact, satisfaction rates on three customer service characteristics jumped by more than five percentage points from 2010.

However, only one in four consumers feels “very loyal” to his or her providers across industries, and just as many profess no loyalty at all. Furthermore, two-thirds of consumers switched providers in at least one industry in the past year due to poor customer service.

In emerging markets, these contradictions are even more pronounced. While consumers there reported greater customer satisfaction than their mature-market peers, they more often switched providers due to poor service across all industries (in some cases by a two-to-one ratio over mature markets), especially within the retail, ISP, mobile and banking industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

User Experience on PCs, Tablets, Smart Phones Differs Vastly

Latency is getting to be a bigger deal for mobile user experience. Apps that load quickly on a PC take much longer to load on a smart phone or tablet, Yankee Group reports, using Keynote Systems data.

Also, according to Yankee Group analyst Carl Howe, typical users now carry as many as five different mobile devices. But each of those devices might be optimized in different ways, in terms of latency.

Load times among sites differ because in most cases, content owners are not customizing the content they deliver to the device, says Howe. The majority of the sites Keynote Systems monitored, including major online brands Craigslist and Apple, sent the same content to smart phones and tablets, for example.

Facebook, Bing, Kayak, MSN, Amazon and IMDB all sent significantly more objects and bytes to tablets than to smart phones. These sites detected the larger screens of tablets and sent them more information, says Howe.

The one company that behaves significantly differently is Google, which sent roughly 450 KBytes to smart phones while sending only about 200 KBytes to tablets.

Google chooses to add several location-based options such as “Restaurants” and “Coffee” to smart phone content but doesn’t serve up those features to tablet users, probably because many tablets don’t offer location services by default. As a result, smart phones receive more content from Google than tablets do.

Those findings are interesting for several reasons. Since different devices feature different screen sizes and input and output capabilities, get used in different ways, at different locations, at different times of day, customizing the experience makes sense.

But tailoring a user experience based on what device is used, when it used or where it is used is not so different from tailoring an experience based on what application a user wants to engage with. And that’s where legitimate concerns about unfair business advantage bump up against end user preferences.

When a user wants to watch a video, conduct a video call or play an interactive game, issues such as latency and consistency of bandwidth availability are important performance parameters.

The policy issue is whether users or service providers ought to be able to manage network experience to enhance end user experience. For such reasons, some think “best effort only” access is not optimal.

Some 21 percent of surveyed enterprise information workers are using one or more Apple products for work, Forrester Research says.

Almost half of enterprises (1000 employees or more) are issuing Macs to at least some employees and they plan a 52 percent increase in the number of Macs they issue in 2012.

Managers and executives are more than twice as likely to use Apple products, suggesting an adoption pattern where the ability to use the device is something of a “perquisite,” much as at one time the ability to use a BlackBerry was a perquisite for enterprise executives.

But younger information workers (IT staffs for example) are twice as likely to use Apple products as older ones.

Higher income workers are more likely to use Apple products as well, but there is a “younger worker” issue here. Most of the sample of 10,000 global information workers earns less than $50,000 a year, but the adoption rate of Apple products is almost 17 percent even in the bottom quartile of workers who make less than $12,000 per year.

Keep in mind, also, that the survey was global in scope, and Information workers in countries outside North America and Europe were more likely to use Apple products for work. Annual salaries also might tend to be lower in non-European and North American settings.

Where click through rates are concerned, screen size matters. Simply put, larger screens tend to get higher click through rates, and some devices tend to have higher engagement than others. Smart phone screens tend to get click throughs at about a two-percent to four-percent rate.

Larger tablet screens such as those sported by the Apple iPad or Samsung Galazy get CTRs of about nine percent. The results are generally similar across device brands.

Also, according to Yankee Group analyst Carl Howe, typical users now carry as many as five different mobile devices. But each of those devices might be optimized in different ways, in terms of latency.

Load times among sites differ because in most cases, content owners are not customizing the content they deliver to the device, says Howe. The majority of the sites Keynote Systems monitored, including major online brands Craigslist and Apple, sent the same content to smart phones and tablets, for example.

Facebook, Bing, Kayak, MSN, Amazon and IMDB all sent significantly more objects and bytes to tablets than to smart phones. These sites detected the larger screens of tablets and sent them more information, says Howe.

The one company that behaves significantly differently is Google, which sent roughly 450 KBytes to smart phones while sending only about 200 KBytes to tablets.

Google chooses to add several location-based options such as “Restaurants” and “Coffee” to smart phone content but doesn’t serve up those features to tablet users, probably because many tablets don’t offer location services by default. As a result, smart phones receive more content from Google than tablets do.

Those findings are interesting for several reasons. Since different devices feature different screen sizes and input and output capabilities, get used in different ways, at different locations, at different times of day, customizing the experience makes sense.

But tailoring a user experience based on what device is used, when it used or where it is used is not so different from tailoring an experience based on what application a user wants to engage with. And that’s where legitimate concerns about unfair business advantage bump up against end user preferences.

When a user wants to watch a video, conduct a video call or play an interactive game, issues such as latency and consistency of bandwidth availability are important performance parameters.

The policy issue is whether users or service providers ought to be able to manage network experience to enhance end user experience. For such reasons, some think “best effort only” access is not optimal.

Some 21 percent of surveyed enterprise information workers are using one or more Apple products for work, Forrester Research says.

Almost half of enterprises (1000 employees or more) are issuing Macs to at least some employees and they plan a 52 percent increase in the number of Macs they issue in 2012.

Managers and executives are more than twice as likely to use Apple products, suggesting an adoption pattern where the ability to use the device is something of a “perquisite,” much as at one time the ability to use a BlackBerry was a perquisite for enterprise executives.

But younger information workers (IT staffs for example) are twice as likely to use Apple products as older ones.

Higher income workers are more likely to use Apple products as well, but there is a “younger worker” issue here. Most of the sample of 10,000 global information workers earns less than $50,000 a year, but the adoption rate of Apple products is almost 17 percent even in the bottom quartile of workers who make less than $12,000 per year.

Keep in mind, also, that the survey was global in scope, and Information workers in countries outside North America and Europe were more likely to use Apple products for work. Annual salaries also might tend to be lower in non-European and North American settings.

Where click through rates are concerned, screen size matters. Simply put, larger screens tend to get higher click through rates, and some devices tend to have higher engagement than others. Smart phone screens tend to get click throughs at about a two-percent to four-percent rate.

Larger tablet screens such as those sported by the Apple iPad or Samsung Galazy get CTRs of about nine percent. The results are generally similar across device brands.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Telecom Finally Has its "Fashion" Moment: But Apple Owns It

When Apple set out to revolutionize the phone handset business, it might not have foreseen precisely how much change it would cause.

Not the least of the changes is a shift of power within the retail business, as mobile service providers for the first time have lost the ability to dictate what devices users can use, and what features devices should provide.

On the other hand, some of us have argued that the key marketing problem for any telecom service provider always has been that nobody really "loves" their service provider, and identifies with the service, in the same way that people routinely identify with their autos, clothing, perfumes, shoes, hobbies or sports.

What telecom has needed, in that vein, is a way to create, for consumers, that high emotional bond.

Apple's iPhones have become that bond, for the first time in the industry's history.

Of course, there is a bit of a downside: the emotional bond is with the device, created by Apple, still not the service. But the change is significant. The Apple iPhone now personifies the value of the communications connection. But other changes, for handset suppliers, would seem to be coming.

The reason is that handset profitability, more than anything else, now is shaping the global smart phone business, one might argue.Globally, Apple and Samsung have, over the last 12 months, surged to the top of the charts in terms of smart phone sales volume, according to Strategy Analytics.

In the past, the “smart phone” category has not been significant, as all devices were feature phones or basic phones.

As the market begins to shift to a smart phone buyer pattern, differences in firm strategy and execution have lead to a rapid change in market leadership.

Global smart phone shipments grew 54 percent annually to reach a record 155 million units in the fourth quarter of 2011, according to Alex Spektor, Strategy Analytics associate director. That apparently has proven to be a decisive change.

In the past, Nokia has been the global share leader, but Nokia has not been able to translate that prior success into smart phone success, where Apple has changed the game and Samsung apparently has been able to keep pace.

Apple overtook Samsung to become the world’s largest smartphone vendor by volume with 24 percent market share. Apple’s global smartphone shipments surged 128 percent annually to 37.0 million units, as distribution of the iPhone family expanded across numerous countries, dozens of operators and multiple price points.”

Apple took the top spot for share on a quarterly basis, but Samsung became the market leader in annual terms for the first time with 20 percent global share during 2011. With global smartphone shipments nearing half a billion units in 2011, Samsung is now well positioned alongside Apple in a two-horse race at the forefront of one of the world’s largest and most valuable consumer electronics markets, Strategy Analytics says.

In contrast, Nokia’s smart phone market share was cut in half from 2011 to 2011, dropping from 33 percent in 2010 to 16 percent in 2011.

That is one reason there has been so much focus on the Nokia partnership with Microsoft, as many would argue the Windows Mobile operating system represents the best shot Nokia will have to avoid collapse.

The other observation of note would be that profitability might now be emerging as the key differentiator, even though design and consumer demand clearly are driving the market overall.

Samsung’s most-recent quarterly earnings also set records. Samsung Electronics Co declared $4.7 billion in quarterly operating profit. jumping 76 percent year over year.

Between them, Apple and Samsung earned fully 81 percent of all profits in the mobile handset business.

As the market begins to shift to a smart phone buyer pattern, differences in firm strategy and execution have lead to a rapid change in market leadership.

Global smart phone shipments grew 54 percent annually to reach a record 155 million units in the fourth quarter of 2011, according to Alex Spektor, Strategy Analytics associate director. That apparently has proven to be a decisive change.

In the past, Nokia has been the global share leader, but Nokia has not been able to translate that prior success into smart phone success, where Apple has changed the game and Samsung apparently has been able to keep pace.

Apple overtook Samsung to become the world’s largest smartphone vendor by volume with 24 percent market share. Apple’s global smartphone shipments surged 128 percent annually to 37.0 million units, as distribution of the iPhone family expanded across numerous countries, dozens of operators and multiple price points.”

Apple took the top spot for share on a quarterly basis, but Samsung became the market leader in annual terms for the first time with 20 percent global share during 2011. With global smartphone shipments nearing half a billion units in 2011, Samsung is now well positioned alongside Apple in a two-horse race at the forefront of one of the world’s largest and most valuable consumer electronics markets, Strategy Analytics says.

In contrast, Nokia’s smart phone market share was cut in half from 2011 to 2011, dropping from 33 percent in 2010 to 16 percent in 2011.

That is one reason there has been so much focus on the Nokia partnership with Microsoft, as many would argue the Windows Mobile operating system represents the best shot Nokia will have to avoid collapse.

The other observation of note would be that profitability might now be emerging as the key differentiator, even though design and consumer demand clearly are driving the market overall.

Samsung’s most-recent quarterly earnings also set records. Samsung Electronics Co declared $4.7 billion in quarterly operating profit. jumping 76 percent year over year.

Between them, Apple and Samsung earned fully 81 percent of all profits in the mobile handset business.

Apple in the fourth quarter of 2011 shipped 37 million smart phones worldwide, up 117 percent from 17 million in the second quarter. This represented the strongest sequential quarterly growth among the top-five smart phone brands, according to IHS ISuppli.

“Samsung advanced in 2011 because of its strategy of offering a complete line of smartphone products, spanning a variety of price points, features and operating systems,” says Wayne Lam, IHS senior analyst.

On the other hand, the market share battle between Apple and Samsung reflects the competition between the two leading smartphone operating systems and ecosystems: Apple's iOS and Google's Android, says Lam.

“The relatively small growth of Sony Ericsson and Motorola may indicate that the Android smart phone market is becoming too crowded as the various licensees compete for limited consumer mind share and shelf space,” Lam says.

“Samsung advanced in 2011 because of its strategy of offering a complete line of smartphone products, spanning a variety of price points, features and operating systems,” says Wayne Lam, IHS senior analyst.

On the other hand, the market share battle between Apple and Samsung reflects the competition between the two leading smartphone operating systems and ecosystems: Apple's iOS and Google's Android, says Lam.

“The relatively small growth of Sony Ericsson and Motorola may indicate that the Android smart phone market is becoming too crowded as the various licensees compete for limited consumer mind share and shelf space,” Lam says.

Aside from the obvious potential implication that there simply is not room in the global smart phone business for more than a few providers, the value of particular handsets, and their suppliers, seems destined to grow.

People increasingly want, not so much the ability to use mobile communications, but iconic devices that use the networks. A hundred years ago, that was not the case. People just wanted the service.

These days, the service is a feature of what has become a "fashion" item; a statement about values and lifestyle. At long last, the industry has managed to create high emotional involvement. As it turns out, though, the involvement is with the iconic devices, not the services.

Tablets appear to be the next connected device to make that leap.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Global Telco "Meltdown" Coming? Or Just Normal Product Substitution?

BSkyB has been a major player in the United Kingdom subscription TV market for decades. But BSkyB faces a maturation of its base business, as do all other video entertainment and communications providers in Europe, North America and elsewhere.

“The company made a number of announcements which confirm that, beyond the near term slowdown, structural issues are looming,” Bernstein analyst Claudio Aspesi argues.

“While we believe the pay TV business is inherently more defensive than advertising-funded ones, the depth and length of the downturn in the U.K. economy are still unknown: any significant changes to our forecasts for the UK TV ad market could be large enough to change the outlook for the stock.”

Structural change is another way of saying that saturated markets and greater amounts of competition are eroding the growth potential for virtually all big communications or entertainment businesses.

“The company made a number of announcements which confirm that, beyond the near term slowdown, structural issues are looming,” Bernstein analyst Claudio Aspesi argues.

“While we believe the pay TV business is inherently more defensive than advertising-funded ones, the depth and length of the downturn in the U.K. economy are still unknown: any significant changes to our forecasts for the UK TV ad market could be large enough to change the outlook for the stock.”

Structural change is another way of saying that saturated markets and greater amounts of competition are eroding the growth potential for virtually all big communications or entertainment businesses.

According to analysts at Ovum, global service provider revenues grew seven percent in 2011. On a global basis, service provider revenues will grow at a compound annual growth rate of 2.9 percent over the 2010-2017 period, down from the historic CAGR of 6.3 percent achieved in 2004 to 2010, according to analysts at Ovum.

The Ovum forecast shows the deceleration of revenue, even despite newer products such as mobile broadband.

A key strategic issue is whether service providers can grow new lines of business fast enough to offset lost revenues from their legacy businesses.

One doesn’t have to agree with all elements of the analysis to sense the danger. In some markets where the leading edge of the trend seems to be emerging (Europe), there is a palpable sense that voice and messaging revenues are about to become over the top apps, with an implied hit to the dominant provider revenue streams.

“I strongly believe the business model for voice and messaging is about to go into reverse,” says Geddes. “The value is going to drain out of minutes and messages charged to users.”

Many would agree with the fundamental challenges, without necessarily agreeing on the timing and magnitude of the revenue changes. In the near term, most also would agree that commercial services are the important new revenue driver for cable companies, while mobile broadband drives telco growth.

At some point, even those growth drivers will slow, which is why telco executives are working on new initiatives in cloud computing, machine-to-machine services and mobile commerce. The key issue is whether those, or other services not yet on the horizon, are big enough to offset the huge potential telco losses in voice and messaging and video losses for cable operators.

The Ovum forecast shows the deceleration of revenue, even despite newer products such as mobile broadband.

A key strategic issue is whether service providers can grow new lines of business fast enough to offset lost revenues from their legacy businesses.

Most executives are familiar with the notion of a “product life cycle.” What might be a more provocative idea is the notion that collectively, the global communications industry might be entering a period where communications itself hits something of a industry life cycle peak.

“The telco voice and messaging business is on the verge of going into meltdown,” muses industry consultant Martin Geddes. By that line of thinking, so much revenue and profit is about to be drained away that the replacement revenue streams (based largely on broadband access for the near term) cannot prevent some significant shrinkage of the overall business.One doesn’t have to agree with all elements of the analysis to sense the danger. In some markets where the leading edge of the trend seems to be emerging (Europe), there is a palpable sense that voice and messaging revenues are about to become over the top apps, with an implied hit to the dominant provider revenue streams.

“I strongly believe the business model for voice and messaging is about to go into reverse,” says Geddes. “The value is going to drain out of minutes and messages charged to users.”

Many would agree with the fundamental challenges, without necessarily agreeing on the timing and magnitude of the revenue changes. In the near term, most also would agree that commercial services are the important new revenue driver for cable companies, while mobile broadband drives telco growth.

At some point, even those growth drivers will slow, which is why telco executives are working on new initiatives in cloud computing, machine-to-machine services and mobile commerce. The key issue is whether those, or other services not yet on the horizon, are big enough to offset the huge potential telco losses in voice and messaging and video losses for cable operators.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

Net AI Sustainability Footprint Might be Lower, Even if Data Center Footprint is Higher

Nobody knows yet whether higher energy consumption to support artificial intelligence compute operations will ultimately be offset by lower ...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...

{kind=link}