The possibility that Sprint is launching its own mobile wallet platform, and might, as part of that effort, have to displace Google Wallet on its devices, will add yet one more provider to a chaotic mobile wallet environment. Neither Google Wallet nor Isis, for example, have gotten significant traction yet, nor, in truth, should have that been expected.

Both Isis and Google Wallet require creation of a huge new infrastructure of near field communications point of sale terminals and end user devices, plus new end user behaviors and a clear value proposition. Those would be difficult under the best of circumstances.

Google will do what it always does: keep working on the next version. It is far too early to declare any long-term winners in the NFC mobile wallet business. Consumer adoption of important new technologies can take some time.

Products such as tablets can reach significant penetration rather quickly because the rest of the infrastructure, including widespread Wi-Fi, apps, end user behavior, business models, quality broadband (at least for purposes of supporting video apps, a key tablet app) and even familiarity with the touch interface are established.

Near field communications has almost none of the infrastructure requirements well established. For that reason, many of us would caution that patience is needed. It might take as much as a decade before there is significant penetration.

ATM card adoption provides one example, where "decades" is a reasonable way of describing adoption of some new technologies, even those that arguably are quite useful.

“Mobile proximity payments will remain in infancy for at least five years,” said Jim Van Dyke, Javelin Research president. In other words, payment systems based on near field communications, and others, might take that long to begin getting serious traction.

Saturday, June 9, 2012

Slow Traction for Google Wallet Isn't Surprising

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, June 8, 2012

Facebook App Center Isn't a Store, It's a Discovery or Search Tool

Facebook's new "App Center" might sound like an app store, but it is not. Rather, the App Center is a way to encourage people to use Facebook-affiliated mobile apps, by helping them find useful and entertaining apps.

Facebook's new "App Center" might sound like an app store, but it is not. Rather, the App Center is a way to encourage people to use Facebook-affiliated mobile apps, by helping them find useful and entertaining apps. It's partly a discovery or search tool, partly an incentive for developers to work with Facebook and hence part of Facebook's effort to maintain its platform relevance.

It also is one example of how device and application providers now are orienting their businesses around a “mobile first” strategy.

Facebook says there are more than 4,500 separate applications that integrate with Facebook.

The company also took the opportunity to highlight the role it has played in driving mobile application sales. It has released statistics indicating that Facebook sent users to the Apple App Store 83 million times in May alone, and sent iOS users into installed applications 134 million times during the same month.

The App Center is rolling out immediately in the United States and will be made available to users in other countries over the next few weeks. It is intended to replace the Facebook website’s existing Apps and Games interface.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Will Google, Apple, PayPal Ever Want to be Banks?

Will Google, Apple, PayPal and others ever decide there is a reason to become "banks?" The question might seem far fetched, except that once application and device firms decide payments and loyalty are businesses with direct implications for their existing businesses, it isn't so clear what other functions associated with "banks" might then seem reasonable as well.

Rogers Communications in Canada already has applied to become a formal bank. To be sure, that appears to be primarily for the purpose of providing credit, payment and charge card services. In one sense, the move is similar to any other large retail brand creating a branded charge card.

"We have no plans to become a full-service deposit-taking financial institution," Rogers Public Affairs Manager Carly Suppa said. "The license, if granted, would give us the flexibility to pursue a niche credit card opportunity to our customers should this make sense at a future date."

"People have already slowed their use of cash and checks in favor of credit and debit cards. Within five years, half of today’s smart phone users will be using their phones and mobile wallets as their preferred method for payments," argues Peter Olynick, Carlisle & Gallagher's Card & Payments Practice leader.

Keep in mind, he isn't saying Google, Apple, PayPal and many others immediately threaten the core banking function, just the parts of their business associated with payment operations.

A survey of 605 U.S. consumers found high receptivity, at least in principle, to use of mobile wallets for loyalty purposes. The same survey also found consumers conceptually also willing to use entities such as PayPal for core banking functions as well.

Once can be skeptical, without being dismissive, about the degree to which such sentiments might eventually become actual behavior. One might remain skeptical that the core banking function actually is attractive for application and device suppliers, or mobile service providers.

But in many African markets, mobile service providers have already in droves become authorized payment providers. You might not consider that banking so much as money transfer. But bill paying has become a more-important banking feature, at the very least, and money transfer is bleeding over broadly into bill paying, in Africa.

What seems unlikely or improbable today might not always seem outlandish. But a reasonable person might still bet against the likes of Google and Apple becoming banks in the common sense of the term, even if payments will be contested terrain.

Rogers Communications in Canada already has applied to become a formal bank. To be sure, that appears to be primarily for the purpose of providing credit, payment and charge card services. In one sense, the move is similar to any other large retail brand creating a branded charge card.

"We have no plans to become a full-service deposit-taking financial institution," Rogers Public Affairs Manager Carly Suppa said. "The license, if granted, would give us the flexibility to pursue a niche credit card opportunity to our customers should this make sense at a future date."

In other words, Rogers doesn't want to become a full-fledged retail bank. But becoming a credit card issuer does set Rogers up for a smooth transition to becoming a mobile payments provider in the future.

Credit cards present a distinct opportunity for Rogers to expand its reach, as the media, cable and wireless giant also owns the Toronto Blue Jays and has direct relationships with millions of customers, including many who pay bills using credit or direct-deposit accounts. So there is an incremental opportunity to capture some of the current transaction revenue, at the very least.

Beyond that, analysts say the company can build a broader card business by leveraging those relationships to market its brand of cards, especially by reaching out to customers who have good credit standing in its database. That would create a new revenue stream for the broader number of retail transactions for which its customers use credit cards.

"People have already slowed their use of cash and checks in favor of credit and debit cards. Within five years, half of today’s smart phone users will be using their phones and mobile wallets as their preferred method for payments," argues Peter Olynick, Carlisle & Gallagher's Card & Payments Practice leader.

Keep in mind, he isn't saying Google, Apple, PayPal and many others immediately threaten the core banking function, just the parts of their business associated with payment operations.

A survey of 605 U.S. consumers found high receptivity, at least in principle, to use of mobile wallets for loyalty purposes. The same survey also found consumers conceptually also willing to use entities such as PayPal for core banking functions as well.

Once can be skeptical, without being dismissive, about the degree to which such sentiments might eventually become actual behavior. One might remain skeptical that the core banking function actually is attractive for application and device suppliers, or mobile service providers.

But in many African markets, mobile service providers have already in droves become authorized payment providers. You might not consider that banking so much as money transfer. But bill paying has become a more-important banking feature, at the very least, and money transfer is bleeding over broadly into bill paying, in Africa.

What seems unlikely or improbable today might not always seem outlandish. But a reasonable person might still bet against the likes of Google and Apple becoming banks in the common sense of the term, even if payments will be contested terrain.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, June 7, 2012

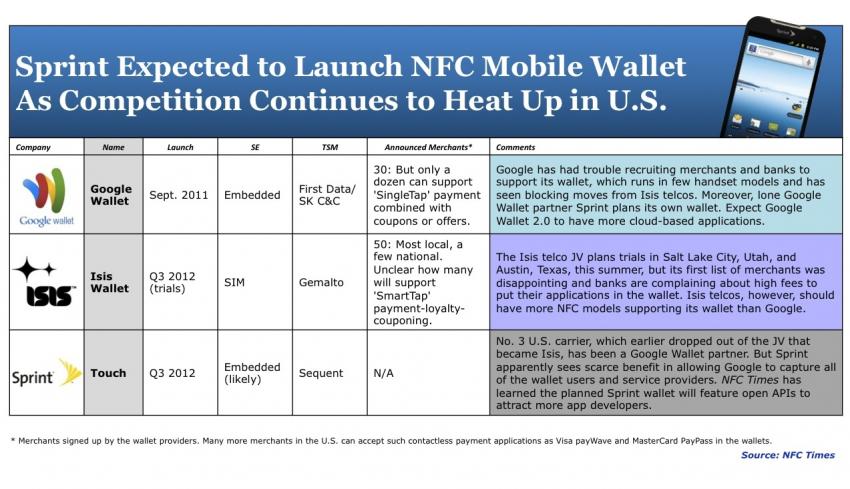

Sprint Plans to Launch own NFC Mobile Wallet?

Sprint is planning to launch its own NFC mobile wallet as early as this summer, NFC Times reports. Sprint earlier had been the only U.S mobile service provider to support Google Wallet. The obvious question is whether this means Sprint will drop support for Google Wallet.

Sprint is planning to launch its own NFC mobile wallet as early as this summer, NFC Times reports. Sprint earlier had been the only U.S mobile service provider to support Google Wallet. The obvious question is whether this means Sprint will drop support for Google Wallet.Sprint apparently sees advantages in rolling out its own wallet, which according to the sources is named “Touch.” With a wallet, Sprint could build relationships with banks and other service providers.

“The limitation isn’t the wallet; the limitation is the secure element,” said a source at Sprint, who added the Sprint wallet offers a “legitimate alternative to Isis.” That rather suggests Sprint has to make a choice between its own offering and Google Wallet, as a wallet apparently needs control of the secure element used to authenticate users and credentials.

Some of you will want to shake your heads at the growing number of wallet platforms, not to mention payment systems. Market fragmentation always is quite high at the start of any new business expected to be sizable.

The emergence of more competitors "validates" the market, executives like to say. That might be true, but fragmentation also will slow adoption, to the extent that users have to lock into devices, service providers or exclusive apps.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

What Happens to Google Revenue as Apple Dumps Google Maps?

Most observers would probably guess that if Apple represents about 40 percent of Google mobile search ad revenue, and Apple stops offering Google Maps in favor of its own map application, that Google revenue will suffer.

Most observers would probably guess that if Apple represents about 40 percent of Google mobile search ad revenue, and Apple stops offering Google Maps in favor of its own map application, that Google revenue will suffer.But Piper Jaffray's Gene Munster predicts that Apple's decision to abandon Google Maps shouldn't have any "material impact" on the revenue Google gets from iOS.

Munster estimates that Google will generate about $4.5 billion in gross mobile revenue in 2012, the lion's share ($4 billion) from search ads and the rest ($500 million) from display.

He believes that iOS is likely to remain the biggest or close to the biggest source of that revenue, generating roughly $1.6 billion. Assuming Google keeps half (after subtracting acquisition costs), iOS would generate about two percent of Google's total revenue in 2012.

You might wonder how that could possibly be. Munster assumes Google Maps still will be available in the Apple app store, and that iOS device users will be able to figure out how to keep using it. Munster says Apple represents about two percent of Google's net revenue overall.

Google might hope Munster is right, but is acting as though the loss could be more significant. Google's recent addition of 3D features to Google Maps probably indicates Google's belief that Apple will try and use the 3D feature to differentiate from Google Maps.

Mobile ads associated with maps or locations are estimated to account for about 25 percent of the roughly $2.5 billion spent on mobile ads in 2012, according to Opus Research, up from 10 percent in 2010. That is reason enough for a battle over map applications.

The reason maps get so much advertising is that geo-location is a fairly serious indicator of purchase intent when a retailer is searched for, within a map app. That obviously has implications if you believe location-based advertising and offers are a big business opportunity.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Global Mobile Advertising Market: $5.3 Billion in 2011

Mobile advertising reached $5.3 billion (€3.8 billion) in 2011. You might call that a good start, but still quite a smallish business, by tier one mobile service provider standards. The reason is simply that an entity booking scores of billions worth of revenue each year would need a market opportunity far bigger than that to become "really interesting."

But mobile advertising is a new and growing business, so most observers think the market eventually will grow to a size that is truly significant for mobile service providers.

Of current revenue, Europe represents 25.9 percent; North America 31.4 percent; Latin America 3.5 percent; Asia-Pacific 35.9 percent; Middle East and Africa 3.2 percent, according to the Interactive Advertising Bureau.

Obviously, mobile service providers in Europe, North America and parts of Asia are likely to reach a "critical mass" of revenue sooner than other regions.

But mobile advertising is a new and growing business, so most observers think the market eventually will grow to a size that is truly significant for mobile service providers.

Of current revenue, Europe represents 25.9 percent; North America 31.4 percent; Latin America 3.5 percent; Asia-Pacific 35.9 percent; Middle East and Africa 3.2 percent, according to the Interactive Advertising Bureau.

Obviously, mobile service providers in Europe, North America and parts of Asia are likely to reach a "critical mass" of revenue sooner than other regions.

2011: Mobile ad spend in $million

| Display | Search | Messaging | Total | |

| Europe | 367 | 900 | 114 | 1,380 |

| North America | 572 | 811 | 295 | 1,677 |

| Latin America | 31 | 74 | 83 | 188 |

| Asia-Pacific | 491 | 1,384 | 41 | 1,916 |

| Middle East & Africa | 44 | 124 | 4 | 172 |

| Global | 1,504 | 3,292 | 536 | 5,333 |

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

What Will Apple Do After Every Sizable Mobile Service Provider Sells the iPhone?

Apple will face a common supplier issue, namely product saturation, at some point, after every significant (in terms of market share) mobile service provider, in each market, sells the iPhone. Except for T-Mobile, all of the largest four U.S. carriers already sell the iPhone, and regional or prepaid carriers also are starting to get the device.

So Apple will do what any supplier normally does, in such situations. Refresh products so that existing buyers want to buy again. Apple also will continue wooing customers who now buy other devices to buy its own.

As it did with the iPod family of products, Apple will flesh out devices in a range of price segments, to capture more of the addressable market. Apple also will try to get existing and potential buyers to spend for other products Apple makes, such as tablets.

So Apple will do what any supplier normally does, in such situations. Refresh products so that existing buyers want to buy again. Apple also will continue wooing customers who now buy other devices to buy its own.

As it did with the iPod family of products, Apple will flesh out devices in a range of price segments, to capture more of the addressable market. Apple also will try to get existing and potential buyers to spend for other products Apple makes, such as tablets.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...