New Verizon Wireless shared data plans are designed to encourage uptake of connected tablets and smart phones. The impact on a single-user smart phone account probably will be "revenue neutral" for both Verizon Wireless and any single smart phone account.

New Verizon Wireless shared data plans are designed to encourage uptake of connected tablets and smart phones. The impact on a single-user smart phone account probably will be "revenue neutral" for both Verizon Wireless and any single smart phone account.And that was intentional, obviously. Ideally, Verizon Wireless would find the new plans provide incentives for group accounts to add smart phone and tablet devices, while not cannibalizing the single-user accounts.

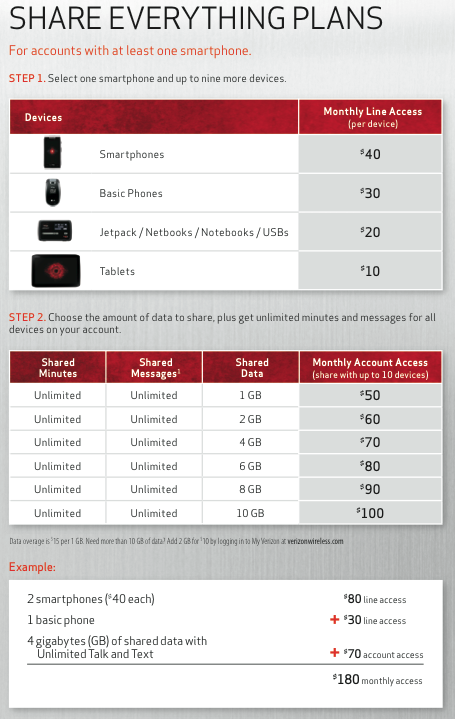

Verizon Wireless seems to have done so. If one compares the existing cost of a single smart phone, with a $40 a month plan including 450 anytime minutes, $20 for unlimited texts, and $30 for 2GB of data, plus $30 for 2GB of data on a connected tablet, the person who owns both devices is currently paying $120 per month for the two devices.

With a shared plan that bumps them to unlimited minutes and shares the whole 4GB of data between devices, their monthly total also costs $120 a month.

But the more telling analysis is the cost for a user who does not connect his or her tablet to the Verizon network. Using the same plan as above, that "phone only" user spends $90 a month just for the phone account.

Adding the tablet represents an incremental cost of $10 for the access. Assuming that user upgrades the data plan to about $70 a month (4 Gbytes), Verizon gains an incremental $40 in mobile data spending, for an incremental increase of $50 a month for a single-device smart phone account adding one connected tablet. That's a significant increase in recurring revenue.

If the single smart phone user only wants to upgrade the data bucket to use the personal hotspot feature, the incremental revenue is $40 a month. That is serious money if enough users upgrade.