Monday, July 30, 2012

"Computers" Hardly Matter for Apple, Anymore

Apple doesn't call itself "Apple Computer" anymore for a very good reason. It makes its money, and profit margin, selling phones, as Wings of Reason illustrates.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Is "Mobile First" Now Affecting Financial Returns?

Is "mobile first" now affecting application and device provider financial returns? You might argue so.

“What we’re seeing is that the non-mobile-centric Four Horsemen, Amazon and Facebook, aren’t seeing the same big profits as the two mobile-centric ones, Apple and Google," says Yankee Group Research VP Carl Howe.

Facebook’s overall revenue in the second quarter of 2012 hit U.S.$1.2 billion, up 32 percent and beating estimates, but the company posted a net loss of U.S.$157 million vs. income of U.S.$240 million posted a year earlier.

Facebook frankly admits it has to create a mobile strategy, but has yet to do so in practice.

“What we’re seeing is that the non-mobile-centric Four Horsemen, Amazon and Facebook, aren’t seeing the same big profits as the two mobile-centric ones, Apple and Google," says Yankee Group Research VP Carl Howe.

Facebook’s overall revenue in the second quarter of 2012 hit U.S.$1.2 billion, up 32 percent and beating estimates, but the company posted a net loss of U.S.$157 million vs. income of U.S.$240 million posted a year earlier.

Amazon, for its part, announced a 96 percent drop in net income, to U.S.$7 million, primarily due to investments in and subsidies for its best-selling Kindle Fire mobile device,

But Google and Apple, which you might argue have head starts in terms of their "mobile first" strategies, are doing better, financially.

But Google and Apple, which you might argue have head starts in terms of their "mobile first" strategies, are doing better, financially.

In fairness, Amazon does, as a matter of strategy, emphasize big investments that provide strategic value, even if it hits quarterly earnings. You might argue that is simply what happened in the second quarter.

Facebook frankly admits it has to create a mobile strategy, but has yet to do so in practice.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Some People Just Don't Want to Buy Cable TV

Would lower prices-even prices 50 percent lower-convince you to buy a product you really did not want? That seems not to be the case for some 33 percent of survey respondents who have abandoned their video entertainment subscriptions, according to TechBargains.

Prices arguably are getting to be a major irritant for most consumers who buy video entertainment services. But not for all. Some consumers simply do not see value in buying video entertainment services at all, no matter what the price.

Prices arguably are getting to be a major irritant for most consumers who buy video entertainment services. But not for all. Some consumers simply do not see value in buying video entertainment services at all, no matter what the price.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Global Handset Shipments Decrease for the Second Consecutive Quarter

As important and as robust as mobile subscriber growth has been over the last decade, it is not invulnerable to economic stress. In fact, on a global basis, mobile handset shipments have declined for two consecutive quarters.

As important and as robust as mobile subscriber growth has been over the last decade, it is not invulnerable to economic stress. In fact, on a global basis, mobile handset shipments have declined for two consecutive quarters. An economist, tracking any nation's economic performance, would say that set of data marks the beginning of a recession.

“Handset shipments have not seen a sequential year over year decline since the global economic crisis of 2008-2009," says ABI Research senior analyst Michael Morgan.

Of course, handset purchases often are affected by consumers waiting for hot new models to be released, while some might also note that the second quarter is a seasonally slower quarter.

Apple, for example, experienced a 26 percent quarter over quarter decline in shipments in the second quarter, as consumers withheld purchasing an iPhone in anticipation of the new model to be released in the late third quarter.

Research in Motion and Nokia experienced 14 percent and 30 percent quarter over quater declines respectively. To some extent, those dips might partially be explained by customers waiting for the next major product families from each of the suppliers, and in part by a shift of demand away from both suppliers.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

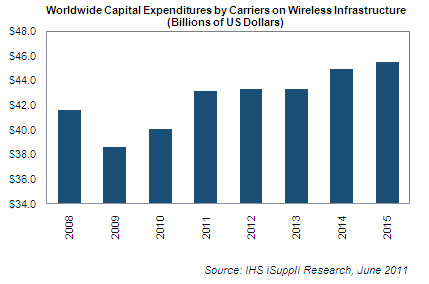

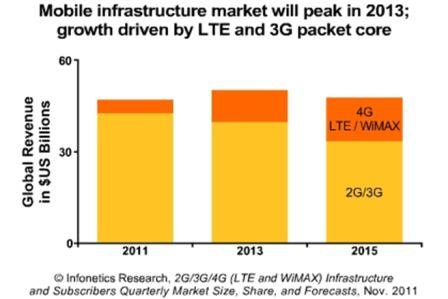

North American Mobile Capex to Grow in 2013

North American mobile operators will hike capital investment in 2013 to support fourth generation inetwork construction, ABI Research estimates. But some think 2013 might market a peak of mobile capital investment on a global basis.

North American mobile operators will hike capital investment in 2013 to support fourth generation inetwork construction, ABI Research estimates. But some think 2013 might market a peak of mobile capital investment on a global basis. Mobile capital investment fluctuates from year to year, based on network upgrade plans, economic conditions and competitive threats, and investment has been building since about 2008, partly because of 4G network constructiion and partly because operators were cautious during the Great Recession that began in 2008.

“North American mobile cellular capital expenditure is expected to hold its ground in 2012 year-on-year, with expenditure of around $10 billion”, says Jake Saunders, VP for forecasting at ABI Research. “In 2013, mobile capital expenditure is likely to surge 4.9 percent to $10.5 billion.

Service providers are in many cases also shifting investment from older networks to 4G. Verizon Wireless, for example, has announced an end to the expansion and capacity enhancement of its 3G network, in favor of building out its 4G LTE coverage.

Mobile operators, as typically is the case, squeezed capital expenditure during the economic downturn in order to protect cash flows and maintain profits. What normally happens is a catch-up phase where deferred investment gets made.

Wireless Intelligence notes that total global mobile capex peaked at $204 billion in 2008, at the beginning of the financial crisis, accounting for 21 percent of total revenues.

Wireless Intelligence notes that total global mobile capex peaked at $204 billion in 2008, at the beginning of the financial crisis, accounting for 21 percent of total revenues.However, capex then fell to $197 billion (19 percent of revenue) by 2010, as operators reacted to the crisis. In developed mobile markets operators reduced capex by eight percent in 2008 and by six percent in 2009, increasing capex again in 2010 as many operators began investing in LTE.

The typical investment slowdown in tougher economic times boosts free cash flow, at least temporarily.

The reductions in capex over the last few years saw operating free cash flow grow to $200 billion (19 percent of revenue) by 2010, up from $133 billion (11 percent of revenue) in 2007.

This means that global operator cash flows are now roughly at the same level as capex. In 2011-12, Wireless Intelligence has predicted operator capex to remain stable at 16 percent of total revenue in developed markets and 23 percent in developing markets. OFCF will account for close to 20 percent of total revenues in both regions.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sunday, July 29, 2012

New Zealand Mobile Operators Eye December 2012 Decision on Mobile Payments Venture

New Zealand mobile service providers say they will decide by the end of 2012 whether to create a mobile payments joint venture.

Bank-owned Paymark, Vodafone, Telecom and 2degrees had said they wanted to form a mobile payments business in April 2012, based on use of near field communications.

Another mobile payments trial was launched in the spring of 2012.

Bank-owned Paymark, Vodafone, Telecom and 2degrees had said they wanted to form a mobile payments business in April 2012, based on use of near field communications.

Another mobile payments trial was launched in the spring of 2012.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Google Fiber Could Get 20% Penetration of Some Kansas City, Mo. Neighborhoods, Quickly

Within just two days, more than 20 percent of the eligible neighborhoods on the Missouri side of Kansas City already have already reached Google’s thresholds for activating home drops. If all those households actually wind up subscribing, Techcrunch reports.

Each neighborhood can have a different threshold, ranging from five percent of homes to 25 percent of homes.

Google Fiber could hit at least 20 percent penetration relatively quickly. In the neighborhood with the highest rate of interest, Google Fiber has reached about 18 percent of homes.

You can track progress online.

Things apparently aren’t moving quite as fast in Kansas City, Kansas, though, where the median household income is significantly lower than on the other side of the city.

Each neighborhood can have a different threshold, ranging from five percent of homes to 25 percent of homes.

Google Fiber could hit at least 20 percent penetration relatively quickly. In the neighborhood with the highest rate of interest, Google Fiber has reached about 18 percent of homes.

You can track progress online.

Things apparently aren’t moving quite as fast in Kansas City, Kansas, though, where the median household income is significantly lower than on the other side of the city.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

AI Might be a Threat that Computer-Generated Graphics Have Not Been

Netflix has guidelines for use of generative AI based on five main points: The outputs do not replicate or substantially recreate identifia...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...