In fact, Brazil has more smart phone users than Germany or France do. In fact, with about 27 million and 23 million smart phone users respectively, Brazil and Mexico both have more smart phone users than Australia has people (Australia’s population is around 22 million).

Google's Mobile Planet also revealed that Argentina has 24 percent smart phone penetration.

These numbers defy the common perception that these large Latin American markets are far behind the rest of the world in smart phone adoption, Google argues. They in fact already possess larger absolute numbers of smartphone users than many other countries, and above-average usage patterns in many areas, Google says.

Some 65 percent of Mexican smart phone users search on their phones every day, compared to 57 percent in the U.S. market.

Some 90 percent of Argentine smart phone users use their phones to access social networks, compared to 63 percent in Japan, and 29 percent of Brazilian smartphone users have changed their minds about a purchase while in a store due to research conducted on their phone, compared to 15 percent in Canada.

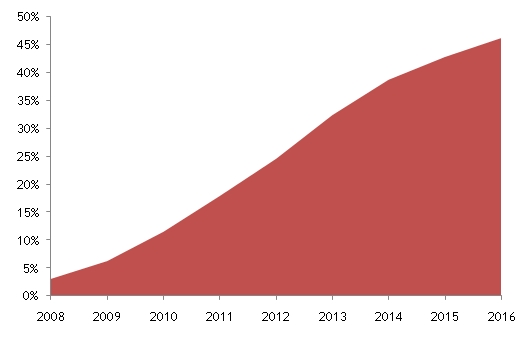

Latin America’s smart phone sales picked up in 2010 when smart phone sales in the region grew 117 percent and total handset sales grew 17 percent.

In 2011 smartphone sales were predicted to represent 17.9 percent of total handset sales and will continue to be the fastest growing category, increasing at a compound annual growth rate of 30 percent in the next five years, compared with a seven percent CAGR for overall handset sales during the same period.

By 2016, Pyramid Research expects smart phone sales to account for roughly 46 percent of total handset sales in the region.

Others might point to China as the driver of growth in emerging markets. Research firm Ovum says emerging markets in 2011 accounted for 160 million of 450 million smartphones sold worldwide. China accounted for about 66 percent of smartphones sold in developing markets, Ovum says.

Latin America smartphone sales as percentage of total handset sales, 2008–2016