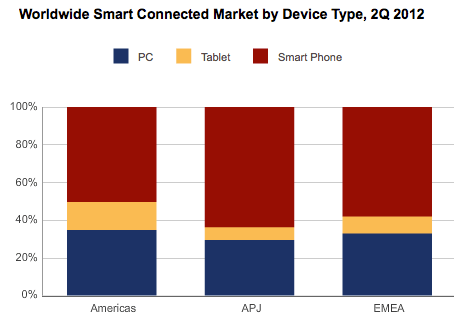

Smart phones now account for 59 percent of connected device shipments, and will grow 15.8 percent annually, to reach nearly 63 percent of smart device shipments by 2016, Forrester Research says.

Smart phones now account for 59 percent of connected device shipments, and will grow 15.8 percent annually, to reach nearly 63 percent of smart device shipments by 2016, Forrester Research says.Tablets will grow the fastest, though, rising from a 10 percent share in 2012 to 13 percent by 2016.

PC share will drop from 31 percent to 24 percent during the same time period.